Let us make an in-depth study of the Chamberlin’s concept of excess capacity.

Prof. Chamberlin’s explanation of the theory of excess capacity is different from that of ideal output under perfect competition.

Under perfect competition each firm produces at the minimum on its LAC curve and its horizontal demand. Curve is tangent to it at that point. Its output is ideal and there is no excess capacity in the long-run.

Its Assumptions:

ADVERTISEMENTS:

Chamberlin’s concept of excess capacity assumes that:

(i) The number firms be large,

(ii) Each should produce a similar product independently,

(iii) It should charge a lower price and attract other’s customers and by raising its price will lose some of its own customers,

ADVERTISEMENTS:

(iv) Customer’s preferences be fairly evenly distributed among the different varieties of products,

(v) No firm should have an institutional monopoly over the product,

(vi) Firms are free to enter its field of production,

(vii) Long-run cost curves of all the firms are identical and are U-shaped.

ADVERTISEMENTS:

As we are aware that this concept of excess capacity is associated with imperfect competition in the long period. This can be defined as the difference between the optimum level of output and the output actually obtained in the long-run.

Regarding this Prof. M. M. Bober has said:

“Under imperfect competition we are apt to witness too many firms all working under less than their optimum capacity all charging higher than competitive price, and all exercising their art of advertisement against each other in the efforts to retain customers and to take them away from each other.”

The above observation of Prof. Bober reveals three major aspects of excess capacity:

(i) In the imperfect competition the output of the firms is less than the optimum output which indicate that the monopolistic firm can produce more than the determine output and the cost of production can further fall.

(ii) The price is determined under imperfect competition is more than the price determined under perfect competition. It is simply because with the increase in sale the price falls.

(iii) The advertisement outlay of each firm influence the sale of his firm and affect the sale of other firms.

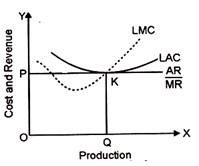

The analysis of Perfect Competition can be explained with the help of the following diagram:

In this figure the demand curve (AR) and marginal revenue (MR) are tangential to the long-run average cost curve (LAC) at minimum point and the condition of full equilibrium are fulfilled i.e.,

ADVERTISEMENTS:

LMC = MR and AR = LAC

This means that in the long period the entry of new firms forces the existing firms to make the best use of their resources to produce at the point of lower average total cost. In this figure at point K the abnormal profits will be competed away and the firms will earn only normal profits because here LAC =AR = MR = LMC. OQ is the most efficient output and there is not excess capacity.

Excess Capacity in Imperfect Competition:

ADVERTISEMENTS:

Under imperfect competition the demand curve facing the individual firm is downwards sloping curve. The downwards sloping demand curve cannot be tangent to the long-run average cost curve at the minimum point. The double condition of equilibrium LMC = MR = AR = minimum LAC will not be fulfilled.

The firm will, therefore, be of less than optimum size even when they are earning normal profits. No firm will have the incentive to produce the optimum output because with the increase in the output the average revenue will fall and possibly the AC >AR. The firm will earn losses instead of profits or normal profits.

A comparison of two equilibrium (i.e., perfect competition and imperfect competition) reveals that the firm under imperfect competition will not be working to their full capacity. There will be chronic excess capacity and wastage. Each firm will be producing less than their full capacity, incurring higher costs and charging a higher price than the perfect competition. Thus, in imperfect competition output will be OQ which is less than OQ1 under perfect competition, the price (OP) under imperfect competition is more than the price OP1 under perfect competition.