The following points highlight the four popular techniques for measuring risk and uncertainty in different projects. The techniques are: 1. Risk Adjusted Discount Rate Method 2. The Certainty Equivalent Method 3. Sensitivity Analysis 4. Probability Method.

Technique # 1. Risk Adjusted Discount Rate Method:

This method calls for adjusting the discount rate to reflect the degree of the risk and uncertainty of the project. The risk adjusted discount rate is based on the assumption that investors expect a higher rate of return on risky projects as compared to less risky projects.

The rate requires determination of:

(i) Risk free rate, and

ADVERTISEMENTS:

(ii) Risk premium rate.

Risk-free rate is the rate at which the future cash inflows should be discounted. It is the borrowing rate of the investor. Risk premium rate is the extra return expected by the investor over the normal rate. The adjusted discount rate is a composite discount rate.

It takes into account both time and risk factors. In this technique, the discount rate is raised by adding a risk margin in it while calculating the NPV of a project. For example, if the rate of discount is 10% for the project, it may be raised to 11% by adding 1% to take account of risks and uncertainties.

The increased discount rate will reduce the discount factor, thereby lowering the NPV. Thus the project would be judged as undesirable. This method is used for ranking of risky projects. But the problem with this method is that there is no ‘specified margin’ which should be added to the free risk rate.

Technique # 2. The Certainty Equivalent Method:

ADVERTISEMENTS:

According to this method, the estimated cash flows are reduced to a conservative level by applying a correction factor termed as certainty equivalent coefficient. The correction factor is the ratio of riskless cash flow to risky cash flow.

The certainty equivalent coefficient which reflects the management’s attitude towards risk is

Certainty Equivalent Coefficient = Riskless Cash Flow/Risky Cash Flow.

If a project is expected to generate a cash of Rs. 40,000, the project is risky. But the management feels that it will get at least a cash flow of Rs. 24,000. It means that the certainty equivalent coefficient is 0.6.

ADVERTISEMENTS:

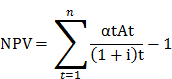

Under the certainty equivalent method, the net present value is calculated as:

Where αt = Certainty Equivalent Coefficient

At = Expected Cash Flow for year t

I = Initial outlay on the project

i = Discount rate

Technique # 3. Sensitivity Analysis:

The future is not certain and involves uncertainties and risks. The cost and benefits projected over the lifetime of the project may turn out to be different. This deviation has an important bearing on the selection of a project.

If the project can stand the test of changes in the future, affecting costs and benefits, the project will be selected. The technique to find out this strength of the project is covered under the sensitivity analysis of the project. This analysis tries to avoid overestimation or underestimation of the costs and benefits of the project.

In sensitive analysis, a range of possible values of uncertain costs and benefits are given to find out whether the projects desirability is sensitive to these different values. In this analysis, we try to find out the critical elements which have a vital bearing on the costs or benefits of the project.

ADVERTISEMENTS:

In investment decision, one has to consider as many elements of uncertainty as possible on costs or benefits side and then arrive at critical elements which affect the expected costs or benefits of the project. How many variables should be tested to carry out the sensitivity analysis in order to find out its impact on costs or benefits of the projects. It is a matter of judgement.

In sensitivity analysis, one has to consider the changes in the various factors correlated with changes in the other. In order to arrive at the degree of uncertainty, the decision maker has to make alternative calculation of costs or benefits of the project.

When there are several uncertain outcomes, three cost-benefit calculations are made in this analysis:

(i) The most pessimistic where all the worst possible outcomes are estimated.

ADVERTISEMENTS:

(ii) The most likely where all the middle of the range outcomes are estimated.

(iii) The most optimistic where all the best possible outcomes are estimated.

It explains how sensitive the cash flows are under these three different situations. If the difference is larger between the optimistic and pessimistic cash flows, the more risky is the project. The most likely outcome can give a good guide to how ‘borderline’ is the project.

Technique # 4. Probability Method:

Another method for dealing with risks and uncertainties is to estimate the probable value for a result. Here one has to see a range of possible cash flows from the most optimistic to the most pessimistic for each pertinent year. Probability means the likelihood of happening of an event. It is the proportion of times an event occurs i.e. its frequency. It is the ratio of favourable number of events to the total number of events.

ADVERTISEMENTS:

In a particular situation, if all possible outcomes of an event are listed and the probability of occurrence is assigned to each outcome, it is called a probability distribution. For any probability distribution there is an expected value. The expected value is the weighted average of the values associated with the various outcomes, using the probabilities of outcome as weights.

If NPV1 NPV2 and NPV3 are three possible estimates of the net prevent value of a project under uncertainty, and’ the probability of each outcome of NPV is P1 P2 and P3 then the expected net present value is

Ev (NPV) = P1 (NPV1) + P2 (NPV2) + P3 (NPV3).

This method is conceptually sound. But it lacks objectivity as it is not possible to find out the probabilities of different outcomes.