In this article we will discuss about:- 1. Fisher’s Equation of Exchange 2. Assumptions of Fisher’s Quantity Theory 3. Conclusions 4. Criticisms 5. Merits 6. Implications 7. Examples.

Fisher’s Equation of Exchange:

The transactions version of the quantity theory of money was provided by the American economist Irving Fisher in his book- The Purchasing Power of Money (1911). According to Fisher, “Other things remaining unchanged, as the quantity of money in circulation increases, the price level also increases in direct proportion and the value of money decreases and vice versa”.

Fisher’s quantity theory is best explained with the help of his famous equation of exchange:

MV = PT or P = MV/T

ADVERTISEMENTS:

Like other commodities, the value of money or the price level is also determined by the demand and supply of money.

i. Supply of Money:

The supply of money consists of the quantity of money in existence (M) multiplied by the number of times this money changes hands, i.e., the velocity of money (V). In Fisher’s equation, V is the transactions velocity of money which means the average number of times a unit of money turns over or changes hands to effectuate transactions during a period of time.

Thus, MV refers to the total volume of money in circulation during a period of time. Since money is only to be used for transaction purposes, total supply of money also forms the total value of money expenditures in all transactions in the economy during a period of time.

ADVERTISEMENTS:

ii. Demand for Money:

Money is demanded not for its own sake (i.e., for hoarding it), but for transaction purposes. The demand for money is equal to the total market value of all goods and services transacted. It is obtained by multiplying total amount of things (T) by average price level (P).

Thus, Fisher’s equation of exchange represents equality between the supply of money or the total value of money expenditures in all transactions and the demand for money or the total value of all items transacted.

Supply of money = Demand for Money

ADVERTISEMENTS:

Or

Total value of money expenditures in all transactions = Total value of all items transacted

MV = PT

or

P = MV/T

Where,

M is the quantity of money

V is the transaction velocity

P is the price level.

ADVERTISEMENTS:

T is the total goods and services transacted.

The equation of exchange is an identity equation, i.e., MV is identically equal to PT (or MV = PT). It means that in the ex-post or factual sense, the equation must always be true. The equation states the fact that the actual total value of all money expenditures (MV) always equals the actual total value of all items sold (PT).

What is spent for purchases (MV) and what is received for sale (PT) are always equal; what someone spends must be received by someone. In this sense, the equation of exchange is not a theory but rather a truism.

Irving Fisher used the equation of exchange to develop the classical quantity theory of money, i.e., a causal relationship between the money supply and the price level. On the assumptions that, in the long run, under full-employment conditions, total output (T) does not change and the transactions velocity of money (V) is stable, Fisher was able to demonstrate a causal relationship between money supply and price level.

ADVERTISEMENTS:

In this way, Fisher concludes, “… the level of price varies directly with the quantity of money in circulation provided the velocity of circulation of that money and the volume of trade which it is obliged to perform are not changed”. Thus, the classical quantity theory of money states that V and T being unchanged, changes in money cause direct and proportional changes in the price level.

Irving Fisher further extended the equation of exchange so as to include demand (bank) deposits (M’) and their velocity, (V’) in the total supply of money.

Thus, the equation of exchange becomes:

ADVERTISEMENTS:

Thus, according to Fisher, the level of general prices (P) depends exclusively on five definite factors:

(a) The volume of money in circulation (M);

(b) Its velocity of circulation (V) ;

(c) The volume of bank deposits (M’);

(d) Its velocity of circulation (V’); and

(e) The volume of trade (T).

ADVERTISEMENTS:

The transactions approach to the quantity theory of money maintains that, other things remaining the same, i.e., if V, M’, V’, and T remain unchanged, there exists a direct and proportional relation between M and P; if the quantity of money is doubled, the price level will also be doubled and the value of money halved; if the quantity of money is halved, the price level will also be halved and the value of money doubled.

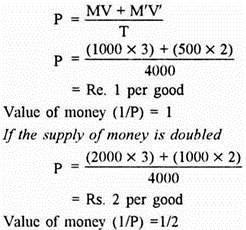

Fisher’s quantity theory of money can be explained with the help of an example. Suppose M = Rs. 1000. M’ = Rs. 500, V = 3, V’ = 2, T = 4000 goods.

Thus, when money supply in doubled, i.e., increases from Rs. 4000 to 8000, the price level is doubled. i.e., from Re. 1 per good to Rs. 2 per good and the value of money is halved, i.e., from 1 to 1/2.

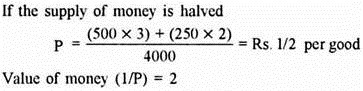

Thus, when money supply is halved, i.e., decreases from Rs. 4000 to 2000, the price level is halved, i.e., from 1 to 1/2, and the value of money is doubled, i.e., from 1 to 2.

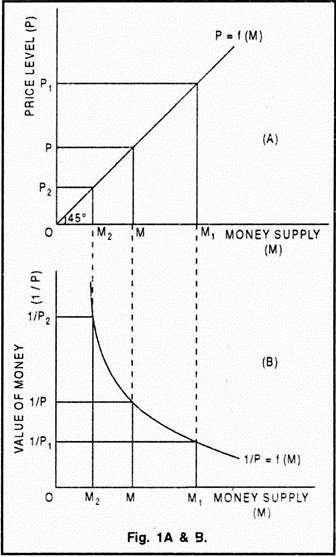

The effects of a change in money supply on the price level and the value of money are graphically shown in Figure 1-A and B respectively:

(i) In Figure 1-A, when the money supply is doubled from OM to OM1, the price level is also doubled from OP to OP1. When the money supply is halved from OM to OM2, the price level is halved from OP to OP2. Price curve, P = f(M), is a 45° line showing a direct proportional relationship between the money supply and the price level.

(ii) In Figure 1-B, when the money supply is doubled from OM to OM1; the value of money is halved from O1/P to O1/P1 and when the money supply is halved from OM to OM2, the value of money is doubled from O1/P to O1/P2. The value of money curve, 1/P = f (M) is a rectangular hyperbola curve showing an inverse proportional relationship between the money supply and the value of money.

Assumptions of Fisher’s Quantity Theory:

Fisher’s transactions approach to the quantity theory of money is based on the following assumptions:

1. Constant Velocity of Money:

ADVERTISEMENTS:

According to Fisher, the velocity of money (V) is constant and is not influenced by the changes in the quantity of money. The velocity of money depends upon exogenous factors like population, trade activities, habits of the people, interest rate, etc. These factors are relatively stable and change very slowly over time. Thus, V tends to remain constant so that any change in supply of money (M) will have no effect on the velocity of money (V).

2. Constant Volume of Trade or Transactions:

Total volume of trade or transactions (T) is also assumed to be constant and is not affected by changes in the quantity of money. T is viewed as independently determined by factors like natural resources, technological development, population, etc., which are outside the equation and change slowly over time. Thus, any change in the supply of money (M) will have no effect on T. Constancy of T also means full employment of resources in the economy.

3. Price Level is a Passive Factor:

According to Fisher the price level (P) is a passive factor which means that the price level is affected by other factors of equation, but it does not affect them. P is the effect and not the cause in Fisher’s equation. An increase in M and V will raise the price level. Similarly, an increase in T will reduce the price level.

4. Money is a Medium of Exchange:

ADVERTISEMENTS:

The quantity theory of money assumed money only as a medium of exchange. Money facilitates the transactions. It is not hoarded or held for speculative purposes.

5. Constant Relation between M and M’:

Fisher assumes a proportional relationship between currency money (M) and bank money (M’). Bank money depends upon the credit creation by the commercial banks which, in turn, are a function of the currency money (M). Thus, the ratio of M’ to M remains constant and the inclusion of M’ in the equation does not disturb the quantitative relation between quantity of money (M) and the price level (P).

6. Long Period:

The theory is based on the assumption of long period. Over a long period of time, V and T are considered constant.

Thus, when M’, V, V’ and T in the equation MV + M’Y’ = PT are constant over time and P is a passive factor, it becomes clear, that a change in the money supply (M) will lead to a direct and proportionate change in the price level (P).

Broad Conclusions of Fisher’s Quantity Theory:

(i) The general price level in a country is determined by the supply of and the demand for money.

(ii) Given the demand for money, changes in money supply lead to proportional changes in the price level.

(iii) Since money is only a medium of exchange, changes in the money supply change absolute (nominal), and not relative (real), prices and thus leave the real variables such as employment and output unaltered. Money is neutral.

(iv) Under the equilibrium conditions of full employment, the role of monetary (or fiscal) policy is limited.

(v) During the temporary disequilibrium period of adjustment, an appropriate monetary policy can stabilise the economy.

(vi) The monetary authorities, by changing the supply of money, can influence and control the price level and the level of economic activity of the country.

Criticisms of Quantity Theory of Money:

The quantity theory of money as developed by Fisher has been criticised on the following grounds:

1. Interdependence of Variables:

The various variables in transactions equation are not independent as assumed by the quantity theorists:

(i) M Influences V – As money supply increases, the prices will increase. Fearing further rise in price in future, people increase their purchases of goods and services. Thus, velocity of money (V) increases with the increase in the money supply (M).

(ii) M Influences V’ – When money supply (M) increases, the velocity of credit money (V’) also increases. As prices increase because of an increase in money supply, the use of credit money also increases. This increases the velocity of credit money (V’).

(iii) P Influences T – Fisher assumes price level (P) as a passive factor having no effect on trade (T). But, in reality, rising prices increase profits and thus promote business and trade.

(iv) P Influences M – According to the quantity theory of money, changes in money supply (M) is the cause and changes in the price level (P) is the effect. But, critics maintain that a change in the price level occurs independently and this later on influences money supply.

(v) T Influences V – If there is an increase in the volume of trade (T), it will definitely increase the velocity of money (V).

(vi) T Influences M – During prosperity growing volume of trade (T) may lead to an increase in the money supply (M), without altering the prices.

(vii) M and T are not Independent – According to Keynes, output remains constant only under the condition of full employment. But, in reality less-than-full employment prevails and an increase in the money supply increases output (T) and employment.

2. Unrealistic Assumption of Long Period:

The quantity theory of money has been criticised on the ground that it provides a long-term analysis of value of money. It throws no light on the short-run problems. Keynes has aptly remarked that “in the long-run we are all dead”. Actual problems are short-run problems. Thus, quantity theory has no practical value.

3. Unrealistic Assumption of full Employment:

Keynes’ fundamental criticism of the quantity theory of money was based upon its unrealistic assumption of fall employment. Full employment is a rare phenomenon in the actual world. In a modern capitalist economy, less than full employment and not full employment is a normal feature. According to Keynes, as long as there is unemployment, every increase in money supply leads to a proportionate increase in output, thus leaving the price level unaffected.

4. Static Theory:

The quantity theory assumes that the values of V, V’, M’ and T remain constant. But, in reality, these variables do not remain constant. The assumption of constancy of these factors makes the theory a static theory and renders it inapplicable in the dynamic world.

5. Simple Truism:

The equation of exchange (MV = PT) is a mere truism and proves nothing. It is simply a factual statement which reveals that the amount of money paid in exchange for goods and services (MV) is equal to the market value of goods and services received (PT), or, in other words, the total money expenditure made by the buyers of commodities is equal to the total money receipts of the sellers of the commodities. The equation does not tell anything about the causal relationship between money and prices; it does not indicate which the cause is and which is the effect.

6. Technically Inconsistent:

Prof. Halm considers the equation of exchange as technically inconsistent. M in the equation is a stock concept; it refers to the stock of money at a point of time. V, on the other hand, is a flow concept, it refers to velocity of circulation of money over a period of time, M and V are non-comparable factors and cannot be multiplied together. Hence the left-hand side of the equation MV = PT is inconsistent.

7. Fails to Explain Trade Cycles:

The quantity theory does not explain the cyclical fluctuations in prices. It does not tell why during depression the prices fall even with the increase in the quantity of money and during the boom period the prices continue to rise at a faster rate in spite of the adoption of tight money and credit policy.

The proper explanation for the decline.in prices during depression is the fall in the velocity of money and for the rise in prices during boom period is the increase in the velocity of money. Thus, the quantity theory of money fails to explain the trade cycles. Crowther has remarked, “The quantity theory is at best, an imperfect guide to the causes of the cycle.”

8. Ignores Other Determinants of Price Level:

The quantity theory maintains that price level is determined by the factors included in the equation of exchange, i.e. by M, V and T, and unrealistically establishes a direct and proportionate relationship between the quantity of money and the price level. It ignores the importance of many other determinates of prices, such as income, expenditure, investment, saving, consumption, population, etc.

9. Fails to Integrate Monetary Theory with Price Theory:

The classical quantity theory falsely separates the theory of value from the theory of money. Money is considered neutral and changes in money supply are believed to affect the absolute prices and not relative prices. Keynes criticises this view and maintains that money plays an active role and both the theory of money and the theory of value are essential parts of the general theory of output, employment and money. He integrated the two theories through the rate of interest.

10. Money as a Store of Value Ignored:

The quantity theory of money considers money only as a medium of exchange and completely ignores its importance as a store of value. Keynes recognised the stores of value function of money and laid emphasis on the demand for money for speculative purpose as against the classical emphasis on the transactions and precautionary demand for money.

11. No Discussion of Velocity of Money:

The quantity theory of money does not discuss the concept of velocity of circulation of money, nor does it throw light on the factors influencing it. It regards the velocity of money to be constant and thus ignores the variation in the velocity of money which are bound to occur in the long period.

12. One-Sided Theory:

Fisher’s transactions approach is one- sided. It takes into consideration only the supply of money and its effects and assumes the demand for money to be constant. It ignores the role of demand for money in causing changes in the value of money.

13. No Direct and Proportionate Relation between M and P:

Keynes criticised the classical quantity theory of money on the ground that there is no direct and proportionate relationship between the quantity of money (M) and the price level (P). A change in the quantity of money influences prices indirectly through its effects on the rate of interest, investment and output.

The effect on prices is also not predictable and proportionate. It all depends upon the nature of the liquidity preference function, the investment function and the consumption function. The quantity theory does not explain the process of causation between M and P.

14. A Redundant Theory:

The critics regard the quantity theory as redundant and unnecessary. In fact, there is no need of a separate theory of money. Like all other commodities, the value of money is also determined by the forces of demand and supply of money. Thus, the general theory of value which explains the value determination of a commodity can also be extended to explain the value of money.

15. Crowther’s Criticism:

Prof. Crowther has criticised the quantity theory of money on the ground that it explains only ‘how it works’ of the fluctuations in the value of money and does not explain ‘why it works’ of these fluctuations. As he says, “The quantity theory can explain the ‘how it works’ of fluctuations in the value of money… but it cannot explain the ‘why it works’, except in the long period”.

Merits of Quantity Theory of Money:

Despite many drawbacks, the quantity theory of money has its merits:

1. Correct in Broader Sense:

It is true that in its strict mathematical sense (i.e., a change in money supply causes a direct and proportionate change in prices), the quantity theory may be wrong and has been rejected both theoretically and empirically. But, in the broader sense, the theory provides an important clue to the fluctuations in prices. Nobody can deny the fact that most of the changes in the prices of the commodities are due to changes in the quantity of money.

2. Validity of the Theory:

Till 1930s, the quantity theory of money was used by the economists and policy makers to explain the changes in the general price level and to form the basis of monetary policy. A number of historical instances like hyper- inflation in Germany in 1923-24 and in China in 1947-48 have proved the validity of the theory. In these cases large issues of money pushed up prices.

3. Basis of Monetary Policy:

The theory forms the basis of the monetary policy. Various instruments of credit control, like the bank rate and open market operations, presume that large supply of money leads to higher prices. Cheap money policy is advocated during depression to raise prices.

4. Revival of Quantity Theory:

In the recent times, the monetarists have revived the classical quantity theory of money. Milton Friedman, the leading monetarist, is of the view that the quantity theory was not given full chance to fight the great depression 1929-33; there should have been the expansion of credit or money or both.

He believes that the present inflationary rise in prices in most of the countries of the world is because of expansion of money supply much more than the expansion in real income. The proper monetary policy is to allow the money supply to grow in line with the growth in the country’s output.

Implications of Quantity Theory of Money:

Various theoretical and policy implications of the quantity theory of money are given below:

1. Proportionality of Money and Prices:

The quantity theory of money leads to the conclusion that the general level of prices varies directly and proportionately with the stock of money, i.e., for every percentage increase in the money stock, there will be an equal percentage increase in the price level. This is possible in an economy – (a) whose internal mechanism is capable of generating a full-employment level of output, and (b) in which individuals maintain a fixed ratio between their money holdings and money value of their transactions.

2. Neutrality of Money:

The quantity theory of money justifies the classical belief that money is neutral’ or ‘money is a veil’ or ‘money does not matter’. It implies that changes in the money supply are neutral in the sense that they affect the absolute prices and not the relative prices. Since, consumer spending and business spending decisions depend upon relative prices; changes in the money supply do not affect real variables such as employment and output. Thus, money is neutral.

3. Dichotomisation of the Price Process:

The quantity theory also justifies the dichotomisation of the price process by the classical economists into its real and monetary aspects. The relative (or real) prices are determined in the commodity markets and the absolute (or nominal) prices in the money market. Since money is neutral and changes in money supply affect only the monetary and not the real phenomena, the classical economists developed the theory of employment and output entirely in real terms and separated it from their monetary theory of absolute prices.

4. Monetary Theory of Prices:

The quantity theory of money upholds the view that the general level of prices is mainly a monetary phenomenon. The non-monetary factors, like taxes, prices of imported goods, industrial structure, etc., do not have lasting influence on the price level. These factors may raise the prices in the short run, but this price rise will reduce actual money balances below their desired level. This will lead to fall in money spending and a consequent fall in the price level until the original price is restored.

5. Role of Monetary Policy:

In a self-adjusting free-market economy in which changes in money supply do not affect the real macro variables of employment and output, there is little room left for a monetary policy. But the classical economists recognised the existence of frictional unemployment which represents temporary disequilibrium situation.

Such a situation arises when wages and prices are rigid downward. To me such a situation of unemployment, the classical economists advocated a stabilising monetary policy of increasing money supply. An increase in the money supply increases total spending and the general price level.

Wage will rise less rapidly (or relative wages will fall) in the labour surplus areas, thereby reducing unemployment Thus, through a judicious use of monetary policy, the time lag between disequilibrium and adjustment can shortened; or, in the case of frictional unemployment, the duration of unemployment can be reduce. Thus, the classical economists assigned a modest stabilising role to monetary policy to deal with the disequilibrium situation.