Read this article to learn about over hundred frequently asked questions on Producer Behaviour and Supply.

Q.1. What is meant by production?

Ans. Transformation of inputs into output is called production.

Q.2. Define Production function.

ADVERTISEMENTS:

Ans. A mathematical expression of the technological relation between physical inputs and outputs of a good.

OR

Production function represents the relationship between physical inputs used and the maximum physical output that can be produced from them during a given time period.

Q.3. Define total product.

ADVERTISEMENTS:

Ans. Total product is the total quantity of goods or services produced, by a firm with a given amount of inputs in a given period of time.

Q.4. Define Average Product.

Ans. Per unit output of a variable factor is called average product.

Q.5. What is meant by marginal physical product?

ADVERTISEMENTS:

OR

Give the meaning of marginal product.

Ans. Marginal Physical Product or ‘Marginal Product’ is the addition made to total product when an additional unit of a variable factor is employed.

Q.6. When AP falls, what is the relation between AP and MP?

Ans. When AP falls, MP curve lies below the AP .i.e. MP<AP

Q.7. Distinguish between short run and long run production function.

Ans. In short run production function some factors are fixed whereas in long run production function all factors are variable.

Q.8. As the variable input labour is increased by one unit, total output falls. What would you say about marginal productivity of labour?

Ans. If on increasing one unit of labour, total output falls, it implies that marginal product (MP) of the unit of labour employed is negative.

ADVERTISEMENTS:

Q.9. What happens to total product (TP) when the marginal product of the variable input is negative?

Ans. TP starts falling when MP becomes negative.

Q.10. What happens to TP when MP is rising?

Ans. As long as MP is rising, TP increases at an increasing rate.

ADVERTISEMENTS:

Q.11. What happens to TP when MP is declining?

Ans. When MP is falling but is positive, TP increases at a diminishing rate and when MP becomes negative, TP also starts falling.

Q.12. What happens to AP when MP is less than AP?

Ans. When MP is less than AP, AP starts falling.

ADVERTISEMENTS:

Q.13. When is TP maximum?

Ans. TP is maximum when MP=0.

Q.14. What is the shape of MP?

Ans. MP is inverted U shaped.

Q.15. What is the shape of AP?

Ans. AP is inverted U shaped.

ADVERTISEMENTS:

Q.16. When is AP maximum?

Ans. AP is maximum when MP=AP.

Q.17. When will the law of variable proportion be postponed?

Ans. The law of variable proportion will be postponed if there is an improvement in the technology or some substitutes of fixed factors are discovered.

Q.18. What is meant by economies of scale?

Ans. The advantages which a firm derives when it expands its level of production are known as economies of scale.

ADVERTISEMENTS:

Q.19. What is meant by diseconomies of scale?

Ans. Disadvantages which occur for a firm on expanding its scale of production beyond optimum level are called diseconomies of scale.

Q.20. In which stage will a rational producer try to operate in short run?

Ans. A rational producer will operate in stage of diminishing returns where TP increases at a diminishing rate.

Q.21. Define law of variable proportion.

Ans. The law states that when more & more quantities of variable inputs are mixed with fixed quantities of fixed factors of production, initially TP will increase at increasing rate, followed by increase at a diminishing rate and finally TP falls.

ADVERTISEMENTS:

Q.22. Define law of diminishing marginal product.

Ans. According to the law of diminishing marginal product, when more and more units of a variable factor are employed with other fixed factors, after a stage the marginal product of that factor starts falling.

Q.23. How can you derive TP?

Ans. TP can be derived by multiplying average product (AP) with the units employed of variable factor.

TP = AP x Quantity used of variable factor.

Q.24. What is meant by point of inflexion?

ADVERTISEMENTS:

Ans. The point where TP stops increasing at increasing rate and starts increasing at diminishing rate is called point of inflexion.

Q.25. Define Cost.

Ans. Payment made for factors of production and for non factor inputs used in the production of a commodity is called cost.

Q.26. Define fixed cost?

Ans. Fixed costs are costs that do not change with change in output.

OR

It is the costs which is incurred on fixed inputs.

Q.27. What are variable costs?

Ans. The cost which vary with the level of output of a firm are known as variable costs, i.e. the cost which change with the change in output is termed as variable costs.

Q.28. Give two examples of variable cost.

Ans. Expenditure on raw material, casual labourers etc.

Q.29. Give two examples of fixed cost.

Ans. Rent, Salary of permanent employee etc.

Q.30. Give one example each of fixed cost and variable cost.

Ans. Fixed Cost:

Rent

Variable Cost:

Expenditure on raw materials.

Q.31. What is the shape of Total Fixed Cost (TFC)?

Ans. TFC is a horizontal straight line parallel to x-axis.

Q.32. What is the shape of Total Variable Cost (TVC)?

Ans. TVC has an inverse S shape and starts from origin.

Q.33. What is the behaviour of Total Variable Cost as output increases?

Ans. TVC first increases at decreasing rate and after a point increases at an increasing rate.

Q.34. Why is the TVC inverse shaped?

Ans. IVC is inverses shaped because of law of variable proportion.

Q.35. Define Total cost.

Ans. Total cost is the sum of all costs for producing a given output.

Q.36. What can you say about the vertical distance between TVC and TC?

Ans. The distance between TVC and TC is equal to the fixed costs.

Q.37. What is the relation between AC, AFC and AVC?

Ans. Ans. AC = AFC + AVC.

Q.38. Define AFC.

Ans. AFC is the per unit fixed cost of a commodity.

Q.39. How is AFC obtained?

Ans. AFC is obtained by dividing TFC with number of units produced.

Q.40. What is the shape of AFC?

Ans. The shape of AFC curve is a rectangular hyperbola.

Q.41. What is the behaviour of average fixed cost as

Ans. AFC falls continuously

Q.42. Define AVC.

Ans. AVC is the per unit variable cost of producing a commodity.

Q.43. What is the shape of AVC?

Ans. U Shaped

Q.44. Why is AVC U shaped?

Ans. AVC is U shaped because of the law of variable proportion.

Q.45. Define Average cost (AC).

Ans. The per unit total cost of producing a commodity is called its Average Cost (AC).

Q.46. What is the shape of AC?

Ans. AC is U shaped.

Q.47. What is the reason behind U shape of AC curve?

Ans. Law of variable proportions.

Q.48. Define marginal cost.

Ans. The changes made to TC on producing an additional unit of a commodity is called marginal cost.

Q.49. What is the shape of MC curve?

Ans. The MC curve is U shaped.

Q.50. Why is the MC curve U-shaped?

Ans. MC curve is U shaped because of the law of variable proportion.

Q.51. What is the shape of TC curve?

Ans. The shape of TC curve is inverted ‘S’ shape moving upward from left to right but never starts from origin.

Q.52. What happens to TVC when MC declines?

Ans. TVC rises at diminishing rate when MC declines.

Q.53. What will be the behaviour of TVC when MC rises?

Ans. TVC will rise at an increasing rate when MC rises.

Q.54. How are TVC and MC related?

Ans. TVC is equal to the sum of MC i.e. TVC = ZMC.

Q.55. What will happen to AC when MC is below it?

Ans. AC will fall when MC is below it.

Q.56. What will be the position of MC when AC rises?

Ans. MC will be more than AC when AC is rising.

Q.57. When is MC=AC?

Ans. At the minimum point of AC, MC will be equal to AC.

Q.58. What is LMC?

Ans. LMC is the addition made to total cost when an additional unit of the commodity is produced.

Q.59. How is MC derived from TVC?

Ans. MC = TVCn – TVCn-3.

Q.60. What are supplementary costs?

Ans. Fixed costs are known as supplementary costs which do not change with the level of output of the firm.

Q.61. Can AFC ever be zero?

Ans. No, AFC can never be zero.

Q.62. Why are long run cost curves U shaped?

Ans. Long run cost curves are U shaped because of the law of returns to scale.

Q.63. Can there be some fixed costs in the long run? If not why so?

Ans. There cannot be any fixed cost in the long run because all factors are variable in the long run.

Q.64. Minimum Telephone Bill is a fixed cost or variable cost ?

Ans. Fixed Cost

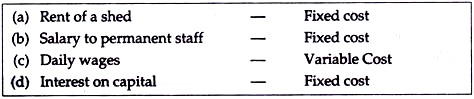

Q.65. Categories these as fixed cost or variable cost

Ans.

Q.66. Name the cost that does exist at zero level too?

Ans. Total Fixed Cost

Q.67. Name the curve which cuts ATC & AVC at their lowest point?

Ans. Marginal cost curve.

Q.68. Other name given to Fixed Cost

Ans. Overhead cost

Q.69. Supplementary cost is the other name given to?

Ans. Fixed cost

Q.70. Prime cost is the other name given to?

Ans. Variable cost

Q.71. Other name given to variable cost?

Ans. Direct cost

Q.72. Other name given to Rising portion of MC?

Ans. Supply curve of a firm.

Q.73. Area under MC curve is known as?

Ans. TVC

Q.74. Define Revenue.

Ans. Money receipts from sale of a product by the seller are called revenue.

Q.75. Define total revenue.

Ans. Total revenue is the total money receipt from sale of a given output in the market.

Q.76. Define average revenue.

Ans. Per unit revenue received from sale of a commodity is known as Average Revenue.

Q.77. How is AR obtained?

Ans. AR can be obtained by dividing the TR with number of units sold.

Q.78. What is the behaviour of average revenue in a market in which a firm can sell more only by lowering the price?

Ans. AR continuously falls as output increases.

Q.79. Define marginal revenue.

Ans. Marginal revenue is the addition to the total revenue when an additional unit of a commodity is sold.

Q.80. What is the relationship between price line and total revenue?

Ans. Total revenue is the area under the price line, in a perfectly competitive market

Q.81. What is the relation between AR and MR of a perfectly competitive firm.

Ans. In case of a perfectly competitive firm AR = MR.

Q.82. What is the elasticity of demand curve of monopoly firm?

Ans. The demand curve of a monopoly firm is less than unit elastic.

Q.83. What is the elasticity of demand curve of a firm under monopolistic competition?

Ans. The demand curve of a firm under monopolistic competition is more than unit elastic.

Q.84. What is the elasticity of demand curve of a firm under perfect competition?

Ans. The demand curve of a firm under perfect competition is perfectly elastic.

Q.85. How is TR obtained?

Ans. TR is obtained by multiplying quantity sold with the price of the product.

Q.86. What will be the elasticity of demand if MR = zero?

Ans. Elasticity of demand is unity when MR = zero.

Q.87. Name the market where AR & MR curve coincide with each other?

Ans. Perfect competition.

Q.88. What will be the position of MR when TR is maximum?

Ans. MR is zero when TR is maximum.

Q.89. What is the behaviour of Marginal Revenue in a market in which a firm can sell any quantity of the output it produces at a given price?

Ans. MR is constant at all levels of output.

Q.90. What will happen to TR when MR is negative?

Ans. The TR will decline when MR is negative.

Q.91. When AR is downward sloping, what is the status of MR?

Ans. When AR is downward sloping, MR lies below it.

Q.92. If TR is increasing at a constant rate, what will be the effect on MR?

Ans. MR will be positive and constant.

Q.93. What is the shape of AR curve in monopoly?

Ans. AR curve of a monopoly firm will be downward sloping.

Q.94. What is the shape of MR curve in monopoly?

Ans. MR curve of a monopoly firm is downward sloping and lies below the AR curve.

Q.95. In what type of market can MR never be negative?

Ans. MR curve can never be negative under perfect competition.

Q.96. What is the shape of MR curve under perfect competition?

Ans. MR curve of a firm under perfect competition is a horizontal line parallel to x-axis.

Q.97. Who is a producer?

Ans. Any economic unit which produces goods and services for sale is a producer.

Q.98. Define profit.

Ans. The profit is the difference between total revenue and total cost.

Q.99. What is the objective of a producer?

Ans. The objective of a producer is to earn maximum profits.

Q.100. What is the breakeven point?

Ans. Breakeven point is the state of no profit no loss. i.e. TR-TC=0

Q.101. What is the meaning of producer’s equilibrium?

Ans. A producer is at equilibrium when he is producing at the level of maximum profit.

Q.102. What is a unit tax?

Ans. A unit tax is a tax which is imposed by the government on per unit sale of the product.

Q.103. At what level will a producer be at equilibrium under TR – TC approach?

Ans. The level of output at which the vertical distance between TR and TC is maximum will be the equilibrium level of output for the firm.

Q.104. What is the condition for producer’s equilibrium under MR – MC approach?

Ans. Ans. MR = MC and MC should be rising.

Q.105. What is the shape of AR of a monopoly firm?

The AR curve or demand curve of a monopoly firm is downward sloping.

Q.106. What is the shape of MR curve under imperfect market situation?

Ans. The MR curve slopes downward under imperfect market conditions.

Q.107. At what rate does MR curve fall?

Ans. MR curve falls at twice the rate of the AR curve.

Q.108. What is the long run supply curve of a firm?

Ans. The rising portion of MC starting from the minimum point of long run AC is the long run supply curve of a firm.

Q.109. When does a firm earn profit?

Ans. A firm earns profit when TR > TC.

Q.110. When will a firm incur losses?

Ans. A firm will incur losses when TR < TC.

Q.111. When does a firm choose to produce in-spite of earning losses?

Ans. A firm will choose to produce in-spite of losses if at least its variable cost is covered by the price.

Q.112. What is shut down point?

Ans. Shut down point is a situation when the price does not cover even the variable cost.

Q.113. Name different forms of imperfect competition?

Ans. (a) Monopolistic

(b) Oligopoly

Q.114. Define supply.

Ans. Supply means the quantity of a good which a firm (or industry) is willing to supply at a given price during a period of time.

Q.115. Define market supply.

Ans. Market supply is the total quantity of a good which is offered for sale by all the firms at a particular price in a given time period.

Q.116. What is meant by price elasticity of supply?

Ans. The degree of change in quantity supplied of a commodity due to change in its price is called price elasticity of supply.

Q.117. State the law of supply.

Ans. Law of supply states that if other things remain constant, supply is more at a higher price and it is less at a lower price or supply is directly related to the price of a commodity.

Q.118. Define a supply schedule.

Ans. Supply schedule is a tabular statement which shows different quantities supplied of a commodity at different level of prices.

Q.119. Define a supply curve.

Ans. A supply curve shows various quantities supplied of a commodity at different levels of prices graphically.

Q.120. Define market supply schedule.

Ans. Market supply schedule is a tabular statement showing different quantities supplied of a commodity by all the firms at different levels of prices.

Q.121. What is meant by change in supply?

Ans. A rise or fall in quantity supplied of a commodity due to factors other than price of the commodity is called change in supply.

Q.122. Give meaning of change in quantity supplied?

Ans. A rise or fall in the quantity supplied of a commodity due to change in price of the commodity, keeping other factors constant is called change in quantity supplied.

Q.123. What is the meaning of expansion of supply?

Ans. A rise in quantity supplied due to increase in the price of the commodity, keeping other factors constant is called expansion of supply.

Q.124. What is the meaning of contraction of supply?

Ans. A fall in quantity supplied due to the fall in price of the commodity, keeping other factors constant is called contraction of supply.

Q.125. What causes a downward movement along a supply curve?

Ans. A decrease in price of commodity leads to downward movement along its supply curve keeping other factors constant.

Q.126. What causes an upward movement along the supply curve of a commodity?

Ans. A rise in price of the commodity would lead to an upward movement along its supply curve, keeping other factors constant.

Q.127. What causes a movement along the supply curve of a commodity?

A movement along the supply curve is caused by only change in price of the commodity keeping other factors constant.

Q.128. What is meant by increase in supply?

A rise in the quantity of supply of a commodity due to factors other than the price of commodity, is called increase in supply.

Q.129. When does a supply curve shift?

When factors other than the own price of the good change, the supply curve shifts.

Q.130. What is ‘Change in Supply’?

Ans. Change in supply due to the change in own price of that good.

Q.131. What is ‘decrease’ in supply?

Ans. A fall in the supply due to factors, other than the own price of the commodity is known as decrease in supply.

Q.132. Mention one factor that causes rightward shift of the supply curve.

Ans. Improvement in technology.

Q.133. Explain the effect of technique of production on the elasticity.

Ans. Supply will be more elastic when techniques used for production is simple and less elastic when complicated methods of techniques are used for production of the commodity.

Q.134. Define perfectly elastic supply.

Ans. When there is an infinite change in the quantity supplied of a commodity, with price remaining constant, supply is perfectly elastic.

Q.135. Define perfectly inelastic supply curve

Ans. A perfectly inelastic supply curve will be a vertical straight line parallel to Y axis, showing that a fixed quantity will be supplied, whatever be the price.

Q.136. What is the term used for a situation when elasticity of supply is between zero and one?

Ans. The supply will be called relatively inelastic.

Q.137. Distinguish between stock and supply.

Ans. Stock is the total quantity available with a producer whereas supply is that part of stock which he is ready to sell at a given price in a given period of time.

Q.138. Price elasticity of supply of a commodity is 1.2. Is its supply elastic or inelastic and why?

Ans. Supply is elastic since coefficient of elasticity of supply is more than one.

Q.139. Define market period.

Ans. Market period is that period in which the supply of a commodity is perfectly inelastic. This is also known as very short period.

Q.140. What is the price elasticity of supply of a straight line supply curve touching the Y axis.

Ans. The elasticity of supply of a supply curve touching Y-axis will be greater than one.

Q.141. Draw a straight line supply curve with infinite price elasticity.

Ans.

Q.142. Give the formula for measuring elasticity of supply?

Ans. The elasticity of supply can be measured with the help of the following formula:

![]()

Q.143. If two supply curves intersect each other, which curve will be having higher elasticity at the point of intersection.

Ans. Flatter curve will have higher elasticity.

Q. 144. Can there be some fixed cost in the long run? If not, why?

Ans. No, there can never be any fixed cost in the long run as in the long run all factors are anyway variable in nature.

Q.145. How does technological progress affect the supply curve of a firm?

Ans. Technical progress will result in increase in production, thus MC will be reduce which will increase the supply. The supply curve will thus shift to the right.

Q.146 .How an increase in the price of an input affect the supply curve of a firm?

Ans. Increase in the price of an input will increase the cost of production of the commodity. The profitability will be reduced. Thus the supply will decrease and the supply curve will shift to the left.