Everything you need to know about the process of controlling. The management process will be incomplete and become useless without the control function.

Control is a tool that helps an organization measures and compares its actual progress with the established plan. Thus, control ensures what is done is what is intended. It is to be exercised by everyone in the organization, from top level to bottom level.

Managerial control is that process under which the standards of work are determined before the commencement of the work.

After this the actual work progress is evaluated, a comparison is made between the actual progress and the standard progress and if there is a difference the causes of this difference are sought to be known and corrective action is taken.

ADVERTISEMENTS:

The process of controlling involves the following steps: 1. Establishment of Performance Standards 2. Measurement of Performance 3. Comparison of Performance against the Standards 4. Analysis of Deviations 5. Initiating Corrective Measures 6. Feedback.

Learn about the Steps Involved in the Controlling Process

Process of Controlling – 6 Steps: Establishment of Performance Standards, Measurement of Performance and a Few Others

Step # 1. Establishment of Performance Standards:

Standards are simply criteria of performance without performance standards. There is no use measuring actual performance. Performance standards for output, cost product, time, sales, etc., should be established. Standards are to be fixed in measurable terms in terms of units, volume, value, time line, thickness, thinness, area, number, sharpness, etc. Thus fixation of standards is the first step in control process.

Requirements to be satisfied in formulating standards are:

i. Standards should be quantifiable as far as possible.

ADVERTISEMENTS:

ii. It should be objective and accurate.

iii. It should be scientific and not based on guess work.

iv. It should be acceptable and reasonable.

v. This should be alterable in the light of changes in the environment.

ADVERTISEMENTS:

vi. It should be clear and meaningful.

vii. It should be periodically revised to keep up to date.

viii. It should focus on strategic points.

Step # 2. Measurement of Performance:

The second step in control process is measurement of actual performance. The purpose behind this step is to generate information about the individuals, groups or units. The means of measurement depends on the type of standards set. Where the standards are set in quantifiable terms, like volume, of goals produced, time taken to complete a task, number of days, number of customers, size of revenues, value, height, weight, length, breath, thickness, thinness, smallness, largeness, etc. the quality of measurement is sound.

It may be free from bias. However, sometimes standards cannot be set in quantitative terms for certain abstract items like employee morale, employer brand, reputation, location advantage, skill and competency level of employees, safety, work climate, attitude, etc. In such a case, they have to be either converted into numerical measures using some scales and measure the performance, or they should be left to subjective judgement of superiors.

Performance data are collated from personal observation, statistical data, oral report, written report, accounting information, sample checking, performance report, etc. After the advent of sophisticated software packages, managers do not have any problem in measuring both quantitative and qualitative performance.

Step # 3. Comparison of Performance against the Standards:

Under this phase, managers have to decide the permissible level of deviation or tolerance limit. If this is not laid down, minor variations may consume a lot of time of the executives and significant deviation may escape the attention of the manager. This range may vary from industry to industry and company to company and product to product.

The focus on major deviation involves the concept of management by exception. For example, even minor deviation is a serious concern in the case of precision equipments like scanner, lens, thermometer, x-ray, quality of chemicals, drugs, etc. Therefore, range of tolerance should be fixed. Where the results are intangible, direct personal observation or reports may be used to spot out defects/deficiencies.

Step # 4. Analysis of Deviations:

The causes of deviations should be probed. It may be due to many factors like lack of adequate skill on the part of employees, poor training, poor inter-personal relationship among workers, lack of adequate infrastructure facility, defective communication, unrealistic target, change in public policy, etc. The manager has to examine the causes for deviation. He/she has to find out the root cause of deviation. It may be due to controllable or uncontrollable factors. Analysts should have a critical bend of mind.

Step # 5. Initiating Corrective Measures:

ADVERTISEMENTS:

Once the cause of deviation is diagnosed, then the manager has to intervene to address it through right measures. If it is due to individual factor, he/she has to think of arranging training to employees to up skill them or enhance the knowledge of employees. If the deviation is due to external factors, the manager has to think of improving the quality of inputs like machines, materials, work environment, tools, etc.

Suppose it is externally-induced like change in public policy, competitor’s action, economic cycles, natural calamities and so on, a strategy has to be put in place and accordingly revise the standard. Sometimes non-attainment of standards may be due to lapses committed in fixing standards. In such a case, standards themselves have to be corrected.

Those who have attained the standards or those who have surpassed the standards need to be suitably recognized by reward of incentives or award of certificates or by some privileges so that they continue to reinforce the positive performance.

Step # 6. Feedback:

The person as well as the management has to be given feedback of performance (both positive and negative).

Process of Controlling – 7 Steps Involved in the Controlling Process

ADVERTISEMENTS:

There is a strong relationship between planning and controlling. The steps in controlling therefore are preceded by two important steps of planning.

Setting of objectives for managers, units and departments is necessary to provide them clarity on the expectations from them. On the basis of the objectives, standards or benchmarks are identified during the planning process. These standards are the specific objectives against which progress can be measured for various parameters.

Having established the standards, we proceed with the steps of controlling:

1. Select Suitable Measuring Instruments for Various Parameters:

ADVERTISEMENTS:

Measuring instruments have to be selected keeping in view the characteristic of a parameter in the standard to be measured. For example, if we are trying to measure the customer satisfaction level, a survey instrument may have to be designed with appropriate questions in the questionnaire.

If we are gauging the number of defective integrated circuits (ICs) being produced by a production process, we would need suitable electronic instruments to test the ICs coming out of the production process. In addition, we would need to decide if we would like to test each and every IC being produced or only a select few (a suitable sample) to assess if the process is working fine.

2. Measure Actual Performance for a Parameter:

Using the measuring instrument selected earlier, measurement of the parameter is done. Care is taken to ensure that each and every time the measurement is done with accuracy for authenticity of the measurement data.

3. Compare Actual Performance with the Benchmark:

In this step, the data pertaining to the measurements of actual performance of a parameter is compared with the desired levels of performance specified in the standard/benchmark established earlier.

ADVERTISEMENTS:

4. Is there a Gap between Actual and Desired?

This step is a decision point where it is determined if a gap exists between the actual and the desired performance of the parameter in the process. If no gap exists, the process is continued as it is.

5. Is the Variation within Acceptable Limits?

If a gap or variation does exist between the actual and the desired performance, it is ascertained if this gap is within acceptable limits of variation. This is because some variation is natural due to inherent characteristics of the process.

For example, if the specification of the diameter of a shaft has been prescribed as 3 cm ± 0.002 cm, any variation in the actual measurement of the diameter between 2.998 cm and 3.002 cm would be acceptable. However, a value of the measurement exceeding these limits (less than 2.998 cm or more than 3.002 cm) would indicate that the production process is out of control. However, when the variation is between the prescribed limits, the process is continued as it is.

6. Is the Standard Valid and Acceptable?

ADVERTISEMENTS:

Before taking any action on the variation detected, it is important to verify if the standard established earlier is still valid and acceptable or not. This is because the expectations from the process may increase by the passing time, and the top management may like to set higher performance standards. For example, the client who sources shafts from a manufacturer may come up with a more stringent specification for its diameter as 3 cm ± 0.001 cm.

i. Revise the Standard:

If it is clear that the earlier standard is not valid or acceptable anymore, it should be revised. In our example of the shaft, it should be revised as per the client’s request to 3 cm ± 0.001 cm.

ii. Identify Assignable Causes of Variation:

However, if the earlier standard is still valid and acceptable, the assignable causes of variation are looked into. The assignable causes of variation may be due to wear and tear of the tools on the machine producing the item, lack of proper skills on part of the worker operating the machine, or worker fatigue, etc.

7. Rectify the Causes of Variation:

ADVERTISEMENTS:

Once the assignable causes of variation have been identified, corrective action is taken to bring the process back in control. In our example, if it has been found that the variation was due to lack of skills on part of the worker operating the machine, the rectification would involve the proper training of the worker to improve his skills, especially in relation to the mistakes committed by him.

After the cause for variation has been rectified, the control loop continues at step 2, i.e. measurement of the actual performance of the parameter, followed by further steps in the control loop.

Process of Controlling – Measurement of Performance, Comparison between Performance and Standards and Correction of Deviations from Standards

The various steps in controlling may broadly be classified into four parts:

1. Establishment of control standards,

2. Measurement of performance,

3. Comparison between performance and standards and the communication, and

ADVERTISEMENTS:

4. Correction of deviations from standards.

Process # 1. Establishment of Control Standards:

Every function in the organizations begins with plans, which are goals, objectives, or targets to be achieved. In the light of these, standards are established which are criteria against which actual results are measured. For setting standards for control purposes, it is important to identify clearly and precisely the results which are desired.

Precision in the statement of these standards is important In many areas, great precision is possible. However, in some areas, standards are less precise. Standards may be precise if they are set in quantities-physical, such as volume of products, man-hours or monetary, such as costs, revenues, and investment.

They may also be in other qualitative terms, which measure performance. After setting the standards, it is also important to decide about the level of achievement or performance, which will be regarded as good or satisfactory.

There are several characteristics of a particular work that determine good performance.

Important characteristics, which should be considered while determining any level of performance as good for some operations are-

(i) Output,

(ii) Expense, and

(iii) Resources.

Expense refers to services or functions, which may be expressed in quantity, for achieving a particular level of output. Resources refer to capital expenditure, human resources, etc. After identifying these characteristics, the desired level of each characteristic is determined. It should be reasonable and feasible. The level should have some amount of flexibility also, and should be stated in terms of range-maximum and minimum.

Control standards are most effective when they are related to the performance of a specific individual, because a particular individual can be made responsible for specific results. However, sometimes accountability for a desired result is not so simply assigned; For example, the decision regarding investment in inventory is affected by purchase, rate of production and sales. In such a situation, where no one person is accountable for the levels of inventories, standards may be set for each step that is being performed by a man.

Process # 2. Measurement of Performance:

The second major step in control process is the measurement of performance. The step involves measuring the performance in respect of a work in terms of control standards. The presence of standards implies a corresponding ability to observe and comprehend the nature of existing conditions and to ascertain the degree of control being achieved.

The measurement of performance against standards should be on a future basis, so that deviations may be detected in advance of their actual occurrence and avoided by appropriate actions. Appraisal of actual or expected performance becomes an easy task, if standards are properly determined and methods of measuring performance which can be expressed in physical and monetary terms, such as production units, sales volume, profits, etc., can be easily and precisely measurable.

The performance, which is qualitative and intangible, such as human relations, employee morale, etc., cannot be measured precisely. For such purposes, techniques like psychological tests and opinion surveys may be applied. Such techniques draw heavily upon intuitive judgement and experience, and these tools are far from exact.

According to Peter Drucker, it is very much desirable to have clear and common measurements in all key areas of business. It is not necessary that measurements are rigidly quantitative. In his opinion, for measuring tangible and intangible performance, measurement must be

(i) Clear, simple, and rational,

(ii) Relevant,

(iii) Direct attention and efforts, and

(iv) Reliable, self- announcing, and understandable without complicated interpretation or philosophical discussions.

Process # 3. Comparing Actual and Standard Performance:

The third major step in control process is the comparison of actual and standard performance.

It involves two steps:

(i) Finding out the extent of deviations, and

(ii) Identifying the causes of such deviations.

When adequate standards are developed and actual performance is measured accurately, any variation will be clearly revealed. Management may have information relating to work performance, data, charts, graphs and written reports, besides personal observation to keep itself informed about performance in different segments of the organization. Such performance is compared with the standard one to find out whether the various segments and individuals of the organization are progressing in the right direction.

When the standards are achieved, no further managerial action is necessary and control process is complete. However, standards may not be achieved in all cases and the extent of variations may differ from case to case. Naturally, management is required to determine whether strict compliance with standards is required or there should be a permissible limit of variation.

In fact, there cannot be any uniform practice for determining such variations. Such variations depend upon the type of activity. For example, a very minute variation in engineering products may be significant than a wide variation in other activities. When the deviation between standard and actual performance is beyond the prescribed limit, an analysis is made of the causes of such deviations.

For controlling and planning purposes, ascertaining the causes of variations along with computation of variations is important because such analysis helps management in taking up proper control action. The analysis will pinpoint the causes, which are controllable by the person responsible. In such a case, person concerned will take necessary corrective action. However, if the variation is caused by uncontrollable factors, the person concerned cannot be held responsible and he cannot take any action.

Measurement of performance, analysis of deviations and their causes may be of no use unless these are communicated to the person who can take corrective action. Such communication is presented generally in the form of a report showing performance standard, actual performance, deviations between those two tolerance limits, and causes for deviations. As soon as possible, reports containing control information should be sent to the person whose performance is being measured and controlled.

The underlying philosophy is that the person who is responsible for a job can have a better influence on final results by his own action. A summary of the control report should be given to the superior concerned because the person on the job may either need help of his superior in improving the performance or may need warning for his failure.

In addition, other people who may be interested in control reports are:

(i) Executives engaged in formulating new plans; and

(ii) Staff personnel who are expected to be familiar with control information for giving any advice about the activity under control when approached.

Process # 4. Correction of Deviations:

This is the last step in the control process, which requires that actions should be taken to maintain the desired degree of control in the system or operation. An organization is not a self-regulating system such as thermostat which operates in a state of equilibrium put there by the engineering design. In a business organization this type of automatic control cannot be established because the state of affairs that exists is the result of so many factors in the total environment.

Thus, some additional actions are required to maintain the control.

Such control action may be:

(i) Review of plans and goals and change therein on the basis of such review;

(ii) Change in the assignment of tasks;

(iii) Change in existing techniques of direction;

(iv) Change in organization structure; provision for new facilities, etc.

In fact, correction of deviation is the step in management control process, which may involve either all or some of the managerial functions. Due to this, many persons hold the view that correcting deviations is not a step in the control process. It is the stage where other managerial functions are performed. Koontz and O’Donnell have emphasized that the overlap of control function with the other merely demonstrates the unity of the manager’s job. It shows the managing process to be an integrated system.

Process of Controlling – Five Chief Basis of Controlling Process – Setting Performance Standards, Measurement of Actual Performance, Analysing Deviations and a Few Others

Managerial control is that process under which the standards of work are determined before the commencement of the work. After this the actual work progress is evaluated, a comparison is made between the actual progress and the standard progress and if there is a difference the causes of this difference are sought to be known and corrective action is taken.

In this way there are five chief basis of controlling process which are as under:

(1) Setting Performance Standards

(2) Measurement of Actual Performance

(3) Comparison of Actual Performance with Standards

(4) Analysing Deviations

(5) Taking Corrective Action

(1) Setting Performance Standards:

The first step of controlling is to set performance standards. Standards are those criterias on the basis of which the actual performance is measured. Only standards tell individuals and departments about their destination. A manager evaluates the actual performance on the basis of these standards and finds out the deviations.

Standards are of the following two types:

(i) Quantitative Standards:

They are the standards which are shown with the help of figures, e.g., production of 10 units by a labourer in a day, total cost per unit comes to 100 rupees, etc.

(ii) Qualitative Standards:

They are the standards which cannot be shown in the form of figures, e.g., increasing the morale of the employees. Measuring the morale of the employees is a standard of qualitative nature. It cannot be measured directly. In order to measure it, the labour turnover rate, absenteeism rate, dispute rate, etc. have got to be taken into consideration. In case the rate of all the three is lower, it can be said that there has been an increase in the morale of the employees.

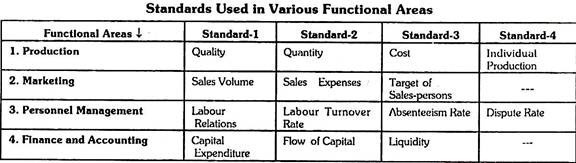

There are chiefly four basis for setting standards – (1) Quantity, (2) Quality, (3) Time, and (4) Cost.

Quantity Standards are related to production, sales, stock, etc. Quality Standards are related to raw material finished goods, customers’ service and employees’ morale. Time Standards refer to the time consumed in the production of goods. Similarly, Cost Standards refer to labour, material and other expenses.

Functional Areas and Standards:

Standards set for the functional areas are chiefly the following:

Factors to be considered while Deciding Standards:

Following facts should be kept in mind while setting standards:

(i) Standards should be easily obtainable.

(ii) Standards should be measurable.

(iii) Standards should be flexible so that changes can be introduced according to the changing situations.

(iv) Standards should be simple and clear so that the people for whom they are laid down should understand them easily.

(v) Deviation tolerance limit should also be clarified while setting standards. For example- there is no cause of worry if the production of 1950 units instead of 2000 units is achieved. By doing so unnecessary corrective action shall not to be taken on such an insignificant deviation.

(2) Measurement of Actual Performance:

The second step in the control process is the measurement of actual performance. The measurement of actual performance is done on the basis of pre-determined standards. The measurement of actual performance tells the manager whether the work has been done according to the plan or not.

An important question regarding the measurement of actual work that arises is whether the measurement of performance can be done only after the actual work is completed or it can be measured during the course of its completion. In reply to this question, it will be appropriate to say that the progress can be measured in both the situations.

Firstly, when the work is in progress it should be ascertained through the medium of supervision whether the work is progressing at a good speed or not so that in case of negative results corrective action can be initiated immediately to avoid any further loss to the remaining work. Secondly, when the whole work has been completed. In this case corrective action, in case of negative result, can be taken for future work which means that the loss that has been caused cannot be compensated.

The following facts should be kept in mind while measuring the actual performance:

(i) The figures regarding work progress should, as far as possible, be completely true.

(ii) These figures should be continuously prepared.

(iii) The standards for measuring progress should be the same as were adopted at the time of determining standards.

(iv) Progress measuring system should be quick to point out deviations.

(3) Comparison of Actual Performance with Standards:

At this step, actual performance is compared with the standards and deviations are found out. Deviations can be of two types – (i) Negative Deviation and (ii) Positive Deviation. In the controlling process, it is important to know the causes of negative deviation but it is not less important to know about the causes of positive deviations. Positive deviation means that the actual performance is more than the standard work.

If the information received regarding the actual performance being more than the standard, the corrective action can help in improving the efficiency in future.

(4) Analysing Deviations:

At this stage, deviations are analysed.

In the analysis of deviations, following things are studied:

(i) Is Standard Being Attained?

If yes, nothing is needed to be done. The work will continue as usual, the actual performance will be measured and remaining process will be completed. Contrary to this, if the standard could not be achieved, answer to the next question will have to be found.

(ii) Is Deviation Acceptable?

If the actual performance is below the standard, but the deviation is acceptable (meaning thereby that the deviation is not so serious that it needs corrective action) nothing is to be done and the work will go on as usual. Contrary to this, if the deviation is not acceptable, answer to the next question will have to be found.

(iii) Is Standard Acceptable?

If the standard is acceptable which means that nothing is wrong with it, the cause of deviation will be located. After this, corrective action will be taken and the work will progress. Contrary to this, if the standard already fixed is found to be wrong, answer to the next question will have to be found.

(iv) Revising the Standard:

If the standard is found to be wrong, it will have to be refixed. Thus, a new standard will be set, actual performance will be measured and process will continue.

Deviations are examined in the light of pre-determined Deviation Tolerance Limits. If the deviations are within limits they can be avoided. But if they cross the limits, they should be reported to the higher level managers without any delay.

There are two important principles regarding this:

(i) Principle of Critical Point Control:

According to this principle, those points or activities should be determined in the very outset which has an important role to play in ensuring the actual work progress in accordance with the plans. These are known as Key Result Areas – KRAs. It means that the managers should not be involved in small insignificant activities but should pay more attention to those activities where unfavourable results can cause heavy loss to the enterprise.

(ii) Principle of Exception:

According to this principle, control will be effective in proportion to the efforts of the manager to focus his attention on more important exceptions. Here, important exceptions mean the especially good or especially bad deviations. It means that the managers should take corrective action, from the point of view of control, in respect of those deviations, only after an in-depth study, which are either too good or too bad.

It has been laid down in this principle that action should not only be taken in respect of bad or negative deviations but also in case of good or positive deviations after ascertaining their causes so that efforts can be made to bring in more improvement. For example- if the sales exceed our expectation, it will be called positive deviation and in case its cause can be good advertisement, sale scan be promoted by paying more attention to advertisement.

It is important to clarify the difference between the principle of critical point control and the principle of exception. Under the principle of critical point control, it is sought to be understood on which points or activities control will be profitable, while in the principle of exception deviation is taken care of in respect of the pre-determined critical points and in case of more deviation in respect of some particular critical point corrective action is taken.

Advantages of Critical Point Control and Management by Exception:

The following advantages are obtained by following these principles:

(i) By taking care of important deviations both time and efforts are saved.

(ii) The managers remain focussed on important areas.

(iii) By delegating authority to handle less important problems to the subordinates helps in raising their morale.

(iv) By locating important problems quickly, possible loss can be avoided.

Following are the possible causes of deviations:

(i) Human Causes – The efficiency of the employees is chief among the human causes.

(ii) Uncertain Events – It includes strikes, lockouts, shortage of raw material, entry of many competitors in the market, etc.

(iii) Various Hurdles – It may include the breaking of machines, hurdle in electric supply, etc.

(iv) Wrong Standards – It may be the form of making a wrong estimate about sales, profits, costs, etc.

In this way, deviations and their causes are traced out and then reported to the concerned officers for taking corrective action.

(5) Taking Corrective Action:

The last but the most important step in the control process is taking corrective action. By the end of the third steps, the deviations and their causes become known. Now is the turn of removing the hurdles in the actual work progress.

The purpose of corrective action is to bring the actual work progress to the level of expected progress.

This includes two types of arrangement:

(i) Removing Deviation in the Actual Performance:

If the production has declined because of some defect in the machines, it should be immediately got rectified and the employees should be asked to work overtime to compensate the loss in production.

(ii) Stopping the Repetition of any Such Problem in Future:

For example- making an in depth study of the causes of the defects in machines and take such steps as will prevent any such problem in future.

Factors to be Considered while Taking Corrective Action:

The managers should take care of the following facts while taking corrective action:

(i) Corrective action should be taken only after a careful inquiry into the causes of deviations.

(ii) If the wrong standards had been determined, they should be modified.

(iii) Corrective action should be taken only by the manager who is directly connected with the work.

(iv) Action should be immediately taken so that loss can be avoided in future.

(v) If necessary, changes should be introduced in the policies, procedures, rules, etc.

(vi) Corrective action should be of such a type which is liked by the people engaged in the actual work performance.

(vii) Positive deviations should be found and efforts should be made for further improvement so that efficiency increases in future.

A special feature of the corrective action is that control does not come to an end only with the implementation of corrective action but it has to be observed as to what effect it has created on the actual results and if the results again happen to be negative, corrective action should again be taken. That is why it is said that control is a continuous process.

Process of Controlling – 3 Steps of the Basic Control Process

Control techniques and systems are basically the same regardless of what it is being controlled; the basic control process involves three steps:

(1) Establishing standards;

(2) Measuring performance against these standards and plans; and

(3) Corrective variations from standards and plans.

(1) Establishment of Standards:

Because plans are the yard sticks against which managers devise controls, the first step in the control process logically would be to establish plans. However, since plans vary in details and complexity and since managers cannot usually watch everything, special standards are established. Standards are by definition simply criteria of performance. They are the selected points in an entire planning programme at which measures of performance are made so that manager can receive signals about how things are going and thus , do not have to watch every step in the execution of plans.

Theoretically, setting up of standards of controlling is a simple task. In actual practice, however, it is not so, as it necessary to take three important steps before attempting to compare actual performance with the standards.

These are:

(i) Ensuing that the standards established are clear and meaningful;

(ii) Identifying responsibility for different goals with individuals; and

(iii) Selecting strategic points for setting up standards.

Prof. Newman has suggested that the control points should be – (i) Timely, (ii) Economical, (ii) Comprehensive, and (iv) Balanced. These guidelines are helpful for selecting strategic control points. While establishing standards, it should be noted that there are many kinds, of standards.

(2) Measurement of Performance:

Although such measurement is not always practicable, me measurement of performance against standards should ideally be done on a forward-looking basic so that deviations may be detected in advance of their occurrence and avoided by appropriate actions.

In order to compare actual performance with the goals and standards established, there are three usual methods in use:

(i) Prior Approval;

(ii) Checking only the Exceptional; and

(iii) Personal Observation.

(i) Prior Approval:

Many managers insist on prior approval before allowing a work to proceed as they need the assurance that the standards laid down will be maintained. Also, they feel confident that the works is proceeding as planned when they have checked it at every step. However, this method is cumbersome and it is likely to cause delay in action.

(ii) Checking the Exceptional:

Ordinarily, a large part of activities of any enterprise must proceed without waiting for approval of some higher executive. The purpose of control, then, is to appraise current and completed action, in order to provide a basis for regulating future activities, by concentrating on unexpected or unusual results. This is called the Principle of Exception. It means that as long as operations go according to plan, there is no need to submit reports; only when unexpected results occur, there is need for reports and corrective action.

Consequently, control authorities make it a rule that reports shall be submitted on unexpected or unusual results; and in the absence of such reports, they would presume that all activities are proceeding as planned. This arrangement will work only if plans clear to all managers and their subordinates, and if responsibility for reporting is suitably located. This method is, usually, suitable for routine activities.

(iii) Personal Observation:

The third method of checking performance is personal observation, which has been recognized by military authorities as a very valuable method. Top executives of many business enterprises also make frequent visits to their plants and their regional sales offices. Depending upon his abilities to visualize situations and to feel the atmosphere, an executive may be able to get a realistic mental picture of the operating situation, an acquaintance with the people involved, and understanding of the attitude and reactions of employees and customers.

All this would add up to a good understanding of what is, and what is not, happening an understanding which he can never hope to get from written report. An executive who has been to the factory in the morning or who has talked to customers or salesman in the field a week before is in a better position to understand and appraise other reports on performance that he has received. Moreover, his personal contacts with the rank and file will always have a favourable effect on their morale.

Reporting:

Having checked the performance, the next step is to prepare a report for action. Such a report to be of any value should be submitted as promptly as possible after checking. Prompt reporting in the first instance, helps in diagnosing the situation. Secondly, promptness of a report can add significantly to the effectiveness of control.

As regards contents of a report, there is a general impression that the more information it contents, the more useful it is for control purposes. This, however, is not always true. Men of action like engineers and salesmen, primarily interested in results, find the work of preparing detailed reports time consuming and somewhat irritating and irksome. This makes it necessary to make the report as brief as possible.

This is in the interest of the person who has to prepare that report, as well as, the person who has to read it and take action on it. Nevertheless, such a report should briefly contain a comparison of actual performance with the standards set, a short explanation for wide variations from standards, and if possible, proposal for remedial action.

(3) Correction of Deviations:

Correction of deviations is the point at which control can be seen as a part of the whole system of management and can be related to the other managerial functions. The third step of taking corrective action is imperative before there is any visible control. The correction of deviations should begin with an investigation of why the errors occurred. Sometimes a planning premise may have been wrong.

Sales may have been lower than anticipated because of an overly optimistic forecast or a strike in the plant may have caused unexpected delays in production. The cause of the deviation will help determine the appropriate action. But a key point to be noted here is that some problems are no one’s fault. Again, not all deviations are directly attributable to any single individual or group. And. if management tries to assess blame for every error, employee attitudes toward work may suffer, in which case the short term success in appraisal could lead to a long-term productivity decline.

Of course, there are times when a manager will make an error in judgement or a worker will handle an order improperly. When this happens, if the errors are grave or habitual, corrective action may require the replacement of the individual or the assignment of additional training. However, the action can be determined only after the specific causes of the deviation have been evaluated.

After the cause is identified, problem solving measures can be taken.

This may be achieved by taking the following measures:

(i) Adjustment of physical conditions or external situation;

(ii) Review of direction, training and selection; and

(iii) Modification of earlier plans and targets.

(i) Adjustment of Physical Conditions:

Operating plans and goals are based on forecasts, regarding future conditions. However, actual conditions may turn out to be different because of unexpected developments and as a results, variations occur between achievements and targets. It is, however, the responsibility of a manager to attempt to make conditions conform to the forecasts, as far as practicable. He can do this in a number of ways; he will try to ensure that raw-materials come in time and that semi-processed goods move from department to department in time.

Again, if there is a breakdown of any machinery, he would arrange for spares or for prompt repairs, with minimum interruption to production processes. He will also try his best to maintain satisfactory working conditions. Thus, in a variety of ways, he could try to influence physical conditions and external situation in such a way as to facilitate achievement of goals and targets.

(ii) Review of Direction, Training and Selection:

A second broad area for corrective action is in making sure that individuals entrusted with responsibilities are properly directed, quite often, failure to meet standards can be traced to inadequate direction and an executive, therefore, should review, with the subordinates, the instructions given and find out reasons. This would enable him to give clear, complete and reasonable instructions in future.

If, however, the failure has been due not to incomplete understanding of instructions but to lack of training and experience on the of a subordinate, the corrective action might consist of providing suitable training to him as soon as possible. If he learns to handle is job satisfactorily, within a reasonable time after training, he should be kept on the job. But if it is discovered that he lacks some of the basic abilities required to perform his job, he should be replaced by a more capable individual, and he may be transferred to a job for which he is more suited.

(iii) Modification of Plans and Targets:

It is well known that there are many external factors such as Government policies, social developments, nature of competition etc., which cannot be adjusted by executive action and which have to be accepted as facts of the situation. The alternative for an executive then is to revise his plans in the light of these factors. Similarly, it may not always be possible to arrange for prompt replacement or repairs whenever there is a break-down of machinery.

Then he must revise his schedule of production and if necessary, adopt a different method of production. A careful review of operating experience might also suggest ways and means to improve standing plans. It may be that standards set have been too high, or that policies need clarification to avoid frequent exceptions, or methods require modifications to make better use of available facilities or personnel.

If, fortunately, on the other hand, operating results turn out to be much better than established standards, attempt should be made to discover the reasons and if it is found that the better results are due to the prevailing policies, they may be modified suitably as standard procedures.

Thus, mangers may correct deviations by redrawing their plans or by modifying their goals. Or they may correct deviations by exercising their organizing function through reassignment or clarification of duties. They may correct also by additional staffing, by better re-staffing measure, firing. Or again they may correct through better leading-fuller explanation of the job or more effective leadership techniques.

Establishing Effective Feedback:

An ideal control system provides timely feedback that can be used to monitor and correct deviations. With the information provided by such a system, the organization can monitor activities, identifying those that are not in accord with plans and taking the necessary corrective action.

In attaining feedback, the manager can use various control techniques. Some of the more traditional ones, include budgeting, break-even analysis, personal observation, and personal performance evaluation. Some of the more specialized, entail Information design and time-event analyses, such as – PERT and milestone scheduling. Since these analytical techniques are not designed to control overall performance, the manager needing overall performance control can simply turn to such other techniques as profit and loss, return on investment, key area control and auditing.

Control by Reports:

Control is now synonymous with ‘control with the help of reports about the performance’. This type of control is not so important for a small sized business. However, as the size increases, this becomes more and more indispensable. The reports are, thus, submitted from bottom to top to convey the actual situation about costs, production, sales, labour turnover, etc.

Similarly reports flow from top to bottom about the results that are expected at various levels and about the corrective action to be taken where actual situation deviates from that prescribed. Reporting system does not directly contribute to profits, the way production and sales departments do. It is, however, essential to ensure that everything goes as expected. In the absence of such a system it would is expected of them. Similarly, few of the higher levels would know the actual facts.

The results could well be disastrous, particularly when organization is sufficiently large to prevent direct personal contact of superiors with actual situation. These conflicts would not just be hypothetical. Drucker has remarked that, like seven blind men viewing an elephant, every manager thinks his function to be supreme, sometimes at the cost of other functions. Controller would have to use his knowledge to avoid such a situation. His guiding motive, however, is apparent which is the goal of the entire organization.

Reports:

The reports to be submitted to various levels of management depend basically on the requirement of the particular situation. The purpose is to over all relevant aspects of the organization through such reports.

For instance, in the case of a company manufacturing paper boxes, following reports were used by the company:

(1) Monthly Balance Sheet;

(2) Monthly Profit and Loss Account;

(3) Department-wise Expenses Report;

(4) Sales and Administrative expenses report;

(5) Overdue account, receivable;

(6) Inventory Report, monthly;

(7) Salesman-wise breakdown of sales, monthly;

(8) Quality control report, monthly;

(9) Overdue deliveries, weekly;

(10) Raw material wastage report, weekly;

(11) Weekly sales report;

(12) Comparison of actual sales with budgets, weekly;

(13) Machine production report, weekly;

(14) Outstanding orders, weekly;

External Reports:

(1) Quarterly economic report on trends in paper box industry

(2) Industry statistics

(3) Industry operation results (competitors’ performance)

(4) Paper board (raw-material) production.

Another aspect to be considered before designing reporting system is the ‘Organization Chart’ of the company. This could facilitate presentation on only such information to each executive as it most essential for his work.

Like reporting system, another device commonly used to maintain control is budgetary control system. Budget specifies the performance expected of each department, section and individual in terms of cost and revenue. This needs to be necessarily in quantitative terms to achieve exactness.

The success of a budgetary control system depends on the following to factors:

(i) The realistic formulation of budget; and

(ii) Constant feedback on actual performance to be compared with the budget. This would facilitate quick corrective action.

Advantages of Budgetary Control:

Because budgets are measured in financial terms, the information which has to be gathered for budgetary control purposes can be handled by the normal accounting facilities. Budgetary control is, therefore, relatively, simple and cheap. Deviations can be detected quickly, permitting rapid feedback for the responsible manager to take corrective action.

Secondly, benefits of the budgetary control process are that the discussions in which managers are involved when budgets are set, improve general coordination. The information gleaned during the process is also useful for future planning, and can form the basis of performance-related-reward systems.

It also provides a common yardstick for comparing the effectiveness of control in departments with widely differing activities, and for controlling waste.

Disadvantages:

Budgetary control also its defects. The formulation of budget is often marked by political and protective manoeuvring. The budget loses much of its utility as a result. In some cases, achievement of budget targets carries a risk of getting the targets elevated next year and managers are not quite enthusiastic of meeting their targets as a result. In the case of some companies, for example, spending within the budget leads to curtailment of budget for the next year which leads to extravagant spending at the end of the year.

Another objection against the budgetary control system is that it reduces the time-perspective for performance to one year only.

Budgets have also found to psychologically pressurise the employees to such an extent that they resent this system and resort to short cuts to achieve their quotas.

Process of Controlling – Establishment of Standard of Performance, Measurement of Actual Performance, Analysing the Causes of Deviation & Taking Corrective Action

i. Establishment of Standard of Performance:

Standard represents the planned performance to be achieved during a specified period. Standard of performance are generally determined keeping in view the capability and competence of the employee concerned. Standard is the yardstick with which actual performance is to be compared. The control process starts with the establishment of standards and methods for measuring the performance. Standards should be fixed in the light of objectives set by the top management. Standards must be neither too high nor too low for any performance achievement. Normally, standards are set in quantitative terms (such as time, cost, money, output, man-hours, etc.).

ii. Measurement of Actual Performance:

The second step in the control process is to measure the actual performance. The actual performance should be measured and expressed in the same unit as the planned performance. There are several techniques for the measurement of performance (such as personal observation, sample checking, management by exception, etc.).

A sound management information system should be developed for timely and accurate measurement of performance. The measurement and reporting of actual performance may be done at periodical intervals (weekly, monthly, quarterly, and yearly, etc.). The performance should preferably be measured in quantitative terms as far as possible.

iii. Comparison of Actual Performance with the Standards:

The third step in the controlling process is to compare the actual performance with the predetermined standards. The purpose of comparison is to find out the extent of deviation and to identify the causes of deviation. If actual performance matches with the standard, the manager feels that everything is within his control. When actual performance exceeds the standard performance, the manager should appreciate the employees for their achievement.

If actual performance falls below the standard performance, the manager should take immediate remedial action so that such a situation does not recur. Comparison of performances helps in quick location of defects and results in rectification with minimum losses. All deviations need not be reported to the management. Only deviations beyond the reasonable limit should be brought to the notice of the top management.

iv. Analysing the Causes of Deviation:

The manager identifies and investigates various deviations so as to get into the possible causes responsible for such a situation. There may be various reasons for adverse deviations (such as defective processes, inadequacy of resources, structural drawbacks, lack of proper monitoring, organizational constraints, external constraints, etc.). Therefore, it is necessary to identify and isolate the appropriate causes of adverse deviations.

v. Taking Corrective Action:

Any corrective action is initiated on the basis of careful analysis of possible causes of deviation. All controlling activities terminate at this point. Corrective actions are employed taking note of the nature and type of deficiencies occurred. A corrective action may involve a change in production method, modifying the existing process, change in the method of selection of workers, change in the nature of supervision, use of quality materials, improving the physical conditions of work, etc. Therefore, the essence of controlling lies in taking suitable corrective action so as to improve performance.

Process of Controlling – 5 Important Steps with Examples

Step # 1 – Setting Performance Standards:

The first step in the controlling process is setting up of performance standards as criteria against which the actual performance is compared and evaluated. The standards can be quantitative or qualitative.

Quantitative standards are expressed in terms of values like cost, revenue, volume or time. Precisely expressed quantitative standards make comparisons easier and meaningful.

Qualitative standards are the subjective standards set to improve performance of the organisation for example, discipline amongst employees, behaviour of sales people, customer satisfaction etc.

The standards must be flexible so that they can be modified to incorporate changes in the internal and external business environment.

Examples of quantitative standards are:

i. Standard cost to be incurred to produce a product. Mediline Ltd. decided that they will import induction cookers from China at maximum price of $12 each.

ii. Price at which the product should be sold. Mediline Ltd. informed its sales staff that the induction cookers will be sold at a minimum selling price of Rs.1500 each.

iii. Number of units to be produced and sold. Mediline Ltd. decided to import 10,000 pcs of induction cookers three months before Diwali.

iv. Standard time to perform a specific task. Each worker must take maximum of 10 minutes to pack the product.

Examples of qualitative standards are:

i. Improve efficiency – All goods must be dispatched within 24 hours to maintain efficiency or production must not have more that 5% defective units.

ii. Motivate employees – Managers sets targets for sales executives and announce financial and non-financial incentives for achieving set target.

iii. Company will exchange goods if customers’ report poor quality for more than 5% of goods supplied.

Step # 2 – Measurement of Actual Performance:

The next step after setting standards is measurement of actual performance in an objective and reliable manner. For effective control and easy comparison the actual performance should be measured in the same units in which the standards are set. The actual performance may be measured either after the task is completed or during the performance or happening of the task.

Small organisations can measure the performance of every task performed but it is not possible for large scale organisations so they measure the performance by conducting sample testing.

Examples –

i. A supervisor may measure performance during the work is being done by inspecting each part manufactured before the product is assembled.

ii. Manager may measure performance of its sales executives at the end of every month.

The performance can be measured using several techniques like personal observation, sample checking, performance reports, etc.

Examples –

i. A manager fills the appraisal form to evaluate his/her subordinate’s performance,

ii. Finance manager calculates ratios to evaluate and compare company’s performance with forecasted results.

iii. Marketing manager may prepare area-wise sales report in units sold and revenue earned.

Step # 3 – Comparing Actual Performance with Standards:

This step involves comparison of actual performance with the standard to check if there are any deviations between actual and desired results. The comparisons are easier for performances expressed in quantitative terms.

For example – It is easy to compare the actual revenue earned by the sales executive with targets given to him. If he achieves less than the target then the reasons need to analysed to ensure better performance in the future.

Step # 4 – Analysing Deviations:

Deviation is the difference between actual performance and the standard performance. To understand the reasons of deviations management must determine the acceptable range of deviations and the process to analyse the causes of deviations exceeding the acceptable range. To analyse the causes of deviations in the critical areas, management uses Critical Point Control and Management by Exception.

Critical Point Control:

Critical point control refers to controlling the key areas which are critical to the overall performance of an organisation. Since it is difficult for a large scale organisation to check at every point of action, the management sets the critical points. Whenever there is any deviation in the actual performance, the performance at critical points is analysed.

For example – Production center is a critical point in a manufacturing organisation. The causes of increase in cost will first be analysed at production point.

Management by Exception:

Management by exception also referred as control by exception refers to controlling of significant deviations which exceed the acceptable or permissible limit. Management by exception states that in an attempt to control all activities management may not be effective and may result in controlling nothing. Following management by exception, management identifies the deviations beyond permissible limits and analyse their causes.

The causes may include unrealistic standards, defective process, and inadequacy of resources, structural drawbacks, organisational constraints and environmental factors beyond the control of the organisation. Therefore, it is important to analyse the causes of deviations to take corrective actions at the appropriate level.

Step # 5 – Taking Corrective Action:

The final step in the controlling process is taking corrective action for all such deviations which are beyond permissible limits. Management must take corrective and preventive actions so that deviations do not occur again and standards are accomplished effectively.

Examples of corrective actions –

i. If a project is running behind schedule because unskilled workers take longer to complete the task then management may employ skilled workers to complete the project on time.

ii. The cost of production rose by 7% and on analyzing the cause of deviation it was found that actual quantity of raw material used was more than the standard quantity. The standard quantity calculated was inaccurate. Management takes the corrective action by recalculating the standard quantity of raw material so that cost can be calculated correctly in future.