In this article we will discuss about the price elasticity of demand, explained with the help of suitable diagrams.

In 1890, Alfred Marshall, the great neo-classical economist, developed a special measure for the response of one variable, such as quantity demanded, to change in another variable, such as price. It is called elasticity which is a measure of market sensitivity of demand.

The law of demand simply states that a fall in the price of a commodity will lead to an increase in the quantity demanded of the same. But, in case of some commodities a small fall in price leads to a large increase in quantity demanded, as in the case of ladies garments. In other cases, a large drop in price does not lead to much increase in quantity demanded, as in the case of salt or life-saving drugs.

Thus, the degree of responsiveness of the quantity demanded of a commodity varies and elasticity is a measure of such responsiveness. Thus, the law of demand describes the relation between price change and quantity change. The elasticity of demand quantifies such changes and gives us an accurate measure of how consumers respond to price change.

ADVERTISEMENTS:

In short, the law of demand indicates the direction of price change and quantity change i.e., price change and quantity change in the opposite direction. Elasticity of demand indicates the magnitude of such change.

The quantity demanded of a commodity is affected by a large number of variables. Elasticity of demand measures the degree of responsiveness of quantity demanded of a commodity to a change in one of the variables affecting demand (i.e., to a change in any one of the demand determinants). The response to change in each influencing variable is measured by a separate elasticity concept. We may start with the most commonly encountered of all elasticities, viz., and price elasticity of demand.

The Law of Demand states that if the price of a commodity falls, the quantity demanded of that commodity will increase. But, will it be a large or a small increase? The degree to which the quantity demanded of a commodity responds to a change in its own price is known as ‘price elasticity of demand’.

If a change in price leads to a relatively large change in quantity demanded, then demand for the commodity is said to be elastic. If the change in quantity demanded is relatively small, demand is said to be inelastic. This point is illustrated in Fig. 5.

ADVERTISEMENTS:

In both diagrams a fall in price from OP1 to OP2 has resulted in an increase in quantity demanded from OQ1 to OQ2. In [Fig. 5(a)] the change in quantity demanded of T.V. sets is relatively large (demand is elastic), whereas in [Fig. (b)] the change in case of bread is small in relation to the price change (demand is inelastic).

Measurement:

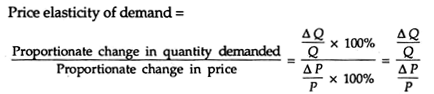

Price elasticity of demand is measured by using the formula:

The symbol A denotes any change. This formula tells us that the elasticity of demand is calculated by dividing the % change in quantity by the % change in price which brought it about.

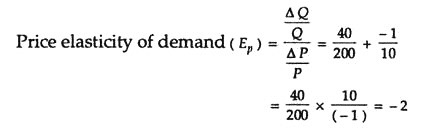

Thus, if the price of a commodity falls from Re.1.00 to 90p and this leads to an increase in quantity demanded from 200 to 240, price elasticity of demand would be calculated as follows:

Here Ep is called the coefficient of price elasticity of demand and is always a pure number (like ½, 1, 2,3, etc.) because it is the ratio of two percentage changes.

Note that Ep must always be a negative number, because quantity demanded and price move in the opposite direction to one another, i.e., if price rises quantity demanded falls; if price falls quantity demanded rises. So, there will always be a negative figure for Ep. Normally we drop the negative sign and take the absolute value of Ep.

If the actual figure given by the formula is greater than 1, demand is elastic; if it is less than 1, demand is inelastic; if it is equal to 1, demand has unit elasticity. Demand is unitary elastic where the proportionate change in quantity demanded and price are equal.

The Total Outlay Method (Test):

A simple method of determining price elasticity is by reference to the total revenue derived by a firm from the sale of the commodity or the total outlay of consumers on a product. If the price of the commodity falls, quantity demanded will increase. But, what will happen to total outlay? What happens to total outlay will depend upon the extent to which quantity demanded increases.

If quantity demanded increases a great deal—to more than offset the fall in price — total outlay will increase and demand is said to be elastic. Thus, in Fig.1 when price falls from OP1 to OP2 total outlay increases from OP1 XQ1 to OP2 YQ1. If, however, quantity demanded increases only slightly, i.e., not enough to offset the fall in price, total outlay will fall and demand is said to be inelastic.

ADVERTISEMENTS:

In Fig. 1 total revenue falls from OP1LQ1 to OP2MQ2. If quantity demanded increases only enough to offset the fall in price, total outlay will be unchanged and demand is said to have unit elasticity. We can adopt the same approach for price rise.

As Lipsey puts it, “The change in total expenditure brought about by a change in price is related to the elasticity of demand. If elasticity is less than unity, the percentage change in price will exceed the percentage change in quantity. The price change will then be the more important of the two changes, so that total expenditure will change in the same direction as the price changes. If, however, elasticity exceeds unity, the percentage change in quantity will exceed the percentage change in price. The quantity change will then be the more important change, so that total expenditure will change in the same direction as quantity changes (that is, in the opposite direction to the change in price).”

The three main points to be noted here are listed in Table 1:

ADVERTISEMENTS:

1. If elasticity of demand exceeds unity (elastic demand), a fall in price increases total expenditure on the good and a rise in price reduces it.

2. If elasticity is less than unity (inelastic demand), a fall in price reduces total expenditure on the good and a rise in price increases it.

3. If elasticity of demand is unity, a rise or a fall in price leaves total expenditure on the good unaffected.

ADVERTISEMENTS:

These three cases can be shown in Table 2:

Slope vs. Elasticity:

In this context, we may draw a distinction between the slope of the demand curve and its elasticity. We may note that the slope of the demand curve is ∆P/∆Q (which is always negative). It is so because P change and Q change are always in the opposite direction on a downward sloping demand curve.

Slope measures absolute change or it is the ratio of two absolute changes (i.e., absolute change in price and the absolute change in quantity). But elasticity measures percentage change. The reciprocal of the slope of the demand curve, i.e., ∆Q/∆P has to be multiplied by the original price-quantity ratio (P/Q) to find out the value of the elasticity coefficient.