In this article we will discuss about the monetary-fiscal policy link, explained with the help of suitable diagrams.

The central bank also handles national debt. Where the national debt is large, as in India, its management cannot be separated from open market operations and the general conduct of monetary policy and this, therefore, becomes an essential function of the central bank.

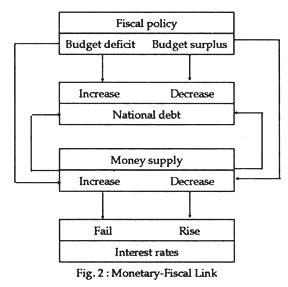

The relation between fiscal policy, monetary policy and national debt is shown in highly simplified form in Fig. 2. A budget deficit may be financed in a number of ways and various methods may be used at the same time. If the deficit is financed by borrowing, the national debt will increase.

On the other hand, if the deficit is financed by printing and issuing new money, the debt will not increase. Debt which is held in the central bank is part of official holdings and is not therefore regarded as part of market holdings.

ADVERTISEMENTS:

A budget surplus may be financed by reducing the money supply or by redeeming part of the national debt. Both of these may occur at the same time. The problem with varying the money supply is that, an increase is inflationary when the economy is nearing full employment and changes in the money supply are normally complementary to changes in rates of interest and, thus, affect investment and the rate of growth. There are also the liquidity aspects of the monetary system. Changes in the supply of money may well affect liquidity “hoards” rather than expenditure on currency output.

What the diagram does not show is the two-fold relationship between the national debt and the money supply, when the government is reducing the debt by purchasing it through the open market operations of the central bank.

Under these circumstances the cash basis of bank lending is increased and the result is the same as if the government had purchased the debt with newly printed money. In the opposite case, the sale of additional debt transfers money into the hands of the government.

ADVERTISEMENTS:

Since money is a highly liquid asset and debt is less liquid, the result of these operations is a change in the liquidity of the assets held by the community. Selling debt tends to lower its price and force up rates of interest. Purchasing debt has the opposite effect.

In effect, an increase in the budgetary deficit of the government implies an increase in government borrowing requirement. To meet the deficit, the government has to borrow any selling gilts (or long-term government securities) to the public and by the taking up of short-term public sector debt (bills) by the banks which increases the asset base of the banks as these securities constitute bank reserve assets. This enables the banks to undertake the multiple expansion of credit, which represents an increase in money supply. Fig. 3 illustrates the link between government expenditure and the money supply.

The government may attempt to sell as much of its debt as possible outside the banking system, to the public or other financial institutions, but in order to do this it will leave to increase interest rates in order to attract them. To prevent an increase in the money supply by this method, therefore, implies a higher level of interest rates.