The following points highlight the three main types of industries found in the long-run supply. The Industries are: 1. Constant-Cost Industry 2. Increasing-Cost Industry: Long-Run Supply Curve 3. Decreasing-Cost Industry.

Industry in the Long-Run Supply Type # 1. Constant-Cost Industry:

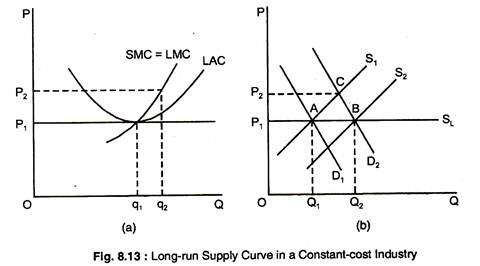

Fig. 8.13(a) and 8.13(b) show the derivation of the long-run supply curve for a constant- cost industry.

Assume that the industry is initially in long-run equilibrium at the intersection of market demand curve D1 and supply curve S1, in part (b) of the figure.

Point A is on the long- run supply curve SL because it tells us that the industry will produce Q1 units of output when the long-run equilibrium price is P1.

ADVERTISEMENTS:

Suppose the market demand for the product increases unexpectedly. A typical firm is initially producing an output q1, where P1 = LMC = LAC. But the firm is also in short-run equilibrium, so that P1 = SMC. Suppose the market demand curve shifts from D1 to D2 which cuts the supply curve S1 at C. As a consequence, the price increases from P1 to P2.

Fig. 8.13(a) shows how the price increase affects a firm in the industry. When the price increases from P1 to P2 the firm follows its SMC curve and increases its output to q2 which maximises profit because it satisfies the condition that P = SMC.

If every firm responds this way, each firm will be earning a positive profit in the short-run equilibrium. This profit will be attractive to investors and will cause existing firms to expand their output and new firms to enter the market.

As a result, the short-run supply curve shifts to the right from S1 to S2 as in Fig. 8.13(b). This shift causes the market to move to a new long-run equilibrium at the intersection of D2 and S2 at B. Output must have expanded enough so that firms are earning zero profit and the incentive to enter and leave the industry disappears.

ADVERTISEMENTS:

The long-run supply curve in a constant-cost industry is a horizontal line SL as in part (b), at a price which is equal to the long-run minimum AC of production.

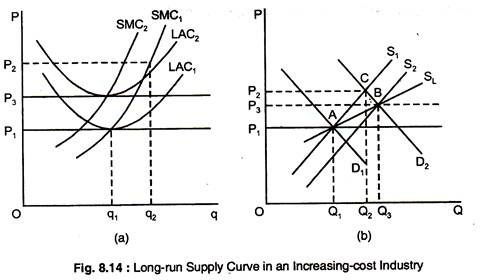

Industry in the Long-Run Supply Type # 2. Increasing-Cost Industry: Long-Run Supply Curve:

In Fig. 8.14(b), the long-run supply curve in an increasing-cost industry is an upward- sloping curve SL. When demand increases, initially causing a price rise, P2, the firms increase their output from q1 to q2 in Fig. 8.14(a). Then, new firms enter into the industry causing a shift of the supply curve to the right.

Since input prices increase as a result, the new long-run equilibrium occurs at a higher price than the initial equilibrium. In an increasing-cost industry, the long-run industry supply curve is upward-sloping. The industry produces more output, but only at a higher price needed to compensate for the increase in input costs.

Industry in the Long-Run Supply Type # 3. Decreasing-Cost Industry:

The industry supply curve can also be downward-sloping. In this case, the unexpected increase in demand causes industry output to expand as before. If industry becomes larger, it can take advantage of its scale of operation to obtain some of its input cheaply. For example, a large industry may allow for an improved transportation system or for a better, less expensive financial network.

In such a situation the firm’s AC curves shift downward, and the market price of the product falls. The lower price and the lower AC of production induce a new long-run equilibrium with more firms, a lower price and more output. Thus, in a decreasing-cost industry, the long-run supply curve is downward-sloping.

The long-run, downward-sloping supply curve also arises when expansion itself lowers input prices or when firms can use scale economies to produce at lower cost.