Beyond linearity, other simplifying assumption limits the advantages of break-even analysis; actual costs incurred(fixed and variable) are substituted for opportunity costs; the business environment is taken as static, that is factors other than volume affecting revenues and costs, such as demand and technology, are assumed to be insignificant; still more importantly, risk and uncertainly are ignored.

However, some simple assumptions are relaxed in certain extensions of break-even analysis; in case of multiproduct, multi-constrained production process, linear programming can be used to identify such product mixes as would allow the firm either to break-even or to maximise profits.

Moreover, nonlinear revenue and costs including semi-fixed costs (discontinues, stepwise cost functions) and semi-variable costs (costs that vary with output but that are partly fixed, even if no output is produced) can be introduced into the analysis.

ADVERTISEMENTS:

A break-even analysis is useful for the obvious purpose of seeing how many units must be sold to make a profit, but it also helps with other types of decisions, such as the choice between buying or leasing equipment, making sure there is enough capacity when buying new equipment, whether to buy an item or make it within the company, or submitting tenders for winning contracts.

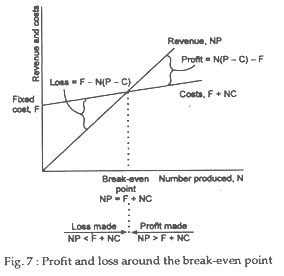

Break-even analysis evolved as an attempt to enable management to use the economic model of the firm by processing cost and revenue data compiled by the accountants. Perhaps the most common difficulty in calculating break-even points is assigning a reasonable proportion of overheads to each product. This depends on the accounting convention used within the organisation.

The problem is made worse if the product mix is constantly changing. Then accounting practices will allocate a changing amount of overheads to each product. In other words, the costs of making a particular product, and hence its profit, can change even though there has been no change in the product itself or the way it is made.