In this article we will discuss about Marginal Efficiency of Capital (MEC):- 1. Meaning of Marginal Efficiency of Capital 2. Factors of Marginal Efficiency of Capital 3. Criticisms.

Meaning of Marginal Efficiency of Capital (MEC):

MEC refers to the expected profitability of a capital asset. It may be defined as the highest rate of return over cost expected from the marginal or additional unit of a capital asset. First we must go to the marginal unit of the capital asset and secondly its cost has to be deducted from its return.

Now the MEC in its turn, depends on two factors: the prospective yield of the capital asset and the supply price of the capital asset. The MEC is the ratio of these two factors. The prospective yield of a capital asset is the total net return from the asset over its life time.

The supply price of an asset is the cost of producing a brand new asset of that kind and not the supply price of an existing asset. It is referred to as the replacement cost. If the supply price of a capital asset is Rs. 20,000 and its annual yield is Rs. 2000, then the marginal efficiency of this asset is 2000/20000 x 100 = 10 percent. Thus the marginal efficiency of capital is the percentage of profit expected from a given investment on a capital asset.

ADVERTISEMENTS:

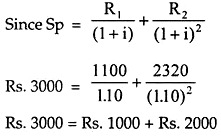

Keynes relates the prospective yield of a capital asset to its supply price and defines MEC “as being equal to that rate of discount which would make the present value of the series of annuities given by the returns expected from the capital asset during its life equal to its supply price”. This may be put in the form of an equation.

Where Sp is the supply price or the cost of capital asset, R1,R2… Rn are the prospective yields or the series of expected annual returns from the capital asset in the years 1,2…….. n, and i is the rate of discount. This makes the capital asset exactly equal to the present value of the expected yield from it. This can be explained with a numerical example.

Let us assume that:

ADVERTISEMENTS:

1. The life time of a capital asset (n) is 2 years.

2. The supply price of the capital asset (Sp) is Rs. 3000.

3. The expected yield from the asset at the end of one year (R1) is Rs. 1100.

4. The expected yield from the asset at the end of 2 years (R2) is Rs. 2420.

ADVERTISEMENTS:

The MEC or the rate of discount which will equate the future yields of the asset with its supply price is 10% as shown below:

In this way, discounted prospective yields of capital asset can be brought into equality with the current supply price. Thus investment will take place only if the net prospective yield of an asset is greater than its supply price and given the income flow the higher the supply price of the capital asset, the lower will be the rate of discount.

Factors of Marginal Efficiency of Capital (MEC):

The various factors that bring about shifts in MEC are short run or endogenous factors and long rim or exogenous factors.

The short run factors are:

1. Expected demand:

If the demand for the product is expected to be high in future, the MEC will be high and the investment will increase. On the other hand if the demand for the product is expected to decline in future the MEC will be low and investment will fall.

2. Costs and prices:

If the costs are expected to decline and if the prices are expected to increase, the expectation of the producer will go up. On the other hand if the costs are expected to go up and prices are to decline the MEC will receive a set back and the investment will be less.

ADVERTISEMENTS:

3. Propensity to consume:

If the propensity to consume is more than the volume of investment will be more and vice versa.

4. Changes in income:

An increase in the level of income will stimulate investment while a decrease in the level of income will discourage investment.

ADVERTISEMENTS:

5. Current state of expectation:

Businessmen while making expectations take into account the current state of affairs regarding costs, prices, returns etc. If they are high the MEC is bound to be high for new projects of investment.

6. Level of confidence:

During period of optimism the businessmen over estimate and boost the MEC of capital assets. During period of pessimism they under estimate and reduce the MEC of capital assets.

ADVERTISEMENTS:

The long run factors which influence the MEC are as follows:

1. Population growth:

A rapidly growing population means a rapid increase in the demand for all types of goods and hence investment rises and conversely, a decline in population will decrease the demand investment.

2. Development of new areas:

When a new area is developed heavy investments in all fields such as agriculture, industries, electricity, housing etc., are to be undertaken.

3. Technological factors:

ADVERTISEMENTS:

New invention or new discovery may necessitate the installation of new machineries in the industrial enterprise and encourage investment.

4. Productive capacity of the Industry:

If the existing capacity is fully utilised then any further increase in demand will be met with by making fresh investment on new capital equipment.

5. Level of current investment:

If the existing level of investment is already high there will be little scope for further investment and vice versa.

Criticism of the Marginal Efficiency of Capital:

Keynes used the term marginal efficiency of capital in a vague manner. Secondly, Keynes failed to recognize that interest rates are also governed by expectations like the marginal efficiency of capital. He considered marginal efficiency of capital in the field of dynamic economics and rate of interest in the field of static economics.

ADVERTISEMENTS:

The rate of discount or yield i.e., r is conventionally called the Marginal Efficiency of Investment (MEI). Keynes originally called it the ‘Marginal Efficiency of Capital’. Brooman says that it is preferable to use a term which refers explicitly to investment (i.e., MEI). The MEI (or MEC) ought to be distinguished from the ‘Marginal product of capital’ which refers to the increase in current output resulting from the addition of one more unit of capital.

It is clear that the marginal product of capital is a physical quantity similar to the marginal product of any other factor. The MEI is a percentage rate, and not the physical quantity. Again the marginal product of capital does not involve expectations about the yield from the unit of capital during the remainder of its life. But the MEI is very much concerned with such expectations about the yield.

Strictly speaking, however, there is a difference between the MEC and the MEI. The MEC is derived as the relationship between i (rate of interest) and the optimum level of capital stock. The MEI is derived as the relationship between i (rate of interest) and the optimum change in capital stock. It can be said by way of corollary that the MEC and the MEI are interrelated.

The MEI really indicates the decision to invest whereby there is change in the capital stock. This relationship between investment as the change in capital stock and the actual capital stock presents a difficulty in determining the MEI. If investment is change in capital stock, it can be assumed that the capital stock is fixed once investment is underway.

Keynes recognized this difficulty and sought to overcome it by stating that he was interested in short period changes in investment. In the short period change in investment would be insignificant relative to the entire capital stock; therefore, the impact of investment on capital stock could be ignored.

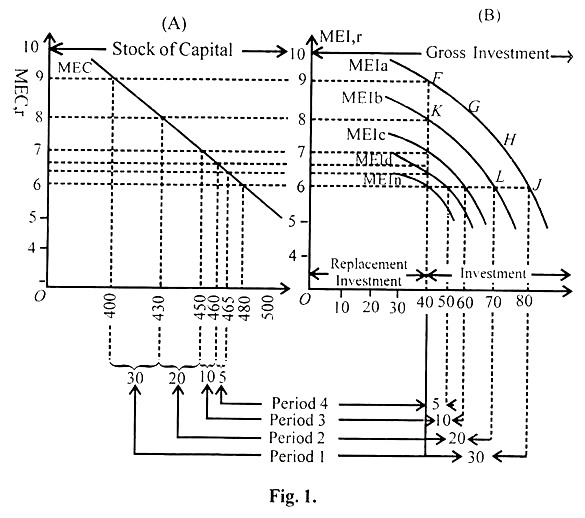

The relationship between MEC and MEI is illustrated in the figure 1.:

MEI schedule indicates the rate of investment spending per time period at each possible market rate of interest for different levels of the stock of capital. Part A shows the MEC schedule. When the rate of interest is 9% and capital stock is 400 billion dollars, the net investment is zero. MEI schedule labeled MEIa shows that at point F, when the rate of interest is 9%, the net investment is zero.

If rate of interest falls to 6%, net investment will be 30 billion dollars. At G, the MEI is 8%, because the rise in net investment spending from zero to 15 billion dollars has raised the prices of capital goods which has reduced the rate of interest to 8%. As this is higher than MEI (6%) higher rate of net investment is needed.

At point H, MEI has fallen to 7 per cent because higher rate of net investment spending has pushed the prices of capital goods to a higher level. The MEI is still above 6 percent, so a still higher rate of net investment spending is wanted. At point J, MEI is 6 percent. It is no higher or lower than the initial rate of interest.

From the beginning to the end of this first time period, with net investment of 30 billion dollars during the period, the capital stock will have risen to 430 billion dollars from its beginning level of 400 billion dollars. As shown in Part A, this increase of 30 billion dollars reduces the MEC about 8 per cent (actually 7.87) from its previous level of 9. Because r is still 6 per cent, further growth in the capital stock is called for.

The amount by which it grows in the second period, or the rate of net investment spending in the second period, depends on the MEI schedule. With MEC now at 8 per cent, the new MEI schedule, relating investment expenditures to the interest rate, must show zero net investment at an interest rate of 8 per cent (point K).

Therefore, MEIb, the new schedule, lies below MEIa because of the increase in the stock of capital in the first time period; the whole MEI schedule must fall to a lower level with each movement to a lower point on the given MEC schedule, MEIb slopes down ward for the same reason that MEIa sloped downward—the rising supply price of capital goods as the rate of output of these goods is expanded in response to investment spending.

ADVERTISEMENTS:

The rate of net investment spending in the second period is determined in the same way as the rate in the first period was. It will be the rate that reduces the MEI to equality with r. Schedule MEIb shows that net investment for the second period will be 20 billion dollars (point L). Note that this is below the 30 billion dollars of the first time period. Given that the prices of capital goods rise with their rate of output as soon as net investment reaches the rate of 20 billion dollars per time period, the rise in prices of capital goods reduces the MEI from 8 to 6 per cent, or the equality with r.

In the first period, only when net investment reached the 30 billion dollars the rate was the rise in prices of capital goods sufficient to produce the greater drop in MEI from 9 to 6 percent, or to equality with r. In other words, the greater spread between MEI and the r at the beginning of the first period permitted the higher rate of investment spending in that period.

Net Investment spending of 20 billion dollars during the second period raises the stock of capital to 450 billion dollars from its level of 430 billion dollars at the beginning of the second period. The increase in the capital stock reduces the MEC further to about 7 percent (actually 7.12) which produces the new, lower MEI schedule, MEIc. The rate of net investment spending in the third period as given by this schedule is 10 billion dollars.

This again raises the stock of capital now from 450 billion dollars to 460 billion dollars. This in turn reduces the MEC and creates the new, still lower MEI schedule, MEId. The rate of net investment spending in the fourth period is then 5 billion dollars. With no shift in the MEC schedule and with no further fall in r, net investment spending, lower in each succeeding period, eventually raises the stock of capital to 480 billion dollars, at which level the MEC equals r.

The actual stock of capital is now the profit-maximizing stock for the interest rate of 6 per cent. With the capital stock at 480 billion dollars, the relevant MEI schedule is MEIn, which shows net investment to be zero and gross investment equal to replacement investment per time period. We have reached a new equilibrium, which will be upset only by a shift in the MEC schedule or by a change in the market rate of interest.