Here is a term paper on ‘Futures’. Find paragraphs, long and short term papers on ‘Futures’ especially written for school and college students.

Term Paper on Futures

Term Paper # 1. Introduction to Futures:

Futures trading in stock and shares were prohibited in India for a long time, until March 1995, when they were permitted again along with options. Futures, in commodities like cotton, jute, tea, tobacco, etc., have been in vogue. For example, Cochin pepper Aug. 1996 was quoted at Rs. 7,400/7,410 while the same for Oct 1996 was Rs. 7,700/7,645 (quotation on July 3, 1996). Generally, these quotations are available for one to three months futures delivery, based on their present quotations and expected future demand and supply position and stock position.

A futures contract is a firm legal commitment between a buyer and seller in which they agree to exchange something say pepper for a specified money at the end of a designated time period, say three months hence. Delivery is necessary and the price is known in advance. The risk is borne by both buyer and seller. Only the risk of uncertainty is not there for the buyer, as the seller bears it, for a reward.

ADVERTISEMENTS:

The possible risk attached to the upward and downward changes in the actual price at the future stipulated time is there for both buyer and seller. If prices fall below the stipulated price, the buyer loses and if they rise above the stipulated price, the seller loses due the contracted stipulated price. The loss of one is the gain of the other and it is a zero sum game. Here in lies the speculative element in futures.

Futures Differ from Options:

In options, the deliver is optional for buyer but obligatory for seller of the option. The buyer pays the seller a premium in the beginning itself while there is no premium paid on the future contract. Future contracts can be performed only at the settlement date but not before that. The buyer of the options has a right to exercise the option either at the expiration date or prior to that. Deliveries and execution of contracts are enforced by the organizing authorities.

Term Paper # 2. Index Futures:

Suppose the future contracts are based NSE Index. The NSE 50 is quoting say at 1,200. Each point in the index is valued at Rs. 50, one futures contract on NSE. Index will cost Rs. 60,000; if at the end of one month, the index rose to 1,220, then on the settlement day a cash payment of Rs. 50 × 20 = Rs. 1,000 is to be paid by the seller to the buyer. All the traders in the futures are to be members and each trader is expected to put in “good faith” margin deposit depending upon the value of the total contracts. These margin moneys are marked to the market value on a daily basis. The margins to be kept on futures are less than for normal deliveries, as index futures do not involve full value payments.

ADVERTISEMENTS:

Thus, an index futures contract is an obligation to deliver at settlement an amount of cost, equal to a number of times (say 100 or 500) of the difference between the stock index value at the close of the last trading day (1,220) of the contract and the price at which the future contract was originally struck (1,200). The terms of the contract, underlying the futures trading will determine the number of times the difference is to be multiplied.

Margin money has to be kept and other conditions are to be observed for any contingent event of failure to make the additional deposit marked to the market value of the contract and the possible failure to honour the contract by either party. The trading hours, and contracts months (normally 3, 6, 9 and 12 months are allowed) minimum price fluctuation and the last day of trading and settlement date etc., are all set out in the original futures trading system; as laid down by the controlling authority, say the NSE authorities, as per the SEBI guidelines.

Valuation of Index Futures:

If an investor invests in BSE 30 index he will collect dividends on the scrips he holds and his principal value may go up or down depending on the index. In the case of the futures index, the investor will get the same outcome as if he invests all his money in riskless treasury bills and enters into a futures contract for future delivery of the index. The futures then must sell at a price equal to today’s price of the index plus a premium equal to risk free return plus dividend on the index shares.

ADVERTISEMENTS:

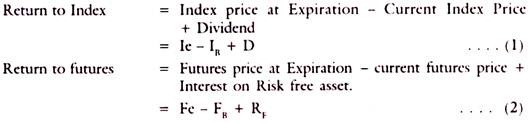

To show this symbolically let Fe be the price of the futures, FB is today’s price of futures IB current price of the Index and D is dividend on the index shares, and IE is the index price at the expiration date.

As IE will equal Fe at expiration, using the above equations, we can derive, FC as = IB + (RF – D).

The above equation means that the present price of futures, will equal present price of Index plus the “cost of carry”, which equals (Rf – D), namely, the interest obtainable on risk-free asset (Rf) minus dividend on Index Shares (D). The cost of purchasing the Index Shares is substantially higher than the cost of buying the futures contract for the same index.

The money used to buy the futures will involve interest cost and by not buying the shares, dividends are lost. Assume that the money used to purchase the index shares is invested in Treasury bills to give risk free return (Rf). If Rf is less than the dividends lost, the futures price will be below the Index price (that is FB< IB) and (RF< D).

Arbitrage or Basis Trading:

Arbitrage is the simultaneous purchase and sale of the same commodity in two different markets in order to make profits from the price difference between the two markets. Inter-market differentials are eliminated by operations of the Arbitrage.

Thus, stock index futures arbitrage involves the buying of a basket of stocks and selling futures when mispricing is perceived by the investor or the reverse operation of the same. These operations require expertise in program trading and a large amount of capital to be used. Arbitrage reduces the risk involved in markets by lowering and eliminating the price differential as between markets.

Hedging:

ADVERTISEMENTS:

Hedging occurs mostly in treasury bill futures markets to reduce the risk of the portfolio which may be an existing investment in money market or anticipated future investment. The exposure to interest rate risk depends on the mismatch of assets and liabilities of short-term nature. Specific or general interest rate risk exposure can be covered by the futures in treasury bills.

The major use of the futures market lay either in the risk coverage of the specific market risk or the interest rate risk. The most common way of covering the interest rate risk is to hedge on Treasury bill futures. A short position in futures will cover the long position in the spot market.

Example of Topix Price Index Futures:

We do not have futures on shares and securities in India to illustrate stock index future, let us therefore take the Topix futures of Tokyo stock exchange.

ADVERTISEMENTS:

The terms of the futures contracts are generally as follows:

Contracts are based on Topix-Tokyo stock price index, covering all shares listed in first section of T.S.E. It represents the market as a whole, comprehensive and weighted by the number of shares outstanding in each stock and is quoted even’ minute of trading session and is the most suitable bench mark for behaviour of the market.

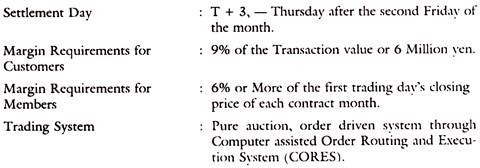

Contract Months:

March, June, September, December — four contract months are traded at all times covering exactly 15 months at any time. Basic trading unit is yen 10,000 times Topix Point (decimals not considered). Minimum price change- one full point in Topix value of minimum Move = 10,000 yen. Daily price limit- Around 3% an either side, last trading day- Trading starts on the second Friday in each new contract month and last trading day is the second Friday of the succeeding month.

ADVERTISEMENTS:

Term Paper # 3. Futures and Speculation:

Longs and shorts take positions in the futures markets. Being a zero-sum game, the loss of one set is a gain of another set. As such it is pure speculation, based on the expectation of the spot price of an asset security or index on the delivery date. The longs in a futures contract gains, if the observed spot price on the delivery date is greater than the expected spot price that has reflected in the futures price of the asset or index at the time of initiation. Correspondingly, those in the short position in the futures gain, when the observed spot price on the delivery date is lower than the expected spot price at that date.

All members in futures trading are controlled by the exchange authorities as per the terms of the contracts. Margins are collected from members as well as their customers and these margins are marked to daily market values. The clearing house of the exchange become the counter party to ensure orderly trading and default-free system. For the buyer, the exchange becomes the seller and for the seller, the exchange is the buyer.

Term Paper # 4. Advantages of Futures Index:

It is a risk hedge and caters to speculative instinct of investors. It is a more efficient method of controlling risk on a portfolio, as it reduces the transactions costs, trading costs and price pressure. Neither the buyer nor the seller pays the full value of the underlying assets but deals only in differences, in cash without involving delivery of the assets. The futures smoothens the asset reallocation, provides hedge to future inflows or outflows of cash and reduces the impact of bullish and bearish trading as futures do not involve full payment or receipt of the underlying assets but is a dealing in differences.

1. Operation of Hedge of Risk:

To illustrate the coverage of risk, assume that you expect a future cash inflow of Rs. 50,000 a month hence, which you wish to invest in equities. But the market is bullish and prices are expected to rise. Then you buy an index future contract to cover the expected rise in price. You can also sell short if the market is expected to fall in prices. Suppose, you have the securities in your portfolio and expect the market to fall then you can sell the futures, instead of the securities. If the actual fall is more than the expected price, you will receive the difference in cash.

ADVERTISEMENTS:

A bullish expectation makes you buy the futures contract and a bearish expectation makes you sell the futures contract. If your expectations are correctly realised, you can make money on the deals without actually buying and selling the underlying securities. This will enable you to trade on a smaller investment as the margins you have to keep for trading in Futures is generally 6 to 10%, and the loss of interest money is less expensive than the loss of interest on a bigger outlay involved in buying and selling for deliveries of underlying securities or shares or bonds.

2. Futures on Bonds:

While stock index futures provide low cost and efficient method of insuring against systematic risk of the portfolio, futures on bonds and Treasury bills provide the risk coverage to interest rate risk, which is the largest source of systematic risk in holding fixed income securities.

In the case of index futures, delivery is in cash settlements only but in the case of futures on Treasury bills or bonds, delivery is in bills or bonds. In the U.S.Treasury Note futures are more popular and easy to understand and operate. These contracts are available for delivery dates in March, June, Sept. and Dec. and for delivery dates of upto two years from the current date. Yields are basic unit on which prices are determined.

Thus, Annual discount rate =

Treasury bill futures price is decided on the basis of change in the discount rate.

ADVERTISEMENTS:

Price paid at delivery = 100 – Discount Rate (as a per cent of face value) × 90/360, if discount rate is 6%, for example, 360

100 – 6 × 1/4

100 – 1.50

= 98.50

Deliverable grade is also set out in the terms of the contract as for example 8% coupon bill with a maturity period of 6.5 years to 10 years.

ADVERTISEMENTS:

There are some futures on long-term bonds, like Mortgage Bonds, U.S Gulf bonds. Municipal Bonds etc. The bond that is cheapest to deliver is used for delivery by traders.

Bonds sell in the cash market at varying prices, some above and some below the converted price of the futures contracts (futures prices x conversion factor). The conversion factors are equal to the ratio of the actual price of the deliverable bond, to the delivery price of the futures contract; the bond that is cheapest to deliver is used for delivery by traders and that is decided by the bond, for which the difference between the invoice price and market price is the most positive.

Futures price = cash price + carrying costs

Carrying costs depend on the interest at which money can be borrowed by the investor and the period of financing, say 3 months to delivery.

3. Duration Effect on Futures:

Futures on fixed income securities, the duration of the portfolio can be changed. Instead of buying in the cash market, it is cheaper to hedge in futures. If interest rates are likely to increase, the investor should shorten the duration of the portfolio and vice versa. He then uses in technique of buying or selling the futures to lengthen or shorten the duration, respectively. This effect on portfolio is called duration effect of futures.

ADVERTISEMENTS:

Portfolio can have reduced duration by selling short in futures and increased duration by buying futures. If cash is expected and interest rates are likely to fall pushing up the prices of bonds, then investor can go long in futures and when funds come in the futures can be converted into cash purchase of bonds or the underlying securing. The opposite stand can be taken if an outflow of cash is expected at a specific time period in future.

4. Hedging Effect on Futures:

Hedging in futures can be done to reduce the interest rate risk. A futures position can be taken to offset the risk in the cash market. Thus, a ten year bond is likely to suffer capital loss due to rise in yields and that is held in the portfolio of the investor.

The risk can be hedged by an appropriate sale of that security-backed futures. If the loss on the existing security is offset by the gain in the futures contract then it is called a perfect hedge. The difference between futures price and cash price is called the basis and the risk of variance of this basis is called basis risk.

The above basis risk is substantial when the cross hedging is done. Cross hedging is hedging in a bond futures, which is not identical with the bond to be hedged and held in the portfolio. A hedged position thus creates a basis risk which can be reduced or eliminated by taking extreme caution and use of expertise in anticipation of the proper time and bond to be hedged.

5. Yield Enhancement Effect on Futures:

The futures on fixed income security, say a bond, can be used to improve yields also. What hedging has done is to reduce the risk on the portfolio by holding a long- term bond for a short maturity. As the price of the futures is fixed, the risk is nil on this period of the futures say 3 months, and the ten year bond of 10 years, purchased will have greater risk than a riskless bond of 3 months in futures plus a 9 year 9 month bond in the portfolio. The holding of a riskless bond for short periods of time in the futures, reduces the risk. This process may, or may not increase the yields, however.

To enhance the yields, the yield on the synthetic security should be higher than on the cash market security. This synthetic security is created by being short in a three months futures Treasury bill along with a long position in the cash market. If the yield on the three month Treasury bill is higher say 6.6% as against the Treasury bill yield in cash market of 6.4%, then the portfolio will benefit, from higher yield of 0.2% on the synthetic security, in the futures market.

6. Options in Future Contracts:

Another financial derivate product traded in New York and London for example is options on future contracts. These contracts are presently traded in Europe and America, in Treasury bonds, Treasury Notes and Euro-dollar deposits. Calls and puts in the above futures are traded.

A call position if exercised, will lead to a long position in the cash market. A put option if exercised will lead to a short position in the cash market. If not exercised, only cash differences are paid and received by the buyer and seller respectively.

The cost of such deals includes the premium paid and the limited margins that have to be deposited for dealing in Futures. By using options trading, the futures market provides high risk speculation for those whose speculative instinct is high. Futures market has an element of speculation although lack of delivery by itself is not speculative but that futures prices may differ widely from its price in cash market at the time of settlement, is itself risky and speculative.

7. NSE Proposal for Futures:

The NSE has proposed to start Futures and options by end of the year 1996 (O & F Section). This section is for corporate members only. Members trading only and those who will write options are the two classes of members in O & F Section. The former will have a networth of Rs. 3 crores and the latter Rs. 5 crores. They have to pay additional cash deposits with NSE and National Securities Clearing Corporation (NSCCL) separately.

The membership of O & F Section is also thrown open to non-NSE members, if they satisfy all the requirements of networth and cash deposits with NSE and NSCCL. The new O & F members have to be members of the Equity market of NSE also, as they can take positions in the cash and futures markets at different times.

Existing NSE members opting as trading members in the O & F Section will have to hike their networth from Rs. 1 crore to Rs. 3 crores and make an additional cash deposit of Rs. 28 lakhs. For NSCCL they will have to pay cash deposit of Rs. 25 lakhs and provide a bank guarantee of Rs. 25 lakhs.

Existing members of NSE opting to be writers of “Futures” or “Options”, will hike their networth to Rs. 5 crores and pay a cash deposit of Rs. 56 lakhs to NSE. For NSCCL, they would make a cash deposit of Rs. 50 lakhs and provide a bank guarantee of Rs. 50 lakhs. The other terms and details are being worked out by the NSE.

Even now, NSE did not succeed in starting futures due to the difficulties in starting futures and due lack of infrastructure, and to the inability of members to bring in additional funds. Reference was already made to the recommendations of the Committee on Derivatives, set up by SEBI.