1. Introduction to Management of Inventory

Inventory management occupies the most significant position in the structure of working capital. Management of inventory may be defined as the sum of the total of those activities necessary for the acquisition, storage, disposal or use of materials. Inventory is one of the important components of current assets.

Inventory management is an important area of working capital management, which plays a crucial role in economic operation of the firm. Maintenance of large size of inventories requires a considerable amount of funds to be invested on them. Efficient and effective inventory management is necessary in order to avoid unnecessary investment and inadequate investment.

A considerable amount of funds is required to be committed in inventories. It is absolutely imperative to manage inventories efficiently and effectively in order to optimise investment in them. Prudent inventory management is one of the challenging tasks of the financial manager.

Efficient management of inventory reduces the cost of production and consequently increases the profitability of the enterprise by minimising the different types of costs associated with holding inventory. An undertaking, neglecting the management of inventories, will be jeopardising its long-term profitability and may fail ultimately.

ADVERTISEMENTS:

It is possible for a firm to reduce its level of inventories to a considerable degree, i.e., 10 to 20 percent of current assets without adverse effects on production and sales by using simple inventory planning and control techniques.

If business planning can be perfect, a firm may succeed even in attaining the “Zero inventory” norm which the Japanese management seems to suggest, is not too unrealistic a goal.

The reduction in inventories carries a favourable impact on the company’s profitability. The efficiency of inventory management in any firm depends on the inventory management practices adopted by it.

2. Meaning of Inventory Management

Inventory Management refers to the activities that are employed in maintaining the optimum number or the amount of every inventory item. Production process modification is the manufacturing procedure that is used to come up with new or modified items. Volume reduction is the processing of waste materials to reduce the space they occupy.

ADVERTISEMENTS:

Generally speaking, the application of managerial functions on the basis of management principles in the field of inventory is termed as inventory management. Managerial functions primarily include planning, organising, control and coordination. When all these four functions are performed with respect to inventory, it may be called inventory management.

In this sense, the inventory management signifies the planning, organising, controlling and coordinating the quantity and value of the inventory. Really speaking, the objective of inventory management is to plan the optimum size of inventory which is neither excessive nor deficient and is timely available.

For timely availability along with optimum size, there is need for controlling as well. Only on the basis of various control techniques one can ensure whether inventory would be timely available.

But effective control in itself depends upon organising and coordination. Thus, inventory management comprises the functions of planning, controlling and organising the types of all goods, quantity, status, flow and time-sequence etc.

ADVERTISEMENTS:

Inventories which comprise of raw materials, consumable stores, work-in-progress, and finished goods are to be purchased and stored. Inventory management is, therefore, a scientific method of determining what, when and how to purchase and how much to have in stock for a given period of time.

3. Objectives of Inventory Management

The objectives of inventory management may be viewed in two they are operational and financial The operational objective is to maintain sufficient inventory, to meet demands for product by efficiently organising the firm’s production and sales operations and financial view is to minimise inefficient inventory and reduce inventory carrying costs.

These two conflicting objectives of inventory management can also be expressed in terms of costs and benefits associated with inventory. The firm should maintain investments in inventory implies that maintaining an inventory involves cost, such that smaller the inventory, lower the carrying cost and vice versa. But inventory facilitates (benefits) the smooth functioning of the production.

An effective inventory management should:

1. Ensure a continuous supply of raw materials and supplies to facilitate uninterrupted production,

2. Maintain sufficient stocks of raw materials in periods of short supply and anticipate price changes,

3. Maintain sufficient finished goods inventory for smooth sales operation, and efficient customer service,

4. Minimise the carrying costs and time, and

5. Control investment in inventories and keep it at an optimum level.

ADVERTISEMENTS:

6. Others – apart from the above, the following are also objects of inventory management. Control of materials costs, elimination of duplication in ordering by centralisation of purchasers, supply of right quality of goods at reasonable prices, provide data for short-term and long- term planning and control of inventories.

Therefore, management of inventory needs careful and accurate planning so as to avoid both excess and inadequate inventory in relation to the operational requirement of a firm. To achieve higher operational efficiency and profitability of a firm, it is very essential to reduce the amount of capital locked up in inventories.

This will not only help in achieving higher return on investment by minimising tied-up working capital, but will also improve the liquidity position of the enterprise.

4. Importance of Inventory Management

Inventory management is now an integral part of general management. Three important functional aspects of a business are closely related to inventory management and this functional management is production management, marketing management (sales management) and financial management.

ADVERTISEMENTS:

As far as production management and marketing management are concerned, these are related to the physical aspect of inventory management; financial management is concerned with the financial aspect of the inventory management.

Production managers will always strive to have such a large inventory of raw materials and of such a good quality as to ensure stable production operations. Similarly, marketing managers aim at satisfying ever-increasing demands for improved customers’ service by having large inventory of inside goods.

On the other hand, a finance manager’s efforts will be to keep investments in different types of inventory at a minimum possible level so that the business concern may earn maximum return.

Needless to mention that the production manager and marketing manager cannot oversight the financial aspects of inventory management. In fact, a proper coordination is needed taking into account the goal of the entire business, for which budgetary control is the appropriate technique.

ADVERTISEMENTS:

The above discussion indicates that taking into account the needs of each business concern; one has to determine the quantity of inventory. The quantity of inventory should neither be excessive nor is deficient of what is required. In other words, the size of inventory quantity should be economical or optimal.

5. Types of Inventory Management

Types of Inventory Management – Raw Material, Work in Progress, Consumable, Finished Goods and Spares

Types of inventory management are as follows:

Type # 1. Raw Material

A basic material on which a manufacturing process is carried to make a product. Raw materials can be unprocessed natural substances or in a semi-processed state.

Type # 2. Work in Progress

WIP is a stage of a transformation process that is either under way or will take place in the future.

Type # 3. Consumable

These are the materials which are needed to smooth running of the manufacturing process.

Type # 4. Finished Goods

Finished product is resulting material after it has been processed and forms an essential part of virtually all business operations.

Type # 5. Spares

ADVERTISEMENTS:

It is also a part of inventories, which includes small spares and parts.

8 Main Types of Inventory Management – Raw Material, Work-in-Process, Finished Goods, Flabby Inventory, Profit-making Inventory, Safety Inventory and More…

Types of inventory management are explained below:

1. Raw Material:

To hold stocks of raw material, an organisation deploys its primary production sections or processes to obtain raw materials from manufacturers and stockists.

2. Work-in-Process:

The holding of both raw materials and stocks of finished goods is generally a planned activity. In process stocks, however, they are likely to exist in any manufacturing organisation, whether they are planned for or not.

3. Finished Goods:

The stock of finished goods provides a buffer between customer and demand and manufacturer’s supplies.

4. Flabby Inventory:

It comprises finished goods, raw materials and stores held because of poor working capital management and inefficient distribution.

5. Profit-making Inventory:

ADVERTISEMENTS:

It represents stocks of raw materials and finished goods held for realising stock profit.

6. Safety Inventory:

It provides for failures in supplies, unexpected spurt in demand, etc., although there may be an insurance cover.

7. Normal Inventory:

It is based on a production plan, lead time of supplies and economic ordering levels. Normal inventories fluctuate primarily with change in the production plan. Normal inventory also includes a reasonable factor of safety.

8. Excessive Inventory:

Even an efficient management may be compelled to build up excessive inventory for reasons beyond its control, as in the case of strategic import or as a measure of government price support of a commodity.

Prakash Tandon Committee in their “Report of the Study Group to frame guidelines for follow-up of Bank Credit” observed that ‘flabby’ inventory should not be permitted, and ‘profit-making’ inventory ought to be positively discouraged. A good management brings down safety inventory as much as periodical statistical checks may justify.

Excess inventory is a luxury which the banker does not encourage. If the normal inventory is to be further analysed, one is fluctuating and the other steady. In the steady part also, there is ‘core’ which is fixed representing the absolute minimum level of raw materials, process stock, finished goods and stores which are in the pipeline and ensure continuity of production.

ADVERTISEMENTS:

These funds invested in core inventories are, therefore, blocked, on a long-term basis due to technological and business considerations like the investment in fixed assets.

Types of Inventory Management According to Functions – Transit, Cycle, Buffer, Decoupling and Other Inventories

All inventories may be described as performing one or more of transit. Cycle, buffer, seasonal and decoupling function.

The following is the types of inventory management according to functions:

Type # (i) Transit Inventories:

These are primarily pipeline inventories and their existence arises because of the need to transport inventories from one point to another larger the distance of supply source, larger is the transit inventory. Work in process transit inventories are determined by process design and plant layout.

Type # (ii) Cycle Inventories:

These exist because of management’s attempt to provide Economic Order Quantity. Here inventories tend to accumulate at various points in the system.

Type # (iii) Buffer Inventories:

In any organisation as a result of uncertainties of the demand and supply of units/price changes, some inventory is to be maintained. The size of buffer inventory may be of significant financial consequence to a firm. These can be reduced by reducing uncertainties of demand and supply and price variations.

ADVERTISEMENTS:

In periods of shortages and rapidly rising prices, although the need to increase inventory in the form of buffer and anticipation stock is clear, the ability of the organisation to commit the necessary funds may be severely taxed. These are also known as Safety Stocks.

Type # (iv) Decoupling Inventories:

The existence of inventories at major linkage points in a production process makes it possible to carry an activity on either side of the point relatively independent of each other.

Type # (v) Other Inventories:

Inventory can also be classified according to the nature of items stocked namely raw materials; in-process inventories, finished goods inventories and spare part inventories.

Example – Packing material, components etc.

4 Major Types of Inventory Management – Raw Materials and Purchased Components, In-Process Inventory, Finished Products Inventory and More…

An inventory is any stock of economic resources that is stored for future use. It is commonly used to indicate materials, raw materials in progress, finished goods, packing materials, spares, etc. stocked in order to meet an expected demand or distribution in future.

Some of the major types of inventory management are:

Type # 1. Raw Materials and Purchased Components:

These are raw-materials, parts and components which enter into the product directly during the production process and generally form part of the product.

Type # 2. In-Process Inventory:

Work-in-progress inventory is often maintained between manufacturing operations within a plant to avoid production hold ups in case a critical machine or equipment was to breakdown and also to equalize production flow. In process inventory semi-finished parts, work-in-process and partly finished products formed at various stages of production.

Type # 3. Finished Products Inventory:

Finished goods are another important part of inventories, especially for the wholesalers and manufacturers. While holding finished goods inventory, it is important to have an adequate and not excess stock of inventories as they may incur cost as well as loss if the excess inventory is not sold out in time. It includes complete finished products ready for sale.

Type # 4. Maintenance, Repair and Tooling Inventory:

Maintenance, repairs and operating supplies which are consumed during the production process and generally do not form part of the product itself (e.g. Petroleum products like petrol, kerosene, diesels, various oils and lubricants, machinery and plant spares, tools, jigs and fixtures etc.).

To manage these various kinds of inventory management, two alternative control procedures can be used:

(a) Materials Requirement Planning (MRP):

It is important that the proper control procedure be applied to each of the four types of inventory. In general, MRP is the appropriate control procedure for inventory types 1 and 2.

(b) Order Point Systems:

This has been the traditional approach to inventory control. In these systems, the items are restored when the inventory levels become low. Order point systems are often considered the appropriate procedure to control inventory type 3 and 4.

3 Types of Inventory Management of a Manufacturing Concern

The Production manager and Finance manager of a manufacturing company should know the items of inventory, classification of inventory and costs related to each item of inventory before taking any step for efficient management of inventory.

The efficiency shown in inventory will have a direct impact on profitability of a business enterprise. In our study about management of inventory, here, we only discuss the first category of inventory i.e., raw materials.

The inventory management of a manufacturing concern is classified into the following types:

i. Raw Materials

It includes direct material used in the manufacture of a product and it also includes the components, fuel etc. used in the manufacture.

ii. Work-in-Progress

It includes partly finished goods and materials, subassemblies etc. held between manufacturing stages. Stocks of work-in-progress are in the process of production.

iii. Finished Goods

The goods ready for sale or distribution will come under this category.

Types of Inventory Management

Types of inventory management are as follows:

Type # (a) Raw material Inventory

It consists of those items of inputs such as basic raw materials which are converted into finished goods through the manufacturing process.

Type # (b) Work-in-Progress Inventory

It consists of those material inputs which are in partially finished or semi-finished stage under the production process.

Type # (c) Finished Goods Inventory

It consists of completed products which are ready for sale but are lying in stock i.e. could not be sold so far.

6. Risk Associated with Inventory

The risk in inventory management signifies the chance that inventories cannot be turned over into cash through normal sale without a loss.

These risks are due to following three factors:

1) Price decline

The main risk in inventory investment is that the market value of inventory may fall below what the firm paid for it, hereby causing inventory losses. It may result from an increase in the market supply of products, introduction of a new competitive product and price reduction by competitors.

2) Product deterioration

It may result due to holding a product too long or it may occur when inventories are held under improper conditions of light, heat, humidity and pressure.

3) Obsolescence

Obsolescence means out of date or out of fashion. This risk arises due to the change in consumer tastes, this can be due to new production techniques, improvement in the product design, specifications etc.

7. Purposes of Holding Inventories

The following are the main purposes or motives for holding inventories:

1) Transaction Motive

The first and the most important purpose of holding inventory to meet the day to day requirement of sales, production process, customer demand etc. This facilitates continuous production and timely execution of sales orders.

2) The Precautionary Motive

Firms keep the balance of inventory to meet some unforeseen circumstances like strike, natural calamities or any other reasons. This necessitates the holding of inventories for meeting the unpredictable changes in demand and supplies of materials.

3) The Speculative Motive

Firms keep some inventory in order to capitalize an opportunity to make profits, e. g. sufficient level of finished goods may help the firm to earn extra profit in case of unexpected shortage in the market.

8. Costs Associated with Inventory

Every firm maintains some stock of material depending upon the individual requirement of the firm. The benefits of holding inventory, no doubt there are some costs also associated with inventory.

The followings are the costs which are associated with inventory:

1) Material Cost

Material cost also known as purchasing cost of material.

2) Ordering Cost

This refers to the costs associated with the ordering of the materials. This is known as ordering cost per order. This cost doesn’t have any impact on the quantity of material. This is the same for all quantities. This includes the cost of requisitioning material. Placing an order, follow up, receiving the evaluating quotations.

3) Inventory Cost/ Carrying Cost/Holding Cost

This is the cost of holding the inventory. It is measured in per unit per year that means the cost of holding one unit of inventory for a year. This includes the cost of storage, insurance, product deterioration and obsolescence, spoilage, breakage, pilferage, interest on capital etc.

4) Stock-out or Shortage Costs

When the firm is having demand for the product in the market but the firm doesn’t have inventory to sell, this makes a firm unable to fill an order, and this will lose the sale. This includes the following costs – Loss of profit due to lost sale, Loss of future sales because customers may go elsewhere, Loss of goodwill.

9. Factors Affecting Level of Inventory

There is no hard and fast rule regarding the level of inventory to be kept by the firms, this is affected by several factors; the important among them are as under:

1) Nature of Business:

Most important determinant of the level of inventory is the nature of the business. A manufacturing firm will have a high level of inventory as compared to the trading firm.

2) Nature of Product:

If the product is perishable the level of inventory should be kept low due to the chances of rotting, on the other hand durable products can be kept easily with less probability of loss. The firms dealing in seasonal products have to hold large stock of finished goods during peak season to meet the demand.

3) Financial Position:

A firm which is financially sound may buy material in bulk and hold them for future use. While a firm having shortage of funds cannot maintain a large stock level.

4) Length of Manufacturing Cycle:

Length of Manufacturing cycle and the requirement of working capital are directly related with each other. Manufacturing cycle is the time lag between the conversions of raw material into finished goods. The longer the time required for inventory to convert in finished goods the greater the requirement of inventory.

5) Rate of Inventory Turnover:

The rate of inventory turnover is the time period within which inventory completes the cycle of production and sales affects the level of inventory. When the turnover rate is high, investment in inventories tends to be low and vice-versa.

6) Inventory Cost:

There are some costs associated with the inventory like ordering cost and holding cost. This cost also affects the level of inventory, because a firm normally determines the inventory level on the basis of economic order quantity and these costs affect the economic order quantities.

10. Process of Inventory Management and Control

The planning of the control of inventory can be divided into two phases, inventory management and inventory control.

Inventory management accomplishes the first phase, consisting of-

1. Inventory Management:

(a) Optimum Inventory Levels:

But this is not the only factor that must be considered by inventory management when determining inventory levels. The planning for the actual production of the product may involve problems of leveling production that is producing at a constant rate even though sales may fluctuate.

(b) Degree to Control:

This Inventory management must decide just how much control is needed to accomplish the objective. The least control – as evidenced by systems, records, and personnel- that is required to perform the function efficiently is the best control. This problem of the degree of control can be approached from the viewpoint of quantity, location and time.

(c) Just-in-Time Concept:

JIT can be implemented with manufacturing work-in- process or with material purchased from outside vendors. One truck transportation company obtains much of its business by catering to companies that must deliver parts to other companies “just in time”.

2. Inventory Control:

The inventory control group puts the plans of inventory management into operation. These plans are seldom complete in every detail. The day-to-day planning required to meet production requirements – the second phase of planning for inventory control -is the responsibility of this group.

11. Dangers of Excessive Inventory

Risks and Costs of Excessive Inventory:

(i) Excessive Carrying Costs

The carrying costs such as storage costs, holding costs, insurance expenses etc. also increase in proportion of inventory. Excessive inventory results in unnecessary tie-up of the firm’s fund and loss of profit due to high carrying costs.

(ii) Risk of Loss of Liquidity

Excessive inventory also increases risk of loss of liquidity. If excessive funds are invested in inventories, it may not be possible to sell inventories at full value whenever funds are required.

(iii) Risk of Price Decline

The price decline in the market may cause finished goods to be sold at low prices. In case of excess inventory, the risk of loss due to price decline is more.

(iv) Risk of Deterioration of Goods

Normally, there is always deterioration of some goods with the passage of time and due to improper storage facilities. Risk of deterioration of goods is more in case of excessive inventory because inventory remains in stores for a longer period.

(v) Risk of Obsolescence

Goods may become obsolete due to change in technique, change in design, and change in consumer’s choice etc. Obsolete goods have to be sold at lower prices. Risk of loss due to obsolescence is more in case of excessive inventory.

12. Dangers of Inadequate Inventory

(i) Risk of Break-down in Manufacturing Process

In case of inadequate inventory of raw-material, there is always a risk of break-down in the manufacturing process due to lack of raw-material supply. Therefore, the firm will not be able to utilise its manufacturing capacity in full. It also increases cost of manufacturing per unit because fixed costs of manufacturing do not reduce even if there are frequent interruptions in production.

(ii) Risk of not Meeting Demand of Customers

In case of inadequate inventory of finished goods, demand of customers may not be met and they may shift to competitors. It will result in permanent loss to the firm.

13. Techniques of Inventory Management

There are many techniques of inventory management.

Here we explain only two of them:

1. ABC analysis and

2. EOQ.

1. ABC Analysis:

ABC Analysis is an inventory categorization technique, which suggests that inventories of a firm are not of equal value. Thus, the inventory is grouped into three categories (A, B, and C) in order of their estimated value and importance.

‘A’ items are very important for an organization. Because of the high value of these ‘A’ items, frequent value analysis is required. In addition to that, an organization needs to choose an appropriate order pattern (e.g. ‘Justin- time’) to avoid excess inventory of these items. For these items, very tight control and accurate records are required.

‘B’ items are important, but of course less important than ‘A’ items and more important than’ C’ items. For these, tight control and accurate records are required but lesser than A’ items.

‘C’ items are insignificant in value and are marginally important. For them, simplest controls and minimal records are sufficient.

The classification system is:

i. ‘A’ items – 20% of the items accounts for 70% of the annual consumption value of the items.

ii. ‘B’ items – 30% of the items accounts for 25% of the annual consumption value of the items.

iii. ‘C’ items – 50% of the items accounts for 5% of the annual consumption value of the items.

However, sometimes an inventory item in “C Class” although inexpensive, may be critical for the production process and may not be easily available. Thus, in such a case, proper attention needs to be given for its effective management.

For example in case of a Jeweller, Diamond jewellery may be classified as ‘A’ items, Gold jewellery as ‘B’ item and silver jewellery as ‘C’ item.

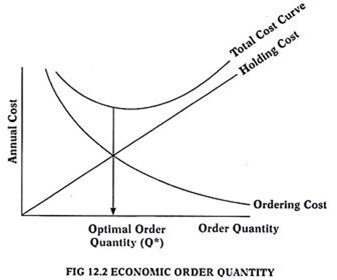

2. EOQ Model:

EOQ model is used to calculate optimal lot size of inventory. Excess inventory and shortage of inventory, both are dangerous. Therefore a firm must maintain optimal inventory.

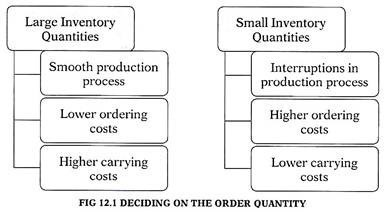

The following diagram depicts the impact of holding large and small inventory quantity levels:

Economic Order Quantity (EOQ) Model:

The optimum level of inventory can be determined with a popular technique known as Economic Order Quantity (EOQ). EOQ determines the optimum order quantity that minimizes the total cost of inventory.

EOQ is based on the following assumptions:

i. The annual inventory requirement (D) is known with certainty and is constant.

ii. Ordering cost per order (B) and carrying cost per unit (C) per annum are known with certainty and constant over the year.

iii. There is uniform consumption of inventory throughout the year.

iv. There is no time lag between the placement of an order and getting its supply. Hence there is instant replenishment of inventory.

v. There are only two costs associated with inventory i.e. ordering cost and carrying cost.

(i) Calculation of EOQ (or Economic Lot Size):

Given the above assumptions, the EOQ level of inventory which leads to minimum total inventory costs is calculated using the following formula –

Where,

D – Annual usage or requirement of inventory

B – buying cost per order

C- carrying cost per unit p.a.

(ii) Total ordering cost = No. Of orders X Ordering cost per order

No. Of orders = Annual usage or requirement of inventory / Lot size

(iii) Total carrying cost = Average inventory X Carrying cost per unit p.a.

Average inventory = Lot size / 2

(iv) Total cost of Inventory = Total ordering cost + Total carrying costIt must be noted that when lot size is EOQ, total cost of inventory is minimum. Further, at EOQ, total ordering cost and total carrying cost will be equal. Any other lot size will have higher total cost of inventory.