Let us learn about Tax Multiplier of National Income.

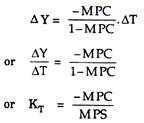

We have seen earlier that a tax increase results in a decline in income. In other words, it is contractionary in effect. An increase in tax (∆T) leads to a decrease in income (∆Y). The ratio of ∆Y/∆T, called the tax multiplier, is designated by KT.

Thus,

KT = ∆Y/∆T and ∆ Y = KT. ∆ T

ADVERTISEMENTS:

Again, how much national income would decline following an increase in tax receipt depends on the value of MPC:

The formula for KT is:

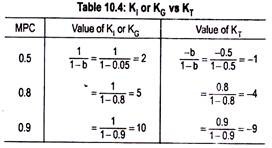

Thus, tax multiplier is negative and, in absolute terms, one less than government spending multiplier. If MPC = ¾ then the value of KT = (-3/4)/ (1 – 3/4) = – 3. This means that an increase in taxes of Rs. 20 crore results in a decline of income of Rs. 60 crore.

ADVERTISEMENTS:

That is to say

60 = (-3/4)/(1 – 3/4). 20

In contrast, with an MPC = 3/4, the value of KG = 4. Assume an increase in government expenditure of Rs. 20 crore.

Applying the formula for KG, we obtain:

ADVERTISEMENTS:

∆ Y = 1/1 – MPC. ∆G

80 = 1/ 1 – 3/4. 20

∆Y/∆G = 80/20 = 4

Thus, KT is negative and its value is one short of KI or KG.

Graphically, tax multiplier has been shown in Fig. 10.18. Pre-tax consumption line and aggregate demand schedule are represented by CI and CI + I̅ + G̅, respectively.

The corresponding level of income is OY1. An increase in taxes shifts consumption line to C2. Consequently, aggregate demand schedule also shifts downwards to C2 + I̅ + G̅. Consequently, income declines to OY2. Thus the effect of an increase in taxes on income is contractionary.

One must know the distinction between KI or KG and KT. This is demonstrated in Table 10.4.

Thus, KT is negative and one less than KI or KG.

ADVERTISEMENTS:

The G-multiplier and the T-multiplier are also called fiscal multipliers as these multipliers are associated with the fiscal activities of the government (i.e., changes in expenditure and taxation plans).