Decision making involves choice between alternative courses of action. The best course of action is the one which yields the greatest cost advantage. In order to make a decision, especially day-to-day routine decisions, it becomes necessary to have knowledge about the behaviour of costs under varying conditions.

In other words, it becomes necessary for the decision maker to know which of the costs remains unchanged if the selected course of action is adopted, and which of the costs vary. It is, in this context, i.e., short-run decision making, that we appreciate marginal costing as a tool of decision making.

As the Official CIMA Terminology points out that “its special value is in recognising cost behaviour, and hence, in assisting in decision making.”

Contents

ADVERTISEMENTS:

1. What is Decision Making

2. Characteristics of Decision Making

3. Factors of Decision Making

4. Situations of Decision Making

ADVERTISEMENTS:

5. Types of Costs in Decision Making

6. Phases, Decision Model and Short-Term Decisions

Decision Making: What is, Characteristics, Factors, Decision Model, Phases, Situations, Types of Costs and Short-Term Decisions

What is Decision Making

Decision making involves choice between alternative courses of action. The best course of action is the one which yields the greatest cost advantage. In order to make a decision, especially day-to-day routine decisions, it becomes necessary to have knowledge about the behaviour of costs under varying conditions.

In other words, it becomes necessary for the decision maker to know which of the costs remains unchanged if the selected course of action is adopted, and which of the costs vary. It is, in this context, i.e., short-run decision making, that we appreciate marginal costing as a tool of decision making.

ADVERTISEMENTS:

As the Official CIMA Terminology points out that “its special value is in recognising cost behaviour, and hence, in assisting in decision making.”

The cost-volume-profit analysis, which is an extension of marginal costing, enables management in studying the effect on profit of changes in the volume and the attendant variable cost. Such a study is of utility in profit planning. Besides, it also facilitates tactical decision making.

Managerial decisions involve alternative choices. For the purpose of making such decisions, management needs data regarding relevant costs. The technique of marginal costing is of immense use in decision making involving alternative choices.

The basic decision making indicators in marginal costing are profit- volume ratio, break-even point, margin of safety, indifference point, shut-down point and differential costs.

While defining the term ‘marginal costing’, the CIMA Official Terminology has specifically mentioned that marginal costing assists in managerial decision making. Besides profit planning, evaluating performance and cost control, the technique of marginal costing is of immense use in short-term decision making in which fixed costs are totally excluded.

Decision Making – Characteristics

Decision making reflect the following characteristics:

Managerial decisions are forward-looking. As such, every such decision is bound to be influenced by a forecast of future results likely to occur under the various alternative courses of action. Costs associated with the future results of alternative courses are, obviously, future costs. They tell us what would happen if a specific decision is arrived at.

Costs may be distinguished as past costs and future costs. Past costs are historical in nature. They are those that are recorded in the account books. As such, they are also called ‘accounting’ costs. These costs are the result of past decisions. They cannot be influenced by a decision to be made either now or in future.

Past costs may also be considered to be the same as sunk costs. They are also unaffected by the choice between alternatives. Although these are not relevant for decision making, they do provide the basis for making a proper estimate of future costs. Thus, all decision making costs are future costs but not all future costs are relevant costs.

Decision Making – Factors: Contribution, Specific Fixed Cost, CVP Relationship, Incremental Contribution, Capacity and More…

The important factors to be considered in decisions are:

ADVERTISEMENTS:

(a) Contribution

Whether the product under consideration, makes a contribution towards recovery of fixed cost;

(b) Specific fixed cost, if any

ADVERTISEMENTS:

Where a choice is to be made between alternative courses of action, the additional fixed overhead, if any, should be taken into consideration;

(c) CVP relationship

It is necessary to study the effect of increase in volume on profit, and the rate of earning additional profits;

(d) Incremental contribution

ADVERTISEMENTS:

Where additional quantities can be sold only at reduced prices, incremental contribution will be more effective in decision making, as it takes into account the additional quantity sold and additional contribution per unit;

(e) Capacity

Whether acceptance of the incremental order, or additional product line is within the firm’s capacity or whether any key factor comes into play; and

(f) Non-cost factors

Wherever applicable, the non-cost factors should also be considered.

It is necessary to remember, in the context of managerial decision making that the technique of marginal costing is relevant for managerial decisions, especially short-run or tactical decisions, where production capacity remains unchanged and, hence, fixed costs are not relevant for such decisions but only the contribution margin.

Decision Making Situations – Decision to Make or Buy, Decision to Accept a Special Offer, Adding or Dropping a Product-Line or Department, Product Pricing, Level of Activity Planning and More…

ADVERTISEMENTS:

The following are the various decision making situations involving alternative choice:

(a) Decision to Make or Buy:

Quite often, management has to take a decision with regard to the manufacture of a component used in the firm’s assembled product or buy the same from outside. Such decisions become necessary when unutilised production facilities exist, and the same could be better utilised to produce a product or a component hitherto being purchased from outside.

It is also possible that concerns manufacturing more products than one, but each being complementary to the other, may decide to give up the production of one of them on the ground that it is less profitable and buy the same from outside. Such a situation may exist in the case of concerns manufacturing primary packing materials.

The considerations governing such a decision are:

(i) Availability of production facility in terms of men, machine and space;

(ii) Differential costs of making the part; the purchase price of the component should be compared with the estimated increased cost of manufacture; and

ADVERTISEMENTS:

(iii) The opportunity cost of using the existing capacity to manufacture another component or product and its contribution to the recovery of fixed cost.

Sometimes, the decision may go against making even if the marginal cost were less than the purchase price. Such a situation is possible when there is no idle capacity and the manufacture of the component is at the expense of some other work involving a high opportunity cost of the facilities released for making.

In other words, while manufacturing the product or component, the contribution foregone should be added to the marginal cost of the product before comparing the same with the vendor’s price.

Again, if the concern in question is not only manufacturing but is also undertaking assembly work, the decision to buy depends upon uninterrupted supply of the component so as not to hold up the assembly work. Further, if it is desired to keep the technical know-how a secret, the decision will be to make rather than to buy.

The other non-cost consideration is whether the supplier can assure and maintain the quality of the component. It is also necessary to consider whether it is’ possible to retrench workers consequent upon dropping the production of the component and whether it is possible to re-start production of the same component as circumstances warrant the same.

(b) Decision to Accept a Special Offer:

Sometimes, a concern may receive a special order either from a local buyer or a buyer from outside the country for a large quantity of its product at a special price, which is lower than the selling price, or the full cost. Such a bulk order may be attractive provided the concern is operating at less than its normal capacity.

ADVERTISEMENTS:

The main consideration in a situation such as this is that the price quoted by the buyer should cover the whole of variable cost plus any additional cost incidental to the special order. Fixed cost is of no consideration because of the fact that it does not in any way influence the decision when there is unused production capacity.

In case the concern is already operating at its full capacity, acceptance of the order means adding to its capacity, and the consequent increase in fixed costs. In such a case, management may prefer to give up the production of any other product and divert the resources employed therein to the production of the article for the special order.

If that is so, it is necessary to take into consideration the opportunity cost of the business lost on account of giving up production of an article.

The other considerations governing the decision are:

(i) In case the special order is from a local buyer, whether the reduced price is to be offered to all other local customers;

(ii) Whether the special order is only temporary;

ADVERTISEMENTS:

(iii) Whether there is the possibility of the buyer from a foreign country reselling the same product in the local market at slightly higher price than the purchase price.

(c) Adding or Dropping a Product-Line or Department:

A multi-product concern may, as situation warrants, add a product-line or eliminate an existing one. Similarly, a concern with a number of production departments may, if it becomes necessary, close down one of its departments. In the case of any of these situations, it is the marginal costing technique that assists managerial decision making.

Products, product-line or departments which do not contribute towards variable costs should be dropped or closed down, if there is no possibility of any improvement. In case, however, contribution generated by the product or department is sufficient to cover the whole of variable costs as well as a part of fixed costs, the decision should be to continue the product-line or department.

Part of fixed costs covered should be well above the shut-down costs, which must be incurred even if the plant is closed down.

Sometimes, the operating income statement pertaining to the product-line may not provide the required data for decision making with regard to suspension or closing down of a segment of the organisation. In such a case, it may become necessary to make incremental revenue analysis for making the decision.

In case some items of fixed cost are common to all the products or segments of the organisation, they would still continue to be incurred even if a product, department or segment is closed down. These costs are, therefore, irrelevant to decision making. Incremental revenue is to be compared with incremental costs for making the decision.

When a concern is desirous of introducing a new product, the most important consideration to be given attention to is whether the product is capable of contributing sufficient amount for the recovery of the whole variable cost and any excess over variable cost contributes to the overall profitability of the concern.

Even if the product does not contribute to the recovery of fixed cost, the decision should be to introduce the product, since the existing products are bearing the fixed cost. Fixed costs are, therefore, not relevant for deciding whether the new product is to be introduced or not.

Before a decision is taken with regard to dropping of a product or a product- line, factors other than contribution should also be considered.

These factors, which are non-cost in nature, are:

(i) The position of the competitor in the market;

(ii) His reaction to closure of the department or dropping a product;

(iii) Accommodating the retrenched workers in the backdrop of strong trade unions;

(iv) The consequence of closing down on the reputation of the concern;

(v) The consequence of closing down on the relationship between the concern and its suppliers;

(vi) Long-term prospects of the product to be dropped;

(vii) The attitude of customers;

(viii) Changes in the manufacturing method and equipment; and

(ix) Whether the concern is working below normal capacity or at full capacity.

(d) Product Pricing:

One of the objectives of cost accounting is the ascertainment of cost for fixation of selling price. Cost data or cost information is, therefore, an important input to pricing decisions. In most cases, selling prices are derived from cost information by estimating future product costs and adding the required margin of profit. While estimating future costs, both variable and fixed costs are taken into consideration. As such, the price that is thus fixed is known as ‘full cost’ price or ‘cost-plus’ price.

In some cases, however, the prevailing market price is accepted. The firm will then be the price-taker. Even then, it has to depend upon cost data for determining the scale of operation, method and terms of marketing, relative profitability of different products, etc.

Decision with regard to pricing the product depends upon the cost of the product and the profit it has to make by production and sale of the product.

Although market price is the result of market forces of demand and supply, absence of perfect competition, and the presence of oligopolistic conditions, has empowered every firm to fix its own price. It is, in this context, that the firm has to make pricing decisions.

Price fixation is one of the fundamental managerial problems. This is because of the fact that there are quite a number of prices which a firm could fix in modern times. These are full-cost pricing, differential pricing, product-line pricing, skimming pricing, penetration pricing, etc.

In every one of these cases, it is the ‘cost’ of the product that sets the lower limit to its price and the upper limit depends upon the nature of the product, the nature of demand for the product, the degree of elasticity of demand, the extent of the market, etc.

During normal periods of sale, therefore, the price charged should cover the total cost. Price of the product should be based on full or total cost arrived at by the application of absorption costing method.

Pricing During Depression:

During a period of business recession, however, the principle of full cost pricing cannot be followed. This is because of the fact that purchasing power in the hands of consumers being low; the demand for products in general, will also be low.

In such circumstances, it becomes necessary for the firm to sell the product at a lower price which may or may not cover the full cost. Alternatively, the firm has to suspend production of the article. In this case, it has to incur the fixed cost which will be the loss to be faced by the firm.

Normally, no concern would like to follow the alternative of suspending production if it could fix the price in such a way as to cover the entire amount of variable cost plus some contribution. During a period of depression, therefore, every firm would fix its price at such a level that it maximises its total contribution.

Variable cost per unit will thus be the lowest level of price and the upper limit being dependent upon the nature of the product and the market conditions. In this case, the larger the contribution, the lower would be the loss since a part of the fixed cost is also covered by the contribution.

Price Indifference Point:

The level of sales at which the firm’s profit is the same for two pricing alternatives, is known as the price indifference point. If, at a particular level of sales, the price fixed generates the same amount of profit as the firm was earning before, the firm is indifferent with regard to fixation of price.

In case, however, the expected sales volume is higher than the price indifferent point, the proposed price change is to be implemented. If the expected sales volume is lower than the price indifferent point, the proposed change to the price should not be decided upon.

Fixation of Price below Marginal Cost:

Although variable cost sets the lowest limit to price fixation, it may, sometimes, become necessary to fix the price even below variable cost.

These circumstances are:

(a) When the product in question is perishable in nature;

(b) When it is desired to make use of the existing stock of materials likely to deteriorate;

(c) When the concern has already purchased a huge quantity of raw materials; and the price of the same is declining;

(d) When it is desired to introduce a new product in market;

(e) When a foreign market is to be captured;

(f) When there is keen competition in the market and lowering the price is a business strategy adopted to drive out competitors;

(g) When it is felt that lowering the price is much better to keep the business going rather than close it temporarily, and meet the shut-down costs;

(h) When employees, specially skilled workers, cannot be retrenched;

(i) To retain old customers who may be lost to competitors if activities are suspended;

(j) To push up the sale of another highly profitable product;

(k) To assist the sale of a joint product;

(I)To keep plant and machinery quite fit for production which could not otherwise be possible if business is stopped;

(m) To capture the future market;

(n) In the case of public utility services;

(o) If reopening after temporary closure requires heavy expenses; and

(p) If dumping in a foreign market is to be resorted to.

(e) Level of Activity Planning:

In the context of profit maximisation, management of a concern operating at less than the installed capacity has to face the problem of planning the level of activity. It is a known fact that the impact of fixed cost per unit will be higher at lower levels of production.

A concern producing goods on a small scale cannot take advantage of the economies of scale unless it expands itself and produces on a large scale. It is also true that a concern has to increase its output and sell a larger quantity by lowering the price.

When a concern is not working to its full capacity, decision with regard to the level it should operate becomes relevant for the following reasons:

(i) Increased capacity utilisation resulting in increased output results in lower fixed cost per unit, since the same amount of total fixed cost gets spread over a larger number of units;

(ii) It is possible to take advantage of economies of scale by increasing the capacity utilisation;

(iii) Bulk purchases of materials results in lower purchase cost due to quantity discount allowed by the supplier;

(iv) If the level of activity is much more than what it should be, fixed cost may increase in step-like fashion;

(v) To cope with the increased level of activity, the concern may have to hire skilled labour by paying a higher wage; and

(vi) With the increase in the volume beyond a particular level, overtime wages have to be paid to workers if additional labour force cannot be employed owing to increased demand for labour.

(f) Profit Planning:

Marginal costing is the technique used for profit planning. In order to maximize profits in the long run, management plans the profit figure and determines the level activity needed to achieve the planned profit.

(g) Profitability of Further Processing:

A very common type of managerial decision whether to sell a product at an intermediate stage of production itself or to process the same further in order to enhance its commercial importance that management has to take is in the case of concerns engaged in the manufacture of joint products.

For instance, in the case of an oil mill, refined oil and oil cake are the joint products. Both are the result of joint processing. Costs incurred at the stage of emergence of the two products are joint costs. These costs are irrelevant for making the decision whether to sell oil cake as it is, or add the necessary ingredients to it and refine the same into cattle fodder.

In order to make a decision, it is necessary to take into consideration only the costs to be incurred for converting oil cake into cattle fodder. This decision depends on incremental revenue. In case the cost of conversion which is the incremental cost, is lower than the incremental revenue, which is the revenue got by the sale of fodder, the decision should be to process further.

(h) Optimum Use of a Limiting or Key Factor:

When an input resource is in short supply, the term ‘key factor’ is used for such an input. Shortage of raw materials, non-availability of the required grade of labour, limited machine capacity, shortage of working capital, shortage of power, etc., are some of the key factors which management has to take into consideration while preparing its budget.

One or more of these key factors may impose restriction on what a concern may produce and sell. In other words, owing to the existence of any of these factors, a firm may not be in a position to reach its full potential, i.e., may not produce what it can otherwise produce or sell what it has produced.

In case availability of raw materials, supply of particular grade of labour, machine capacity or working capital limit production to less than the volume that could be achieved, management will be faced with the problem of decision making with regard to the product or the quantity of a product to be produced.

The decision-making indicator in this regard is maximisation of contribution per unit of the key factor. Accordingly, in the case of a multi-product concern, preference is given to that product which yields the highest contribution per unit of the key factor.

When two or more limiting factors are simultaneously in operation, it is necessary to consider all of them to determine the profitability or otherwise of a line of activity. Optimum use of the limiting factor can be made only by taking into consideration the contribution per unit of the limiting factor.

(i) Suitable Product Mix:

In the case of a multi-product concern the question often arises with regard to the product mix or sales mix which will yield maximum profit. The question cannot be answered easily in the light of the fact that each product line is as profitable as the other on the basis of differing cost structures and sales prices.

Under normal circumstances, a product which yields the highest contribution is to be considered to be the most profitable one. Bearing this in mind, management may alter the existing product mix by pushing up production or sales of the more profitable products and reducing the production or sale of the less profitable ones.

However, it is necessary to recognise the key factor or factors, while selecting that product mix which gives the maximum contribution. If there is a key factor, the contribution per unit of that factor has to be compared in order to know the profitability of the products.

Decision Making – Types of Costs: Decision Making Costs, Relevant Costs and Incremental Costs

Some of the types of cost in decision making are as follows:

1. Decision Making Costs:

Cost data or cost information required for product costing cannot be made use of for decision making. Further, the users of cost data are not just the managerial personnel.

Several others such as accountants, economists, engineers, market research analysts, operation researchers, municipal authorities, government, sociologists, psychologists, etc. also fall back upon cost data for their own decision making consistent with their decision objectives.

If this is so, managerial personnel need cost data tailored to meet their requirements. Again, even amongst managerial personnel, the data required by top management will not be the same as those needed by middle and lower levels.

Thus, decision making costs are those that are tailored to meet the requirements of managerial personnel in their function of decision making. Although cost data contained in the cost records constitute the basic raw material for managerial decision making, the collection and presentation of data differ in form and in details, depending upon the purpose for which the same is sought for.

This is mainly because of the fact that the same data, in the same form, will not serve all managerial purposes with the same degree of efficiency. It, therefore, becomes necessary to do the work of addition, subtraction, substitution, etc. to the accounting costs produced from the cost accounting records.

When done so, the resultant costs become called ‘decision-making costs’ collected under various captions or headings such as incremental cost, differential costs, opportunity costs, imputed costs, escapable costs, sunk costs, out-of-pocket costs, etc.

2. Relevant Costs:

All decision making costs should be related or relevant to the decision to be taken. Relevant costs are those future costs that will be different for the available alternatives. Since every managerial decision is different in it and has its own peculiarity, all decision making costs may not be relevant to the decision.

Relevant Costs for Decision Making:

The Official CIMA Terminology defines relevant costs as “costs appropriate to a specific management decision.” Relevant costs are those that differ from one set of circumstances to another, depending upon the nature of decision to be made. Different types of managerial decisions demand consideration of different relevant or appropriate costs. Such costs would change by the adoption of a particular course of action in the form of a decision.

Accordingly, for the purpose of decision making, costs and revenues are classified according to whether they are relevant to a particular decision. While relevant costs are taken into consideration in the process of making a particular decision, irrelevant costs are not. Irrelevant costs are not affected by the decision. Such costs are independent of a decision. Hence, they need not be considered while making a decision.

It may be of interest to note, in this context, that while establishing such costs as are relevant to a particular decision, we may find that some costs will be relevant in one situation, but irrelevant in another. Consequently, the identification of relevant costs depends upon the circumstances of each situation. It is not possible, therefore, to list out costs that would be relevant in particular situations.

If, for instance, a choice is to be made between two alternative modes of transport for making a journey to a particular place, insurance and road tax are irrelevant costs, since they will remain the same regardless of the alternative chosen. Petrol or diesel costs will, however, differ with the mode of transport decided upon. These costs are, therefore, relevant for making the decision.

3. Incremental Costs:

Incremental costs are added costs of change in the level or nature of activity. If a change in the level of activity takes place within a planned range of activity, incremental cost will be the same as variable cost. In case different ranges of activity are compared, incremental cost includes not merely variable cost but fixed cost also. As such, incremental cost need not necessarily be variable cost.

It is, probably for this reason that the Official CIMA Terminology does not distinguish between incremental and differential costs. In fact, it considers incremental cost as synonymous with differential cost and defines the same as “the difference in total cost between alternatives; calculated to assist decision making.”

Cost difference between alternatives may be an increase in cost or a decrease in it. If the cost difference is an increase, it may be called ‘incremental’ cost. Similarly, if the cost difference is a decrease, the same may be called ‘decremental’ cost. Accordingly, incremental cost and decremental cost are nothing other than differential costs.

Decision Making – Phases, Decision Model and Short-Term Decisions

Decision making becomes complex, when numerous alternatives are to be evaluated. Another problem is that many decisions are non-recurring in nature and cannot be resolved by relying on past experience with similar situations.

Decision making involves following phases:

1. Selection of measurement criterion such as a minimum cost, maximum profit or maximum rate of return. The criterion permits a quantitative comparison of alternatives, in terms of goodness or desirability.

2. Preparation of forecasts of uncontrollable factors and identification of the restrictions or constraints that affect controllable factors.

3. Formulation of alternative courses of action and evaluation of each alternative using the measurement criterion referred to at 1 above.

To facilitate this, a decision model can be prepared to guide the formulation and evaluation of alternatives. A formal decision model is a symbolic or numerical representation of the variables and parameters that affect a particular decision. Variables are factors controlled by management and parameters are operating constraints or limitations.

Steps in Building a Decision Model:

1. Define the parameters of the project.

2. Identify possible alternative courses of action and select a measurement criterion.

3. Develop information for each alternative.

4. Construct incremental analysis of alternatives.

5. Eliminate all irrelevant costs.

6. Prepare a formal report to management.

Some Major Short-Term Decisions:

1. Sell or Process Further:

Additional processing adds value to a product and increases its selling price above the amount, for which it can be sold at split off. The decision to process further depends upon whether the increase in total revenues exceeds the additional costs incurred for processing beyond split off point. Joint costs incurred prior to the split off point have no effect on the decision.

The costs incurred before split off are past cost, sunk cost or irrelevant cost for this decision. Only future incremental revenue and differential cost should be considered. Differential cost of additional processing should include all production costs that will be incurred.

Summary of Important Points for Decision-Making:

i. Only relevant costs are used in evaluating alternative price indifference points.

ii. Cost indifference point should be used when preference shifts from one alternative to another alternative at a particular level.

iii. Sunk costs are not relevant for decision making.

iv. The fixed cost of the firm must be examined to see whether it will change due to decision under consideration. If decision variables cause a change in fixed cost, then fixed cost is relevant to the analysis.

v. Depreciation on an asset purchased in the past is irrelevant to decision making.

vi. If fixed assets can be sold, then cash inflow due to disposal is relevant for decision making.

vii. Allocated joint costs are not relevant to a single product decision. Joint costs become relevant only when one alternative is to terminate.

viii. Costs after the split-off point are relevant to decision making.

ix. Opportunity cost represents the benefit forgone by rejecting one alternative to accept another alternative. This must be considered in decision making.

x. If an alternative involves investment, then interest on investment is a major consideration.

xi. When choice is involved between two alternatives, emphasis should be to find out the net advantage of taking a particular decision.

Steps taken are:

(a) Identify revenue for each alternative.

(b) Identify the cost for each alternative taking a particular care to include opportunity cost.

(c) Identify profit for each alternative and the profit (loss) of preferring one alternative to another.

Alternatively, match incremental revenue with differential cost of alternatives involved. Either approach can be followed.

xii. Remember that a decision should not be taken on revenue and cost analysis alone. Qualitative considerations like customer relationship and inter-product relationship may be the major consideration in implementing a decision.

xiii. Cost accumulated for stock valuation purposes should not be used for decision-making purposes.

Quantitative and Qualitative Factors:

It is difficult to quantify in monetary terms all the important elements of a decision. At times, decision is dictated not by quantitative factors but by qualitative factors, which are not amenable to precise quantification.

For example, the decision to purchase from an outside supplier can result in the closing down of a company’s facilities for manufacturing of components. The effect of such a decision might lead to redundancies and a decline in employee morale, which could affect future output.

In addition, companies may become dependent on outside suppliers, who may not always deliver in time. In that situation, the company’s reputation to meet its delivery schedule will suffer and this may lead to loss of customer goodwill and decline in future sales.

All qualitative factors must be properly reported and weighed in decision making. Given below is a summary of non- quantitative considerations relating to certain major decisions.

Non-Qualitative Factors:

i. Make/Buy Decision:

(a) Quality reliability.

(b) Adherence to delivery schedule.

(c) Continuous source of supply.

(a) Availability of space if the company has to revert to a decision to manufacture in future.

ii. Special Order:

Risk of lost orders, if customers or wholesalers learn of special selling prices.

iii. Overtime vs. Additional Shift:

(a) Quality of work on the second shift.

(b) Training problems of new workers if all are assigned to the second shift.

(c) Balancing trained workers and new workers in different shifts.

iv. Continue Operations vs. Temporary Shutdown:

(a) Loss of trained personnel.

(b) ‘World-of-mouth’ advertising from off-season customers.

(c) Other alternatives to increase off-season business.

(d) Regular customers may be lost.

(e) Resumption of operation may call for heavy expenditure.

v. Expand or Contract:

(a) Quality should not go down.

(b) Workers with required level of experience may not be available.

(c) Expansion may require fresh licensing.

(d) Financial calculation may give a rosy picture, but position of obsolescence may not justify the decision. For example all factories in the scooter industry are facing severe problems due to sudden influx of new improved models.

In this situation, relying on financial analysis above for expansion may not be justified. A detailed note on risk involved should always accompany proposals for expansion.

If a product is processed beyond split off, fixed overheads that are common to other production activity must be excluded from the decision analysis.

This decision can be taken in following two situations:

A. The company already processes a product beyond split-off and has invested in the equipment and required personnel.

B. The company is evaluating the possibility of further processing beyond split off and must incur certain equipment costs and other fixed costs, if additional processing is to incur.

Important Considerations in Situation A:

i. Certain fixed costs such as supervisory salaries are related to additional processing.

If these production salaries would be eliminated by selling products at split off, these costs are relevant and should be considered in decision making. If salaried personnel would be assigned other duties in the company, when additional processing is discontinued, then salary costs are not relevant as they are incurred in either decision alternative.

ii. If equipment used for additional processing will remain idle or be used in other processes, then it should be ignored in the decision analysis.

iii. Depreciation is never relevant in a short run operating decision, since depreciation is an allocation of costs incurred in the past time period.

iv. If the equipment is sold for cash and not used for additional processing, the annual cash equivalent cost should be included as an annual incremental cost. The annual cash equivalent cost is the annual cash flow of an annuity at a specific interest rate for which present value equals the salvage value received from selling old equipment.

Length of the assumed annuity should correspond with the remaining useful life of the equipment. This annual cost factor is not depreciation, but it is the opportunity cost of continuing to use the equipment.

Important Considerations in Situation B:

It is a capital budgeting problem. If a company must expand its physical capacity to allow additional processing it is not sufficient to determine whether incremental revenue exceeds differential costs.

Since new investment in machinery is involved, the rate of return on this investment must be considered. Condition B is a problem requiring a rate of return analysis on new investment. Condition A is a problem or how to best use existing facilities.

2. Discontinuing Sales to a Certain Type of Customer:

A company may face a situation in which it has to make a decision, whether to sell its goods to small customers or large customers. In this situation emphasis should be to find out the net advantage of selling to a particular class of customers. It calls for matching of differential revenues and differential costs. Determine whether placing orders with large customers furnishes business, which provides a higher contribution margin per week of sales personnel efforts.

Therefore, companies may take a decision to apply greater sales efforts to large customers and discontinue salespersons’ visits to smaller customers. Assuming that there is an adequate supply of new large customers, which could be approached for business, for which following data is collected.

It is also assumed in this situation that a sales person can make one successful call to a large customer per week or three successful calls to small customers per week (average of Rs.2,000 sales revenue per small customer).

This is clear from the data collected that selling to large customers maximises the contribution margin per unit of time. The company’s contribution increases by Rs.3,250 (the difference in the contribution margins) per sales-person per week if sales are made to large customers.

The cost and revenue data given above can also be presented as follows:

Readers should note that, when choice is involved in two alternatives, emphasis should be to find out the relative net advantage of taking a particular decision by matching differential revenue and differential cost.

3. Retain or Replace Decision:

Management often faces this decision. Choice is to be made between retention of equipment and its replacement. Basically, replacement of machine or equipment is a capital investment or long term decision requiring use of discounted cash flow technique. Here, discussion is confined to short-range problems.

Therefore, only one aspect of replacement will be dealt with, i.e., how to deal with written-down value of old equipment. Different cost approaches are primarily followed because replacement will invariably involve additional fixed cost.

Major considerations relevant to this decision are given below:

i. Determine relevant items of cash outflows and inflows due to the decision.

ii. Book value or written-down value is irrelevant for this decision. Loss on sale of old machinery is irrelevant for this decision.

iii. Sale proceeds of old equipment is relevant for the decision and should be considered for this analysis.

iv. Replacement of machinery may bring down the cost per unit, but it may involve capital outlay. Here, the company may have to decide at what point replacement will be justified.

v. Profit or loss on the sale of assets being replaced may affect taxation payment and this taxation effect should be included in analysis.

4. Make or Buy Decision:

A company has to take this decision, when it has to face following choice:

i. Buy certain part or sub-assemblies from outside suppliers or

ii. Use available capacity to produce the item within the factory.

This problem involves determining how best to use the available capacity. Least costly alternative is selected from available alternatives.

Following are major considerations:

i. Costs that will be incurred under both alternatives are not relevant to the analysis.

ii. Potential uses of available capacity should be considered.

iii. Pertinent quantitative factors must be evaluated in the decision process.

These considerations include price stability from suppliers, reliability of delivery and quality specifications of materials or components involved. Qualitative factors are not included in incremental cost analysis, but they are kept into account to test the reasonableness of any decision based purely on quantitative cost studies.

If additional equipment must be purchased to permit production, make or buy decision is no longer a short run operating decision and it becomes a problem of capital expenditure which necessitates consideration of required rate of return.

5. Pricing Decisions for Special Orders:

When a company has got excess or idle production capacity, management considers the possibility of selling additional products at less than normal selling price. It is important to note here that units sold at lower prices are marginal output (i.e., they are produced in addition to regular output volume). The basic problem is to determine an acceptable price for marginal output.

This type of situation arises, when a company receives a special order from a foreign customer or from a firm that intends to resell the product under a private label or brand name. Cost analysis using contribution, approach is a useful technique to find out short run profit effects of special order transactions.

Pricing analysis concentrates on the recovery of incremental costs caused by accenting the order. Total selling price of the special order must recover variable costs incurred in order to provide a positive contribution margin.

Unless fixed costs are incurred to facilitate the transaction, any contribution margin provided by the special order will increase profit. If the company starts including normal fixed overhead costs, bids may be too high and the company may lose the entire order.

For pricing of special order, fixed cost will be relevant only when it is incurred to facilitate the order. An unusual aspect of special order situations is that special order is not anticipated or included in the period budget or overhead rate determination.

If planned capacity is attained, all fixed overhead costs will be absorbed by regular operations. Therefore, fixed overheads which are incurred regardless of special order decisions are not relevant to pricing analysis.

If regular customers come to know that price cuts are being allowed, the company’s total sales may be adversely affected. As a general rule, total price for special order should be an incremental cost plus desired profit.

6. Elimination of Unprofitable Segment:

Sometimes management has to decide whether to shut down or continue a segment of the organisation. A segment can be a product, department or sales territory etc., based on decision-needs of management. The decision involves choice from the two alternatives, i.e., either to keep the segment or to eliminate it.

Key concept is to isolate avoidable costs. This decision is of special importance in performance evaluation. To evaluate the financial consequences of eliminating a segment, it is necessary to concentrate on the differential effect of the decision. As a general rule, it is unprofitable to eliminate any segment for which contribution margin exceeds the avoidable fixed costs.

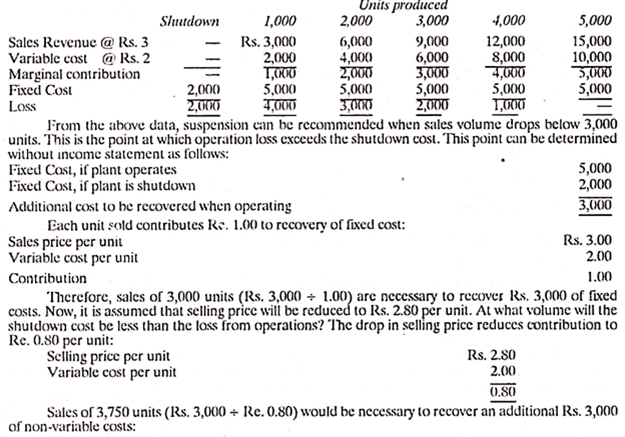

7. Decision to Shut Down Facilities:

Sometimes management is confronted with the possibility of shutdown of both manufacturing and marketing facilities, it is always in the interest of the company to continue to operate the facilities as long as products or services sold recover variable cost and make some contribution toward recovery of fixed cost.

A shutdown of facilities does not eliminate all costs. Depreciation, interest, property tax and insurance continue during complete inactivity.

If operations are continued, certain expenditure connected with shutting down will also be saved. Further, costs will have to be incurred when a closed facility is reopened can be saved.

In the event of a shutdown company may lose the benefit of experience of present employees. In the event of shut-down of facilities, morale of employees and confidence of customers is adversely affected.

Recruitment and training of new workers would add to cost. Loss of customers is another major consideration. It is in the interest of the company to continue the operations as long as differential costs or any amount above that can be obtained. This can be explained by income statements prepared for sales at different capacities.

8. Price to Pay for Raw Materials:

The question is frequently raised as to what constitutes the maximum price one can afford to pay for raw material. This is particularly the case where established selling price is the rule.

Here the manufacturer may work back from the selling price and deduct from it the desired profit, the operating expenses, the manufacturing overhead and the direct labour. This would leave a residual value representing the amount available for raw material. An alternative method is to have recourse to differential costing.

9. Expand or Contract:

Management sometimes faces a situation where it has to decide whether its operations should be expanded or contracted.

Major considerations relevant to the decision are:

i. Expansion means addition in capacity level that calls for incurring of huge capital outlay. Therefore, one dimension of the problem requires it to be considered from a capital budgeting point of view.

ii. Expansion means eventual improvement in production and sales. For improvement in sales, drop in selling price may be necessary. This requires inclusion of another dimension to the analysis for this problem.

iii. Next major consideration is to determine whether it will be possible to sell the increased production. Expansion should not lead to increased inventories.

iv. Contraction may result in reduction of some fixed cost, but the decision will have to consider lost contribution.

10. Change vs. Status Quo:

A company may have an old machine and it may be possible for management to replace it with a machine with updated technology. Thus it is not a simple problem of assets replacement only. It is a choice between change and status quo.

A company may be busy carrying out operations manually but now it may require to work on an automatic equipment with larger capacity, lower unit cost and better quality. The question of deciding between “change and status quo”, often benefits in terms of lower unit cost and costs in terms of huge capital outlay.

Following are the major considerations relevant to this decision:

i. Saving in terms of lower unit cost should be matched with capital outlay. Decisions for the change will be taken at a point where benefits of replacement in terms of lower unit cost equal to capital outlay required for replacement (cost indifference point). But, this is only one cost consideration.

ii. There may be non-cost considerations in the “Change vs. status quo” decision. For example local laws may prohibit retrenchment, which may be necessary to avail lower unit cost due to change. In this situation financial analysis may permit a decision of replacement, but it cannot be implemented, till some alternative productive job is found for workers being retrenched due to change.

iii. Consideration of risk involved due to change should accompany the proposal. Quantitative approaches should be adopted for quantification of impact of risk on a particular decision.

11. Adding a New Product to the Line:

A company is often confronted with the problem of adding a new product to the existing product line. This new product is to be manufactured in the existing plant without any capital investment (for capital investment, capital budgeting approach based on time value of money becomes relevant). In a case of this type, a new product can be priced even a little above the marginal cost.

Following situations may cause this assumption to be questionable:

(i) Suppose a plant is operating at 80% of the practical capacity, when the question of adding a new product say product B was raised. If the sale of existing products is only temporarily depressed, subsequent recovery in sale of products may make it necessary to use the full capacity of the plant for product A. This may require expansion of the plant if product B is continued m production. Additional fixed costs attributable to product B will then be incurred,

(ii) Additional usage of plant facilities may shorten their life and make replacement necessary at an early date. The effect of this is to increase the amount of depreciation, which should be charged during the year. In this case, this additional depreciation and increased maintenance and repair costs are the cost of Product B. This is the rare situation, where even depreciation may become a relevant cost.

The conditions listed above usually require some time to become evident. Hence, product B can probably be produced as a temporary measure. Differential cost analysis may be reasonably accurate from a short-range point of view, but from the long-range point of view it would be realistic to charge product B with an average share of fixed cost associated with all the facilities used in producing and selling the new addition to the product line.

Decision Making and Limiting Factors:

Sometimes a company combats following situations:

i. Full capacity is being utilised.

ii. Output is restricted by such limiting factors as shortage of labour, shortage of materials or factory space etc.

iii. Demand is in excess of the company’s productive capacity.

In a situation of this type, the company faces the problem of deciding the best product mix. Stress remains on contribution per unit of limiting factor and best utilization of available resources. In a situation, where more than one resource is scarce, it is necessary to resort to linear programming method to determine the optimal production programme.

Decision Making: Features, Elements, Importance, Scientific Process and Principles

Let us make an in-depth study of Decision-Making:-

1. Definition of Decision-Making 2. Features of Decision-Making 3. Elements 4. Importance 5. Scientific Process 6. Principles.

Definition of Decision Making:

The important definitions of management are as follows:

1. In Simple word:

“Decision-making is the selection of one course of action from two or more alternative courses of action. It is a choice-making activity and the choice determines our action or inaction.”

2. According to George R. Terry:

“Decision-making is the selection based on some criteria from two or more possible alternatives.”

3. Philip Kotler has defined decision-making as under:

“A decision-making is a conscious choice among alternative courses of action.”

It is clear from the above definitions that if there is only one course of action, the question of decision-making does not arise. But when more than one alternative courses are open before us then the selection of the best alternative is called decision-making.”

Characteristics or Features of Decision Making:

The important characteristics of decision-making are as follows:

1. Decision-making is a selective process in which only the best possible alternative is chosen.

2. Decision-making involves careful evaluation and analysis of all the possible alternatives.

3. Decision-making is the responsibility of the management executives at all levels.

4. It is a continuous process which goes on throughout the life of an organisation.

5. It is a mental process which involves deep thinking and foreseeing things.

6. It may be positive to do a certain thing or negative not to do a certain thing.

7. Decisions are normally taken on the basis of past experiences and present circumstances for a future course of action.

8. It is not an end in itself but a means to reach the goal.

9. If necessary experts and specialists should be consulted before making a particular decision.

10. Decisions exert great influence on the success or failure of an organisation. Therefore, they should not be made in a hurry or without close security and thinking.

Main Elements of Decision Making:

The main elements of decision-making are as follows:

1. Concept of Best Decision:

Rational decisions must conform the basic concept of good decision.

Curdiff and Still:

Mentions three keys to rational decision-making:

(i) Conceptualization,

(ii) Information,

(iii) Prediction.

are the three main keys to rational decision-making. The problem should be thoroughly analysed and all possible alternatives be folly considered.

Rational decisions require:

(a) Intelligence,

(b) Insight, and

(c) Lot of experience.

2. Organisational Environment of the Company:

Organisation environment also exert great influence on decision-making. Some organisations believe in rigid centralisation while others have faith in decentralisation and leave the routine decision-making function with the departmental heads.

Further, in the interest of the company it has been suggested that the policy matter decision must be left with the top management and leave the ordinary day to day routine matter decisions to the various departmental heads. External, Social, Political and Economic environment also influence decision-making. But instable political conditions in the country are not conducive to important decision-making.

3. Psychological Elements:

In psychological elements personal traits like preferences, intellectual maturity experience, educational standard, social and religious designation and status etc., of the person responsible for the decision-making also exert great influence on decision-making.

Further in company the manager’s habits, temperament, social environment, upbringing domestic life and political learning’s all have to trace his choice of alternative, consequently on his decisions.

4. Timing of Decisions:

Decisions must be taken at the appropriate time keeping in view the prevailing conditions. Marketing aim should also be taken into consideration and time required for achieving the aim. Any decision taken in time leaves a lasting impression on the mind of those who are affected by the decision.

5. Communication of Decisions:

When a particular decision has been taken it must be communicated properly in time to the persons concerned. Decision should be communicated to the subordinate executives in a courteous, simple and understandable language. There should not be any ambiguity in the language written. It should be in a vary simple language.

6. Participation of Employees:

Participation of the employees in decision-making makes its implementation easier. Employees participation has certain advantages and it ensures loyalty of the employees towards the organisation. It arouses the feeling of oneness with the company and the decision taken are considered as superior. It helps in enhancing the efficiency of the organisation which helps in attaining the goals of the organisation.

Importance of Decision Making in Management:

The Management and decision are two very important activities which cannot be separated. Both move together. Decision-making is the main business of management and it has been considered as soul of management. Decision should always be taken after a great deal of deliberations and it should be taken quickly and as far as possible intuition based.

Sound decisions are always information based and are a combination of:

(a) Judgement, and

(b) Information (on facts) based.

But information based decisions have many major problems, which arise at irregular intervals. Sound decisions live for a long time because it is very difficult and awkward to change decisions once they are made.

Scientific Process of Decision Making:

The process of decision-making has been divided under two heads:

1. Traditional method or Symptomatic Diagnosis.

2. Scientific method.

1. Traditional or Symptomatic Diagnosis:

This decision is taken on the basis of—limited knowledge, experience and intuitions. There is no scientific analysis involved in this. In this decision taken are not logical. This method is also known as “Symptomatic Diagnosis”. The Physicians in ancient times diagnosed the ailment on the basis of symptoms only.

In the same way the management also resolves the various problems facing the organisation on the basis of symptoms. Now-a-days an expert doctor relies not only on external symptoms but makes use of accurate X-ray, E.C.G. reports etc.

2. Scientific Method:

The process of taking scientific decisions is as follows:

(i) Defining the problem, objectives and constraints are studied.

(ii) Analysis of the problem.

(iii) Development of alternative solution is searched.

(iv) Deciding upon the best solution.

(v) Converting the decision into effective action.

(vi) Follow up the decision.

(i) Defining the problem, objectives and constraints are studied:

Under this process the nature of problem is considered. Here, a careful study of the external and internal aspects of the problem should be made carefully. The objectives of resolving the problem and constraints in the way of resolving it must also be given due weight-age in order to reach the correct decision.

(ii) Analysing the problem:

It involves careful appraisal of the alternatives and as such to decide which departmental executive should take the particular decision. Who others should be taken into confidence. Whether some specialists have also been consulted in this connection and who should be informed of such decisions.

It should be noted here that all policies and operating decisions should be taken by the top management while routine departmental decisions should be left to be taken by Departmental Heads. To make an important decision thorough analysis of relevant information is needed. If facts and factual information are not available, they may be estimated to the best of information available.

(iii) Development of Alternative Solution:

To develop alternate solutions following courses be adopted:

(a) Spending more on advertisement and publicity,

(b) Developing the market promotion activities, or

(c) Appointing more salesmen,

(d) Improving the quality of the product,

(e) Packaging should be more attractive or reducing the price etc.

Management should not depend on one solution alone, because if that fails under a peculiar situation the other one might be taken up in its place. It is therefore, essential to consider all possible course of action.

(iv) Deciding upon the Best Solution:

It is essential that the decisions be effective there must be co-ordinated, systematic and continuous information of all facts and situation. For example—All decisions on the marketing problem are taken on the basis of complete information available from internal and external sources. In deciding the best solution several factors have to be taken into consideration.

They are:

(a) The ratio of advantages and dis-advantages of each solution.

(b) Out of all the possible solutions which one is such that require the minimum amount of effort.

(c) What is the financial limitation of the organisation?

(d) Which solution is favourable to the circumstances after considering all these factors, the best possible solution should be decided upon?

(e) Now a day’s Operation Research Technique is employed in selecting the best alternative. Each alternative is quantitatively evaluated. Those which cannot be evaluated quantitatively is judged on the basis of experience, knowledge and intelligence.

(v) Converting the Decisions into Effective Action:

It is to be noted that a decision what so ever important it may be if not put into practice effectively it can serve no purpose. The decision taken must reach to the hands of all sub-ordinate officers and staff’ and all concerned employees and executives for whom it is meant.

The language of the decision must be simple and understandable. There must be full co-operation from the side of staff in its implementation. Staff should feel that the management decision is their own decision. While taking decision it is essential that sub-ordinates should be involved by their participation. Their participation will help in its implementation and it makes the matter quite simple, efficient and effective.

(vi) Follow up the Decision:

Decision making by scientific process is no guarantee that it is cent per cent correct. It is quite possible that it may be defective and might cause loss to the organisation. In order to minimise the chances of loss it in necessary that it should be followed carefully and shortcomings in the decision should be made up by taking suitable steps.

Therefore, the follow-up action has been considered a better scientific decision. Knowledge regarding business is never said to end and perfect, similarly marketing conditions are never stable. There is always uncertainty about the future. So all decisions must be taken considering all aspects of the business.

Principles of Decision Making:

Eminent authors of management are of this opinion that on right and appropriate decisions, the success and failure of the enterprise depend. Therefore, a manager has to take all precautions before arriving at a decision.

Following are the important principles which may be taken into consideration while taking decision:

1. Marginal Theory of Decision-Making:

This theory has been suggested by various economists. Economists believe that a business undertaking works for earning profits. To earn profit is their prime-motto. That is why they agree that the manager must take every decision with the aim in view that the profit of the organisation goes on increasing till it reaches its maximum.

The marginal analysis of the problem is based on law of diminishing returns. With extra unit of labour and capital put in production, the production increases but it increases at a proportionately reduced rate.

From every extra unit of labour and capital the production diminishes and a time comes when the increase in production stops with ‘zero’ as the production of the last unit used there in. At this stage a decision is taken to the effect that no additional unit of labour and capital now is required to be introduced in the production.

Production of the last unit is marginal one where-after further in-production of extra-unit becomes un-economical or non-yielding.

The marginal principle can be effectively and while taking decision on matters relating to:

(i) Production,

(ii) Sales,

(iii) Mechanisation,

(iv) Marketing,

(v) Advertising,

(vi) Appointment and other matters, where marginal theory can be scientifically and statistically used and a good decision is rendered possible.

2. Mathematical Theory:

There are few other theories like—venture analysis, game theory, probability theory, waiting theory. On the basis of which a manager analyses a given fact and takes decision accordingly. This has given rise to a scientific approach to the decision-making process.

3. Psychological Theory:

Manager’s aspirations, personality, habits, temperament, political leanings and social and organisational status, domestic life, technological skill and bent of mind play an important role in decision-making. They all in some form or the other leave an impact on the decision taken by the manager.

He is also bound by his responsibilities and answerability. Decision-making is a mental process and the psychology of those who are deliberating and of the person who takes the final decision has a definite say in decision-making.

4. Principle of Limiting Factors:

The decisions taken are based on limited factors nevertheless they are supposed to be good because of the simple fact that under the circumstances it was the only possibility.

From this principle it emerges that though there are numerous alternative available to a decision-maker but he takes cognizance to only those alternatives which suit the: (i) time, (ii) purpose, and (iii) circumstances and which can be properly and thoroughly analysed considering the human capacity and then finally one of the alternatives is chosen which form the basis of a decision.

5. Principle of Alternatives:

Decision is an act of choice. It is a selection process. Out of many available alternatives the manager has to choose on which he considers best in the given circumstances and purpose.

6. Principle of Participation:

This principle is based on human behaviour, human relationship and psychology. Every human being wants to be treated as an important person if it is not possible to accord him a V.I.P. treatment. This helps the organisation in getting maximum from every person at least from those who have been given the place of importance and honour.

Participation signifies that the subordinates even if they are not concerned should be consulted and due weightage should be given to their viewpoint. Japanese do this. Japanese business or institutions or government make decisions by consensus.

This makes all of them feel that they are very much part of the decision. The Japanese mostly debate a proposed decision throughout its length and breadth of the organisation until there is an agreement.

A few may disagree with Japanese method of decision-making because they may agree that it is not suited to our conditions. Such a method involves politicking, delays the decisions and sometimes may result into indecisiveness. But workers participation in decision-making can be ensured by the Japanese method.

Those favouring Japanese method and workers participation advance the argument that decisions are important. But according to modern thinking the decision should not be within the purview of only a selected few. Those who are to carry out the decisions must be actively associated with their decision-making also.

The principle of participation mostly aims at two things:

(1) It aims at the development and research of all possible alternatives. If larger number of people concerned are asked to search for alternatives on the basis of which decisions are expected to be taken then greater participation is assured which is surely an important aim of this principle.

(2) This principle asks for debating and deliberating by more and more people, so as to know the mind of all and to assess the possible reaction of a particular decision which the manager has in mind.

Why the Principle of Participation is becoming Popular?

The principle of participation is becoming popular due to the following reasons:

1. The participants feel that the business is their own of which they are important parts;

2. Opposition to a decision is considerably reduced and those who are to carry the decision are gladly accepting even if any change is being introduced;

3. Guidance and direction functions of management are being easily performed;

4. Decisions are the results of best possible selection of the alternatives, therefore decisions may yield results to the advantage of the organisation on the expected lines;

5. Increase in the efficiency of workers;

6. Development of co-ordinated efforts;

7. Development of good human relations.

8. Development of team spirit and better understanding because of good human relations; and

9. Assurance of growth and prosperity to both the organisation as well as the whole working force—managerial supervisory and operating.

Today the managers are more interested in eliciting the participation of workers with their decisions with a view to get more co-operations and to exercise effective control. Over them in the accomplishment of the tasks assigned by the objectives of the organisation.