The equilibrium conditions of an individual firm under perfect competition are to be studied under two heads. They are: 1. Short-Run Equilibrium 2. Long-Run Equilibrium.

1. Short-Run Equilibrium:

A short period has two major characteristics:

(a) Fixed production scale:

ADVERTISEMENTS:

In the short period a firm cannot change its scale of production. It has to increase its supply by utilising fully the existing machinery and capital equipment. So, it has to increase fixed and variable costs in such a period.

(b) No free entry or free exit of firms:

In the short period no new firms can enter into the industry, nor an old firm can go out of the industry. So, the number of firms in the industry remains the same.

Conditions of a short-run competitive equilibrium:

ADVERTISEMENTS:

In such a short period there are two major conditions of equilibrium of a firm:

(a) P = SMC:

The total profits of a firm become maximum at the output where marginal cost is equal to marginal revenue. Under perfect competition a firm is to sell all the units of its output at the same market price. For this reason market price becomes equal to a firm’s marginal revenue in this type of market.

So, it follows that the total profits of a competitive firm become maximum at the output level at which P=MC. So a competitive firm produces an output up to this level. It may be noted that in equilibrium position the marginal cost must be a rising one; otherwise there cannot be any stable equilibrium of a competitive firm.

ADVERTISEMENTS:

(b) The Short-Run P and SAC—(Break-Even and Shut-Down Points):

In the short run, the competitive price may be greater than SAC, creating excess profits as no new firms can enter the industry. Sometimes it may be equal to AC and then the firm earns just normal profits, and this point (P=SMC=SAC) is called the break-even point as it equals TR with TC. Again, sometimes the competitive price may even be less than average cost yielding loss to the firm, provided it is greater than, or equal to, average variable cost.

If the market price is just equal to the average variable cost, the firm reaches what is called the shutdown point. Unless the position improves; or if the price goes below it, the firm will have to close down at this point. The short-run equilibrium output and price of a competitive firm is illustrated in Fig. 4.

It shows that at price OP1 (the demand curve being d1d1) the competitive firm produces OQ1 units of output because at this output level the price (OP1 or Q1d1) is equal to the marginal cost (Q1d1). Here the price is greater than the average cost (Q1d1), creating an excess profit (Ld1) is possible in the short run as no new firms can enter into the industry. If the price is lower, i.e., OP2 (the demand curve being d2d2), the firm produces OQ2 units of output, because at this output now the price (OP2 or Q2d2) is equal to marginal cost (Q2d2).

Here the price is also equal to the average cost (Q2d2), giving the firm only normal profits. Such a point (P=SRMC=SRAC) is known as the break-even point (the point without either loss or profit, the normal profit being ignored). Again, if the price is still lower at OP3 (the price line being d3d3), the firm would produce OQ3 because at this output the present price (OP3 or Q3d3) is equal to the marginal cost (Q3d3).

But, here the price is less than the average cost (Q3T) creating a loss for the firm. Such a price is possible in the short run as it fully covers the average variable cost (Q3d3). The point (P=AVC) is called the shut-down point; the firm will shut down its business, unless the position improves or if the price falls below this short-run minimum limit of the average variable cost.

2. Long-Run Equilibrium:

A long period has also two characteristics:

ADVERTISEMENTS:

(a) Variable Scale of Production:

In the long run a firm can change it scale of production. So, it has to increase only variable costs in the long run.

(b) Free Entry or Free Exit of Firms:

In the long run new firms may enter the industry or the existing firms can go out of it, depending on profits and losses.

ADVERTISEMENTS:

Conditions of the long-run equilibrium of a competitive firm:

In such a long period there are also two important conditions of equilibrium of a competitive firm.

(a) P = LMC:

Even in the long run a competitive firm would produce an output up to that level at which price is equal to marginal cost which must be rising one. Although the equality of P and MC is an essential condition of the long-run equilibrium, it is not a sufficient one; another important condition is to be fulfilled for a stable long-run equilibrium.

ADVERTISEMENTS:

(b) P = LAC (minimum):

The second condition is that the long-run competitive price must also be equal to average cost. It is obvious due to the fact that in the long run the total revenue of a competitive firm must cover its total cost. If the long-run price is greater than the average cost, the firm will make excess profits, which will attract new firms into the industry.

For this reason, the number of firms will increase, the total supply will be larger and the market price will fall to the level of average cost. So, the firm under consideration will incur a loss; as a result some firms will leave the industry, the number of firms will be smaller, the market supply will fall and the market price will rise again to the level of average cost.

Thus, it is clear that the long-run competitive price must equal both marginal cost and average cost, and the firm is then able to make only normal profits. At this stage the average cost is the minimum (at the point of equality of P and LAC). So, in long-run equilibrium the competitive price becomes equal to the minimum average cost.

Hence, the condition of the long- run equilibrium of a competitive firm becomes:

P=LMC=LAC (minimum).

ADVERTISEMENTS:

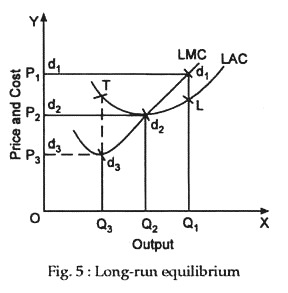

The long-run equilibrium of a competitive firm is shown in Fig. 5. Here at the output level OQ1 the price OP1 is equal to the marginal cost (Q1d1). This price cannot be stable as it is higher than the average cost (Q1L). This price will attract new firms into the industry, causing an increase in market supply and a consequent fall in market price. If, on the other hand, market price is lower at OP3, the firm produces OQ3 units of output where the price is equal to the marginal cost (Q3d3).

This price also cannot be stable as it is lower than the average cost (Q3T). But when the price is OP2, the firm produces OQ2. This price becomes stable as it is equal to both marginal and average costs (Q2d2). Here the average cost is the minimum. So, a competitive firm attains the long-run stable equilibrium position at the point of intersection of the three curves (d2d2, LMC and LAC), i.e., at the output level at which P=LMC=LAC (minimum).