In this article we will discuss about:- 1. Concept of Inventory Control 2. Importance of Inventory Control 3. Methods.

Concept of Inventory Control:

The term inventory control is used to cover functions which are quite different and are related to one another only in that they both require the maintenance of adequate records of inventory as well as receipt and issue corresponding to these two functions. It is interpreted as accounting control and operating control.

Accounting control of inventories is concerned with the proper recording of the receipt and consumption of the material as well as the flow of goods through the plant into finished stock and eventually to customers.

It is also concerned with the safeguarding of the undertaking’s property in the form of raw materials, work-in-progress and semi-finished product. Operating control of inventories is concerned with maintaining inventories with the optimum level keeping in view the operational requirements and financial resources of the enterprise.

Importance of Inventory Control:

ADVERTISEMENTS:

The aim of holding inventories is to allow the firm to separate the process of purchasing, manufacturing, and marketing of its primary products. Inventories are a component of the firm’s working capital and as such represent a current account.

Inventories are also viewed as a source of near all cash. The purpose is to achieve efficiencies in areas where costs are involved. The scientific inventory control results in the reduction of stocks on the one hand and substantial decline in critical shortages on the other.

In the following paragraph we can specify the various importance’s that accrue from holding inventories:

(i) Reducing Risk of Production Shortages:

ADVERTISEMENTS:

Firms mostly manufacture goods with hundreds of components. The entire production operation can be halted if any of these are missing. To avoid the shortage of raw material the firm can maintain larger inventories.

(ii) Reducing Order Cost:

Where a firm places an order, it incurs certain expenses. Different forms have to be completed. Approvals have to obtained, and goods that arrive must be accepted, inspected and counted. These costs will vary with the number of orders placed. Smaller the inventories lesser the capital needed to carry inventories.

(iii) Minimise the Blockage of Financial Resources:

ADVERTISEMENTS:

The importance of inventory control is to minimise the blockage of financial resources. It reduces the unnecessary tying up of capital in excess inventories. It also improves the liquidity position of the firm.

(iv) Avoiding Lost Sales:

Most firms would lose business without goods on hand. Generally a firm must be prepared to deliver goods on demand. By ensuring timely availability of adequate supply of goods, inventory control helps the firm as well as consumers.

(v) Achieving Efficient Production Scheduling:

The manufacturing process can occur in sufficiently long production runs and with preplanned schedules to achieve efficiencies and economies. By maintaining reasonable level of inventory production scheduling becomes easier for the management.

(vi) Gaining Quantity Discounts:

While making bulk purchases many suppliers will reduce the price of supplies and component supplies will reduce the price of supplies and component parts. The large orders may allow the firm to achieve discounts on regular basis. These discounts in turn reduce the cost of goods and increase the profits.

(vii) Taking the Advantage of Price Fluctuations:

When the prices of the raw materials are low the firm makes purchases in economic lots and maintains continuity of operations. By reducing the cost of raw materials and procuring high prices for its goods the firm maximises profit. This with the help of inventory control the firm takes advantage of price fluctuations.

ADVERTISEMENTS:

(viii) Tiding over Demand Fluctuations:

Inventory control also helps the firm in tiding over the demand fluctuation. These are taken care of by keeping a safety stock by the firm. Safety stock refers inventories carried to protect against variations in sales rate, production rate and procurement time. Inventory control aims at keeping the cost of maintaining safety stock minimum.

(ix) Deciding timely Replenishment of Stocks:

Inventory control results in the maintenance of necessary records, which can help in maintaining the stocks within the desired limits. With the help of adequate records the firm can protect itself against thefts, wastes and leakages of inventories. These records also help in deciding about timely replenishment of stocks.

Methods of Inventory Control:

ADVERTISEMENTS:

Inventory control is concerned with the periodic review of materials in stock to detect those not required for planned production or for other purposes not required and whether obsolete materials continue to occupy storage space until removed from stores.

The inventory control methods give us a means for determining an optimal level of inventory as well as how much should be ordered and when. There are several methods suggested for inventory controls.

The following are the most important systems used for inventory control:

(a) ABC System:

ADVERTISEMENTS:

A firm using ABC system segregates its inventory in to three groups-A, B and C. The ‘A’ items are those in which it has the largest rupee investment. This group consists of the 20 per cent of the firm’s rupee investment. The B group consists of the items accounting for the next largest investment, i.e., the B group consists of the 30 per cent of the items accounting for about 8 per cent of the firm’s rupee investment.

The C group typically consists of a large number of item accounting for small rupee investment. C group consist of approximately 50 per cent of all the items of inventory but only about 2 per cent of the firm’s rupee investment.

The common procedure for categorisation of items into ‘A’, ‘B’ and ‘C’:

(i) The categorisation can be made by comparing the cumulative percentage of items with the cumulative percentage of usage value.

(ii) All the items are to be ranked in the descending order of their annual usage value.

(iii) The cumulative percentage of items to the total number of items is also marked in another column.

ADVERTISEMENTS:

(iv) The cumulative totals of annual usage values of these items along with their percentages to the total annual usage value are to be noted along-side.

The advantages of this system are listed below:

(i) It helps in achieving the main objective of inventory control at minimum cost.

(ii) It helps in developing a scientific method of controlling inventories.

(iii) It gives closer control on costly items.

Limitation of ABC Analysis:

ADVERTISEMENTS:

(i) The system analyses the items according to their value not according to their importance in the production process.

(ii) The analysis to be effective needs to be constantly undertaken and periodically reviewed by management.

(iii) Generally hundreds of items fall in category ‘C’ as a result a lot of time is spent on managing inventory.

(b) Budgetary Control System:

Budgetary control is a tool of management used to plan, carry- out and control the operations of business. It establishes pre-determined objectives and provide the basis for measuring performance against these objectives. Under this system the number of units of the materials to produce a finished product and the level of inventory to be maintained and the quantities to be purchased during the period are all pre-determined.

When these plans are projected in advance they are called budgets. Control over inventories is exercised on the basis of budgeted figures. Successful inventory budgeting depends upon the sales forecast. The budget on control system has the advantage of the co-ordination on the inventory consumption level and the expected consumption.

ADVERTISEMENTS:

This system integrates and ties together all activities of the enterprise right from the planning to controlling. Control helps to eliminate or reduce unproductive activities and minimising waste. It is an effective method of controlling activities of the business unit since it provides standards against which actual performance is measured.

(c) Minimum-Maximum System:

This is one of the oldest methods used in most of the business for controlling inventories. It is essential that proper control should be exercised on the level of the inventory to be maintained. Efficient management of inventory demands that both over and under investment in stock be avoided.

If higher levels of inventories are maintained stock level will be influenced by obsolescence, change in fashion and improvements in technicalities. Too much capital tied up in inventories results in the lower rate of return and the possibility of substantial loss from decline in market value.

Too small a quantity is likely to reduce the value of the business and proper servicing of the customers. According to this, a maximum level of inventory based upon the demand and the minimum level to prevent out of stock conditions for each item of stock are established. An order is placed when the minimum level is reached which will bring the quantity to the maximum level.

(d) The Economic Order Quantity Approach:

ADVERTISEMENTS:

The Economic order quantity (EOQ) refers to the optimal order size that will result in the lowest total of order and carrying costs for an item of inventory given its expected usage, carrying cost and ordinary cost. By calculating an economic order quantity, the firm attempts to determine the order size that will minimise the total inventory costs.

Assumptions:

(i) Constant or uniform demand.

(ii) Independent orders.

(iii) Instantaneous delivery.

(iv) Constant ordering costs.

(v) Constant carrying costs.

(vi) Constant unit price.

Finding Economic Order Quantity:

The EOQ model assumes that the finished goods are sold at a constant rate overtime. The important decision in inventory management is to balance the cost of holding inventories with the cost of placing inventory replenishment orders. When the holding costs and ordering costs are balanced, the inventory costs are minimised and resulting order quantity is called the economic order quantity.

Total inventory cost = Ordering cost + Carrying cost

Total ordering cost = Number of orders x Cost per order

= Rs.U/Q x F

Where

u = Annual usage

Q = Quantity ordered

f = fixed cost per order

Total carrying cost = Average level of inventory x price per unit x carrying cost.

Total carrying cost = Rs. Q/2 x P x C

= Rs. QPC/2

where

Q = Quantity ordered

P = Purchasing Price per unit

C = Carrying cost.

Inventory Level and Order Point for Replenishment:

From Fig. 1., it can be noticed that the level of inventory will be equal to the order quantity (Q units) to start with. It declines to level 0 by the end of period 1. At that point an order for replenishment will be made for Q units. In view of zero lead time the inventory level jumps to Q and the same procedure follows in the subsequent periods. As a result of this the average level of inventory will remain at Q/2 units, the simple average of the two end points Q and Zero.

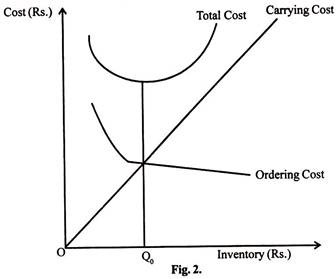

From the above we know that as order quantity increases the total ordering costs will decrease while the total carrying cost will increase in proportion to the magnitude of the order quantity.

From Fig. 2 it can be seen that the total cost curve reaches its minimum at the point of intersection between the ordering cost curve and the carrying cost line. The value of Q corresponding to it will be the economic order quantity Q0.